Payoneer has reported strong results in Q3 2024, supported by a growing customer base across multiple segments. We spoke to Payoneer CEO John Caplan to find out more about their global market strategy.

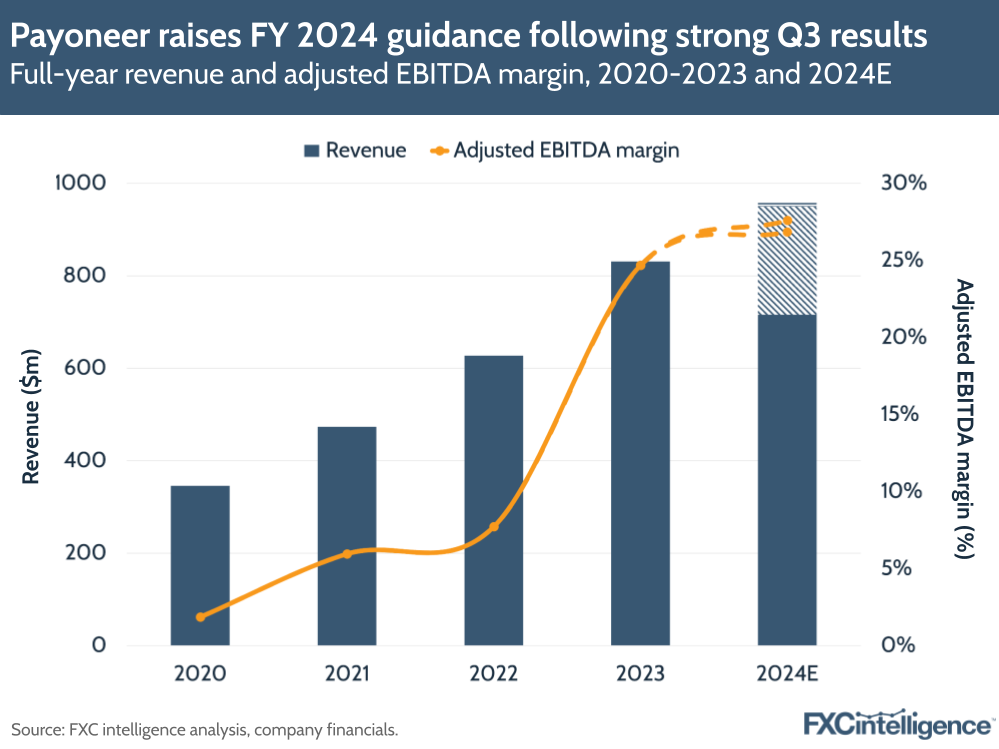

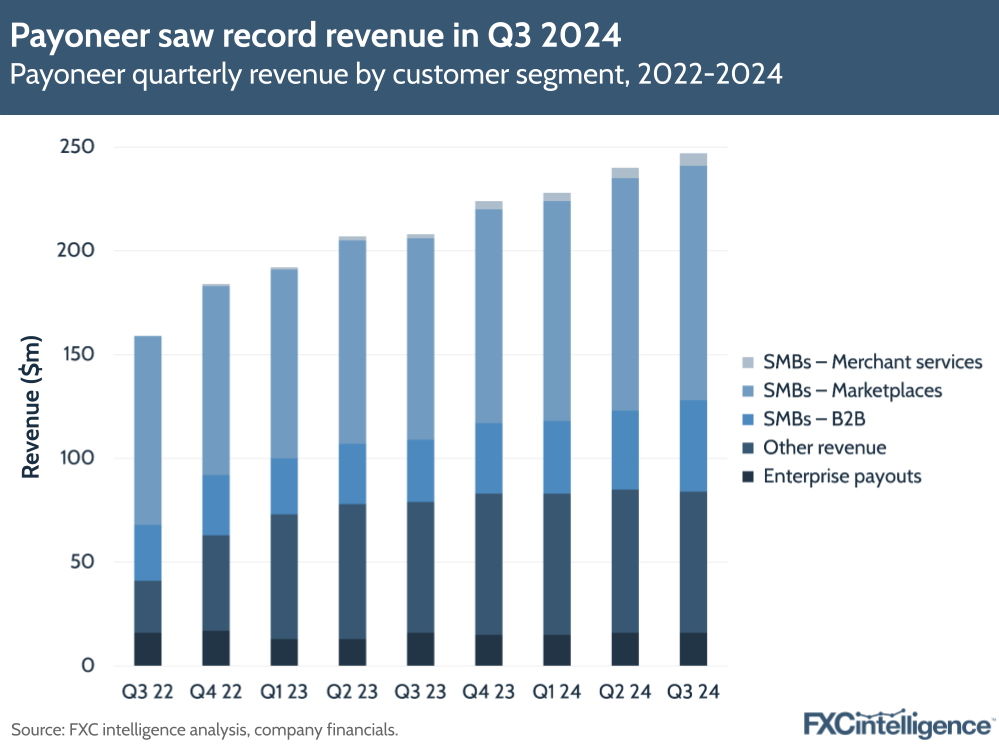

Payoneer saw record revenue and volume in Q3 2024, reporting revenue growth of 19% YoY to $248m and 25% YoY volume growth to $20.4bn. The company has updated its 2024 guidance, with a $20m increase in its revenue outlook range to $950-$960m and a $30m rise in its adjusted EBITDA guidance range to $255m-$265m.

