Payoneer has reported a record quarterly increase in its Q1 2024 results, with strong performance across the company, led by its B2B and Merchant Services businesses. We caught up with CEO John Caplan to find out more.

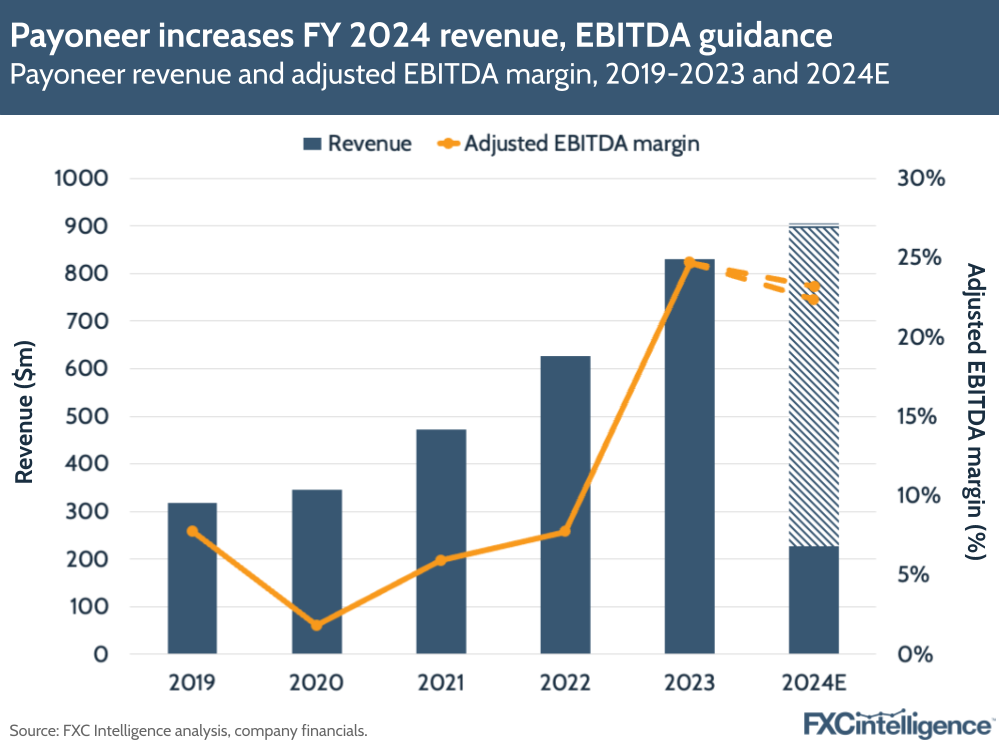

Payoneer has reported its Q1 2024 results, with revenue increasing 19% to reach a record $228.2m. Adjusted EBITDA, meanwhile, increased 68% to $65.2m, giving the company an adjusted EBITDA margin of 28.6%. Volume also saw its strongest growth rate in nearly three years, increasing 21% YoY to $18.5bn.

While the company said this growth was driven by increases across all channels, faster growth in its higher take rate B2B and Merchant Services businesses was a key driver.