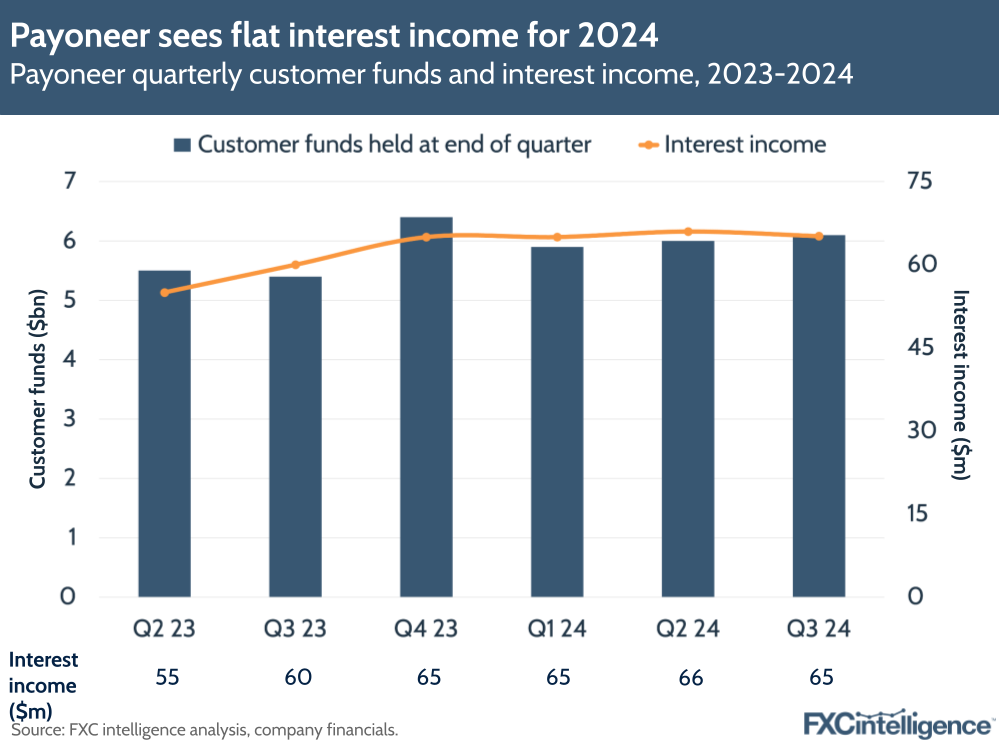

Meanwhile, the company’s net income rose to $41.6m, representing 224% YoY growth, which was driven by a mix of operating and interest income. Payoneer’s operating income saw 5% YoY growth to $35m, while interest income grew by 8% YoY to $65m, despite relatively flat average interest rates YoY. This reflects a significant increase in customer funds held by Payoneer, which surged by 13% YoY, reaching $6.1bn in Q3 2024.