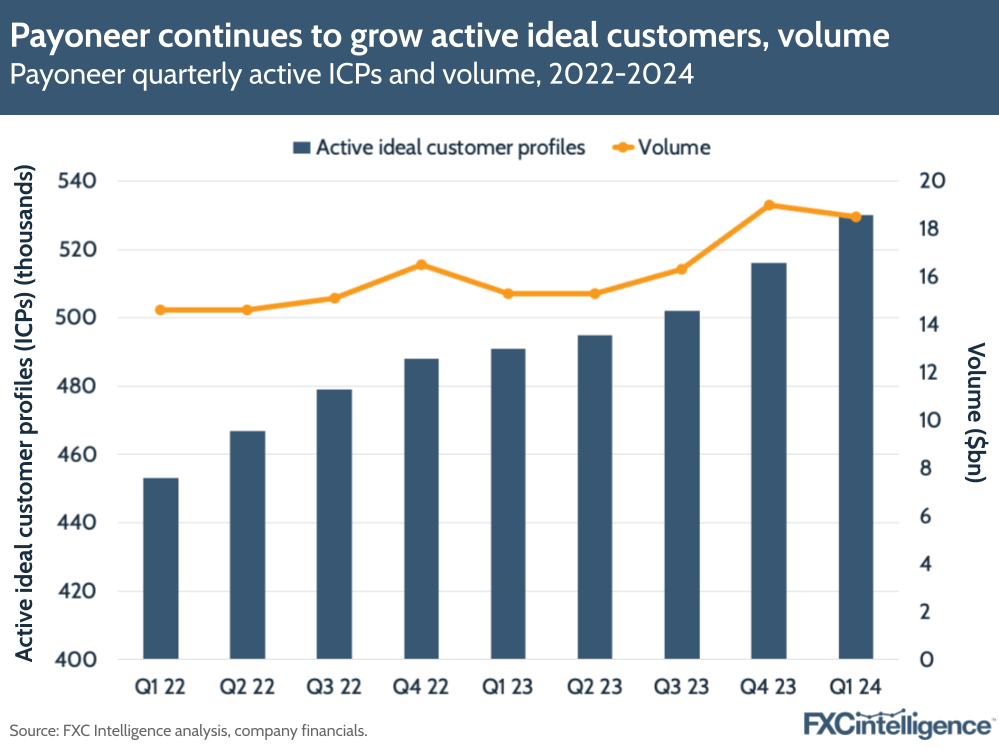

The company also continues to see returns on its focus on active ideal customer profiles (ICPs), with ICPs overall increasing 8% YoY to 530,000. Payoneer also reported higher ICP growth in regions with a higher take rate, with ICPs climbing 15% in APAC, SAMEA and LatAm. Larger, higher volume ICPs – defined as those with over $10,000 a month volume – also grew faster, increasing 13% YoY.

The strong results prompted Payoneer to increase its guidance for FY 2024, with the company now projecting revenue for the year to reach $895m-905m (up from its previous projection of $875m-885m), while its adjusted EBITDA is now expected to reach $200m-210m (up from $185m-195m), for an adjusted EBITDA margin of 22.4-23.2%.

To find out more about the drivers of the company’s strong performance, I caught up with CEO John Caplan, with additional input from Michelle Wang, VP of Investor Relations at Payoneer.

Drivers of Payoneer’s record Q1 2024 results

Daniel Webber:

Let’s start at the top. Some record numbers across the board. What’s been driving that?

John Caplan:

The highlights for Q1 for Payoneer, the big highlights: 8% growth of our ideal customers; 13% growth of the customers greater than $120,000 of trailing 12 month AR; 33% volume growth in our B2B business; over 200% growth in our checkout business; 34% growth in our card usage; great strength in our China business.

It was really a top to bottom beat. Great execution by the team – we saw good results even in our marketplace business, 13% volume growth. There wasn’t a number in our operations in Q1 that wasn’t going in the right direction.

Daniel Webber:

What are some of the drivers underneath that you would pick out?

John Caplan:

In the B2B business, it’s really 32% growth of ICP customers in APAC and 40% growth of volume in APAC. 32% growth of ideal customers in SAMEA and 41% growth of volume in SAMEA.

So our acquisition model is working, our cross-sell focus is working. Really, running a company like Payoneer is basically a series of a thousand decisions daily and a strategy that we put in place.

I became CEO on 1 March 2023. You and I are talking 9 May 2024 and we just had, in Q1, the best quarter this company’s ever had. It’s not me, it’s us here.

The leadership team we’ve put together – Bea, Kevin, Adam, Oren, Sarit, Elana, Tsafi – is on the same page to go capture a big market opportunity. And when you can see the volumes we’re doing and the size, we’re all very bullish on where the company is and how we can execute for the balance of 2024 and beyond.