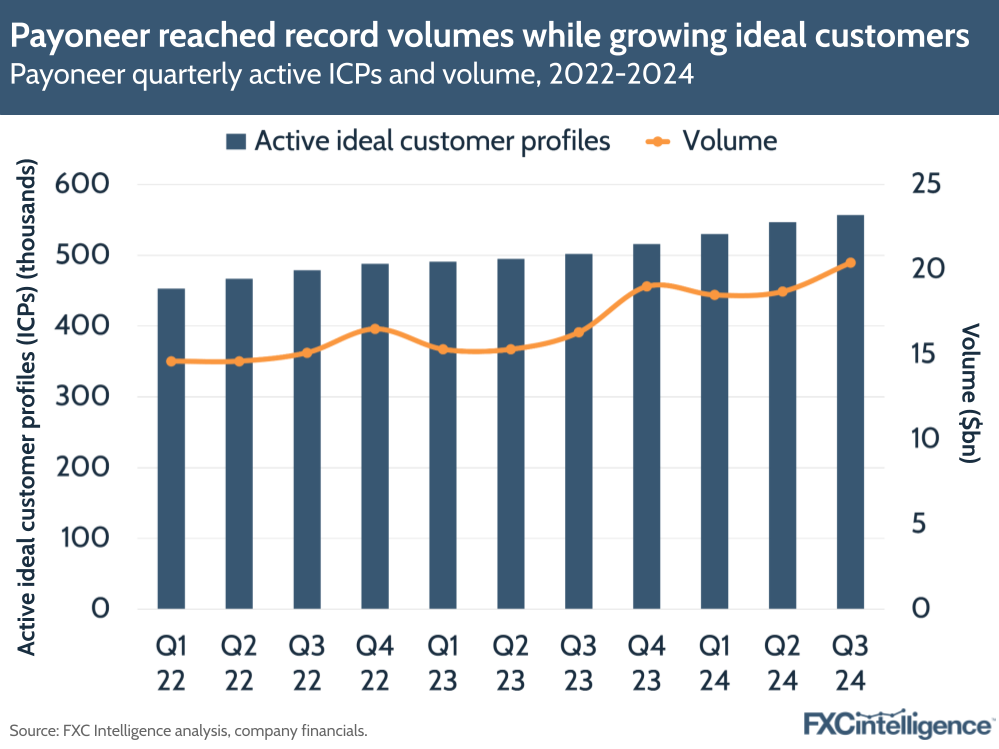

Back in 2023, Payoneer launched its ideal customer profiles (ICPs) strategy, focusing on customers handling over $500 in monthly volume that were active over a trailing 12-month period. In Q3 2024, the company saw continued growth in customer acquisition, with 11% YoY growth to 557,000 ICPs. It also grew volume and revenue from more than 10,000 ICPs by 25%.