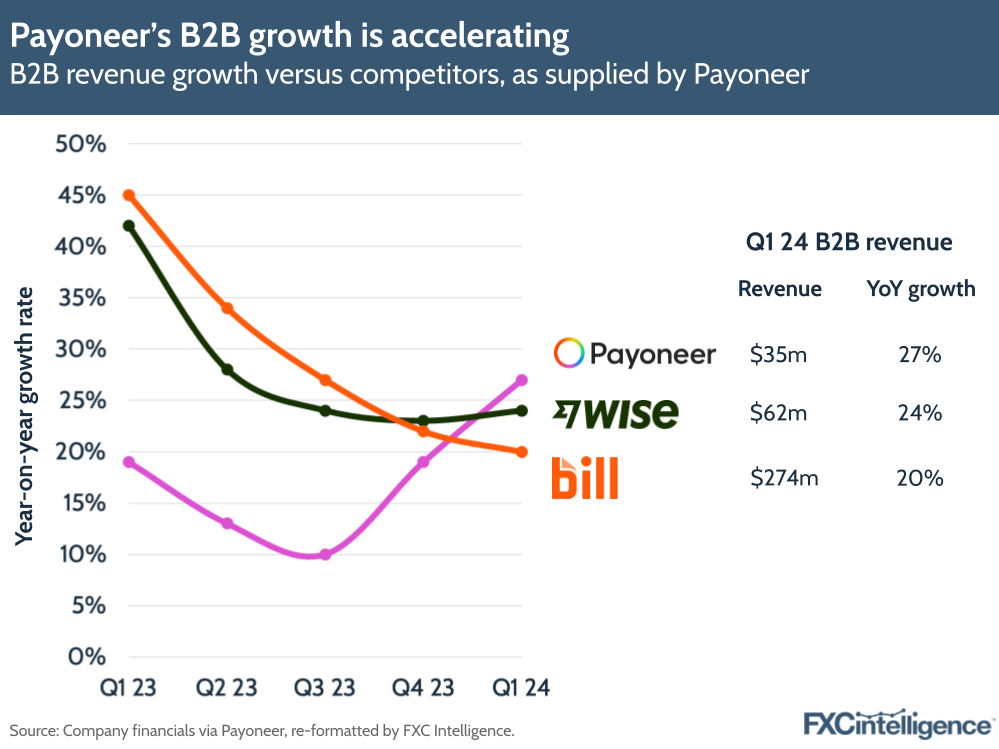

Payoneer’s B2B growth versus competitors

Daniel Webber:

You’ve shared a slide with us [below] showing Payoneer’s B2B growth compared to the market. Talk us through that.

John Caplan:

We’ve seen exceptional growth in our B2B franchise. In Q3 of 2023 we had 1% volume growth, in Q4 of 2023, 13% volume growth, and Q1 of 2024, 33% volume growth. So across the board, Payoneer as a solution for cross-border SMBs is accelerating in our penetration of the big opportunity.

When we look across similarly focused companies or directionally focused companies, our growth has been accelerating versus companies like Bill or Wise or others. We saw 39% growth in volume in APAC, 41% volume growth in SAMEA. It feels very clear to me that we have accelerating momentum in what is our core driver of the teams going after the $6tn global B2B market.

Daniel Webber:

It’s at least $6tn – our market size numbers show the opportunity to be much larger than that. Unlike some of the companies you compared against, the heart of Payoneer is that you focus on emerging markets. How does that fit in?

John Caplan:

That’s part of the core narrative of why Payoneer is so special right now. It’s high-growth emerging markets where we have a competitive moat with our banking infrastructure, with our regulatory infrastructure, with our brand, our go-to-market teams and our product market fit.

We’re in a position to capture markets where we have an exceptional lead and you can see others that are not enjoying the kind of momentum we have in our organisation.