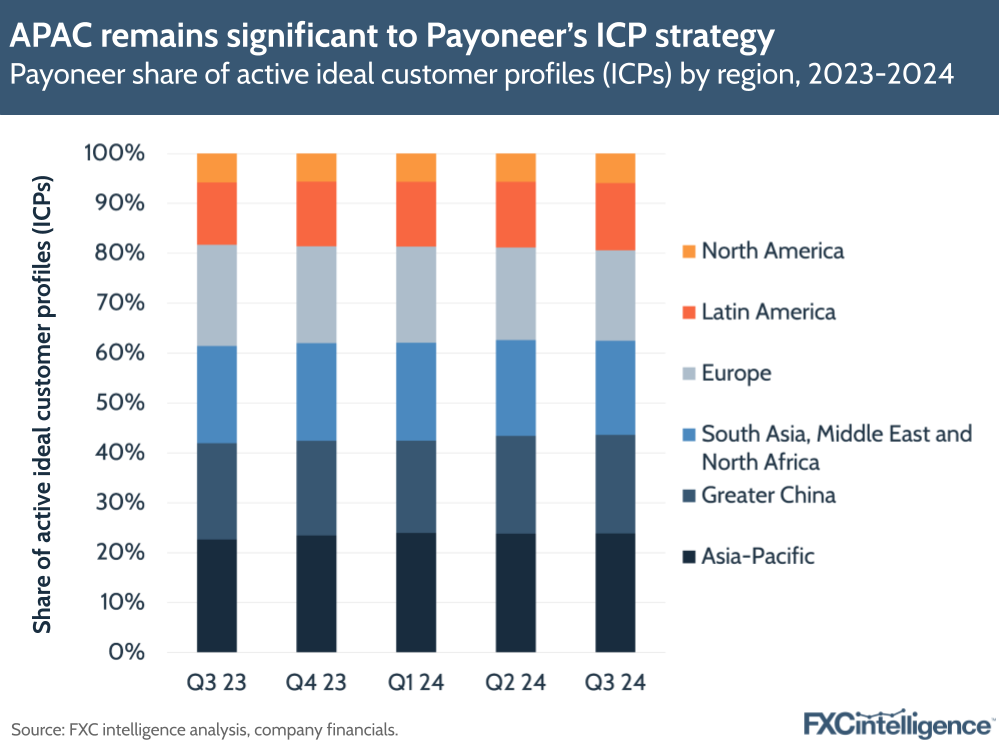

The company also saw significant market expansion in APAC and LatAm countries, reporting double-digit ICPs growth. Payoneer expanded its market share in China through cross-selling card products to existing customers with payment service provider (PSP) relationships, while also acquiring new ecommerce sellers and wallet share with current customers. In the earnings call, Payoneer also mentioned its pending acquisition of a licensed Chinese PSP, which is expected to complete in the first half of 2025.

In response to the strong Q3 2024 performance, Payoneer’s stock price went up by 20.8% the day after it released its earnings and stayed in the range of $10.30 to $10.39, reflecting a positive outlook for the company.

As a global payments player, Payoneer has built a scalable platform to meet the diverse financial needs of small and medium-sized businesses (SMBs), serving a customer base beyond traditional banking. To find out more about the company’s market strategy, we spoke to CEO John Caplan.

Behind Payoneer’s growth in Q3 2024

Daniel Webber:

Given the record revenue and volume in Q3 2024, what’s driving the strong performance?

John Caplan:

We have a clear strategy to build and deliver a full financial stack for cross-border business owners, covering 100% of accounts receivable and accounts payable for SMBs. This is an opportunity for which the legacy banking infrastructure and the legacy banks do not have the capabilities, multi-currency accounts technology, go-to-market capability, or network dynamics to create that flywheel.

Payoneer’s flywheel is beginning to spin. More larger customers are joining Payoneer, the existing customers are utilising more of our products and services, our customer count is growing, revenue per customer is increasing and the stickiness of the Payoneer product and platform is rising. The customers that we’re adding are larger, with greater need for more services and our volume is increasing.

Our customer acquisition costs have also declined over the last 18 months, and the quality of those customers has increased. We’re seeing leverage unlock in our business. Through the first half of this year, Payoneer’s core business, net of interest, is profitable. We’re generating a tremendous adjusted EBITDA, but even net of interest, this is a profitable growth company. Everything has worked well in all the arenas.

Our organisation is thinking about how to continue to institutionalise profitable growth across the organisation. I’m confident in the guidance we provided at our investor day in September 2023, which we’ve reaffirmed every time we’ve communicated with shareholders. I was on a call with one of our top 10 shareholders and he said: “every 90 days, Payoneer exceeds my expectations of what great looks like, and every 90 days, my confidence in Payoneer grows.”

Payoneer projects strong performance for full 2024

Payoneer has raised its full-year guidance for both revenue and adjusted EBITDA margin, reflecting the ongoing momentum into the final quarter.

For 2024, Payoneer is projecting total revenue between $950m and $960m, with revenue excluding interest income of $700m-$710m. Without interest income, the company projects $20m increase in revenue, implying full-year growth of 17% at the midpoint.