Drivers of B2B growth

Daniel Webber:

What is driving growth in your B2B products beyond picking the right emerging markets?

John Caplan:

It’s the right emerging markets, it’s the power of our invoicing capability, our batch payments capability, our schedule payments capability, as well as our other spend management tools, our commercial Mastercard tools, our network payments across the board.

What we’ve established for our customers is a full suite that they’re using. So it is not just that the B2B product is better, but the B2B product is designed for service-oriented market economies to have the tools they need to invoice their customers and get paid, and then manage in a multicurrency wallet their expenses for everything that they have to manage.

The true benefit that we see is that our customers in those high-growth emerging markets want a full AR/AP solution attached to the multicurrency account, and we’re the only game in town.

Payoneer’s regional focuses

Daniel Webber:

You mentioned China. Are there any other regions that you want to highlight, and how are you ensuring that you are executing the right strategies for each country?

John Caplan:

LatAm had 18% or 19% growth, really solid results in Latin America for the team and great execution. Our India business also continues to be strong – we really saw broad-based across-the-board strength.

How we’ve organised the company is we’ve made big investments over many years when Scott [Galit, former CEO] was running the company, big investments putting in place a go-to-market infrastructure globally.

We have people on the ground in Delhi, Lahore and Sao Paulo. We have people on the ground who know the market, who are empowered both on how they price our products, who they sell our products to and what configuration of products we offer. So we have a strong central platform that’s sold and executed locally to the needs of customers around the globe.

Michelle Wang:

One thing that’s really unique about Payoneer is really elevating the regional and country leaders. Unlike many American and Western companies that put an expat in X region to lead the team, we really do find local leaders who are incredibly familiar with and have grown up in the regions that they are leading, which I think really is a differentiating factor versus putting an American expat in Ho Chi Minh City to try to run our APAC business.

Exploring M&A opportunities

Daniel Webber:

You also touched upon potential future M&A in the earnings call. What types of opportunities are you looking for?

John Caplan:

We are looking at deals particularly on the spend management side. Think about AP products that Payoneer has: our cards, our pay within the network, batch payments of contractors around the globe. All of these have been largely homegrown and built inside the business.

There are some very interesting products and services that we’re looking at acquiring to improve the amount of options our customers have. Managing contractors or employees around the globe would be one area, managing their card and their spend management might be another area, loyalty programs that they’re implementing for themselves and in the vendors that they’re selecting.

There is a long list that our team is going through – meeting companies, evaluating the fit and the culture of the team so that the people we add to Payoneer fit with Payoneer.

Daniel Webber:

Is there anything else you want to highlight that we’ve missed?

John Caplan:

Michelle and I have done 25 or 30 investor calls since yesterday morning. Pretty consistently what we’re hearing is: “You delivered what you said you were going to do. You laid out a strategy and you’re executing against the strategy.”

They are recognising the top to bottom beat; effectively every number going in the right direction. The feedback has been: “We’re starting to understand because of your disclosures.” That’s slide 23 and 24 in our disclosure deck, which we did again this quarter.

What the investor community is saying is: “We see what you see and we understand why you’re so excited about what you’re building here in the company because we can see the traction and momentum.”

Michelle Wang:

We even added another new slide this quarter, slide 13. It’s really interesting. We’ve tried to help people better understand what exactly it is that our platform does. We’re in accounts receivable but also, importantly, we’re an accounts payable company.

On slide 13 of that presentation, you can see how we’ve been growing the amount of AP usage from customers who are using three or more AP products from us.

Historically, if you think back two, three years ago, everyone thought of Payoneer as primarily helping international sellers get money from large Western marketplaces. But nobody fully appreciates that AR/AP story and side of our business. So we increasingly are looking to highlight that as well, which I think is vastly underappreciated today.

Daniel Webber:

John, Michelle, thank you.

John Caplan and Michelle Wang:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.