Payoneer has also increased guidance on adjusted EBITDA to $255m-$265m (up by $30m from Q2 2024) and interest income revenue to $250m (a $10m increase). The interest income revenue of 2024 is expected to be three times the growth rate of 2023. However, the company has said in 2025 it expects interest income to decline YoY as the market expects average interest rates to decline from over 5% in 2024 to approximately 3.7% in 2025.

Payoneer’s interest income reached $65m in Q3 2024, representing 26.2% in share of total revenue. Despite relatively flat average interest rates this year, the customer funds held by Payoneer contributed to an 8% increase in interest income. This reflects the growth in customer funds, which surged by 13% YoY to $6.1bn in Q3 2024.

Payoneer’s approach to targeting customers

Daniel Webber:

How are you driving down customer acquisition costs while also adding the customers you need to grow?

John Caplan:

We have go-to-market teams around the globe, including in Pakistan, Vietnam, South Korea and Argentina. Our teams are part of the communities they serve, which is a powerful driver of SMBs acquisition globally. We attract 11 million applications a year, using our data to identify high-quality ones. These are then handled by someone who speaks the language and goes to the same coffee shop as the person who needs our service. The authenticity of these connections sets us apart – while we’re a global financial services company, we build very local relationships with our customers.

For example, in Dubai, we have many marketing services customers using our virtual credit cards to buy ads for their customers globally, so the focus is on selling our card products. In Ukraine, where we have lots of agriculture customers, we focus on the multicurrency wallet due to domestic banking laws.

We have a global platform that’s localised based on the needs of high-growth centres in our tier-one countries. We lead with one product in some regions and then cross-sell the stack, while in other regions, we focus on a different product and then cross-sell the stack. Ultimately, the cost of customer acquisition is decreasing because the quality of the customers is going up, and we understand how to match their needs with our capabilities.

Payoneer’s growing ideal customer profiles (ICPs)

Payoneer saw a record total volume of $20.4bn in Q3 2024, reflecting 25% YoY growth and accelerating for the seventh consecutive quarter. While this was driven by multiple segments, B2B volume grew 57% YoY, accounting for nearly 25% of quarterly revenue (excluding interest income) and contributing over 13% to total volume share.

Payoneer’s customer portfolio continues to evolve, with ICPs now making up 28% of the overall base, up from 25% at the beginning of 2023. Payoneer noted that it had seen “solid penetration” of larger ICPs (i.e. with greater than $250,000 a month in volume), while the number of customers with $500,000-$10m in monthly volume grew by 12%.

Against this backdrop, Payoneer continued to show strong performance in Greater China, with 110,000 active ICPs and 13.4% YoY growth in regional ICPs. However, it is important to note that Payoneer separates Greater China from the APAC region in its figures.

APAC had the largest share of active ICPs in Q3 (24%), followed by Greater China (20%), South Asia, Middle East and North Africa (19%) and then Europe (18%). Having said this, Greater China currently holds the largest share of Payoneer’s revenue at 34%.

Notably, LatAm saw the fastest ICPs growth in Q3 2024, followed by APAC and China. Despite the growth, LatAm counties only generated $24.7m in regional revenue, representing the smallest proportion of revenue share at 10%.

Addressing SMBs’ demands by scaling infrastructure

Daniel Webber:

How are you meeting the full financial needs of cross-border SMBs, and what role is your infrastructure playing in this?

John Caplan:

2025 is the 20th anniversary of Payoneer, coming up next year, which is amazing. The infrastructure of Payoneer – our regulatory relationships, banking relationships, global brand, technology platform and its flexibility – enables us to capture the large global B2B opportunity ahead.

We operate in the four most interesting areas of cross-border trade: SMBs, emerging markets, B2B and cross-border payments. These are the most exciting parts of the payments landscape, and we lead in all of them. We are earning trust in our relationships with our customers, regulators and banks every single day.

The infrastructure enables us to offer a service to customers that other competitors cannot. We also have the scale to be local globally, which is a powerful advantage for a financial services company to leverage efficiently at scale. These dynamics are accelerating both our growth and leverage in the business.

Payoneer’s SMBs continues to show strong results

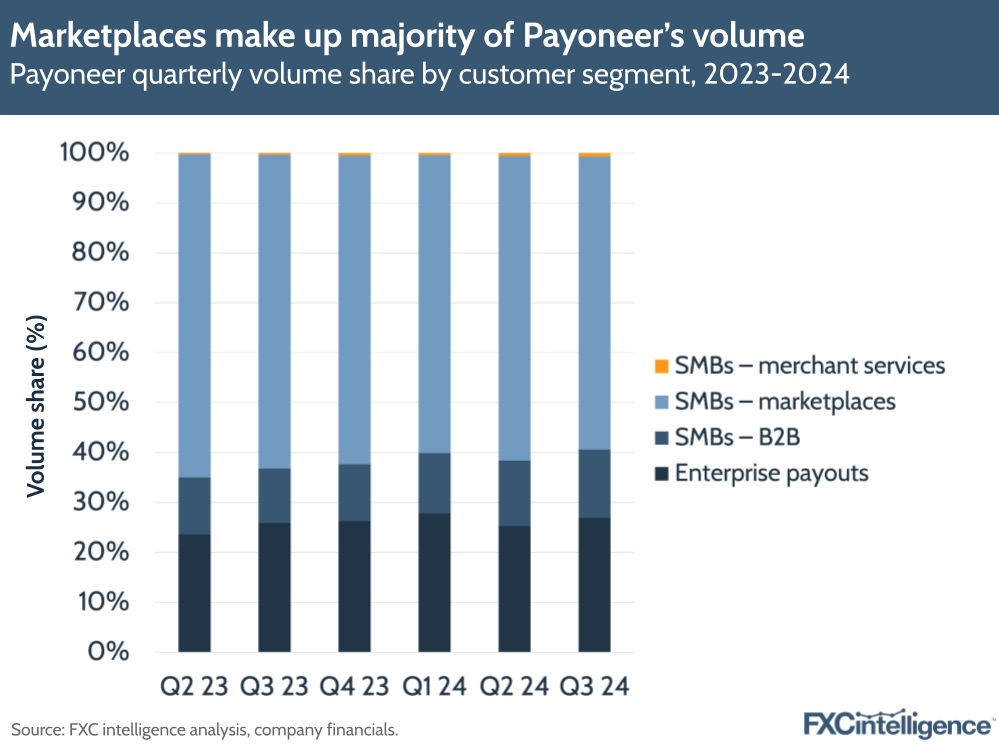

With strong performance from marketplaces and B2B payments, Payoneer’s SMBs segment performed well in Q3 2024, reporting $15bn in total volume and $163m in quarterly revenue – growth of 24% and 26%, respectively. In total, the SMB segment accounted for 73% of total volumes for the business, driving 66% of total revenues.

Payoneer’s marketplaces continued to account for the largest share of its SMB volumes, with 17% YoY volume growth in Q3 2024, representing 59% of total volume share. The B2B segment accounted for a lower volume share at 14%, but continues to see much faster volume growth this year (57%, versus 1% growth in Q3 2023), and has grown its share across quarters sequentially since Q3 2024 (11%).

Enterprise payouts accounted for the remaining 27% of volumes in Q3 2024, though volumes grew by 30%, which was faster than SMB total volume growth at 24%.

Breaking down Payoneer’s SMB segment further, 46% of Payoneer’s Q3 total revenue came from marketplaces, with 18% coming from B2B and 2% coming from merchant services. Though Payoneer’s recently established merchant services accounts for the smallest share of revenues, it is scaling up quickly, with revenue growth of 200% and 143% volume growth during the quarter.

Amongst growing SMB revenues, enterprise payout revenues were flat compared to Q3 last year at $16m, accounting for around 6% of revenues overall. As a result, enterprise payouts have continued to trend down compared to previous quarters in terms of revenue share (compared to an 8% share in Q3 2023, and a 10% share in Q3 2022).

Payoneer’s enterprise business

Daniel Webber:

Are big enterprise customers still a significant part of your interest?

John Caplan:

Of course, our enterprise business has seen exceptional growth year over year and the growth will continue. It’s because our infrastructure is the best of breed. It’s a great time to be in payments.

Daniel Webber:

John, thank you.

John Caplan:

Thanks very much.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.