The B2B cross-border payments space is set to see continued consolidation this year, as well as trends around real-time payments, AI and consolidated services. We spoke to a number of B2B payments companies to explore some of the biggest trends the industry can expect in 2024.

In 2024, B2B cross-border payments companies will continue to provide platforms that enable fast, less costly and more transparent payment flows between businesses.

B2B payments is a less mature industry than consumer money transfers, with no clear leaders of the pack worldwide. Having said this, FXC’s own data forecasts that the global B2B cross-border payments market will total $50tn by 2032, driven by growth across large enterprises and SMBs, as well as increased digitisation.

A wave of investments in B2B payments startups in 2023 suggest that disruption is coming in the space in 2024. What’s more, established companies in the cross-border payments space – such as Payoneer and OFX – saw a sizeable contribution to their revenues coming from B2B, highlighting a growing demand from businesses for better payment solutions.

But what will be the biggest trends for this space this year? FXC Intelligence spoke to a number of companies in the B2B cross-border payments space, including at Fintech Connect Europe in December, to find out.

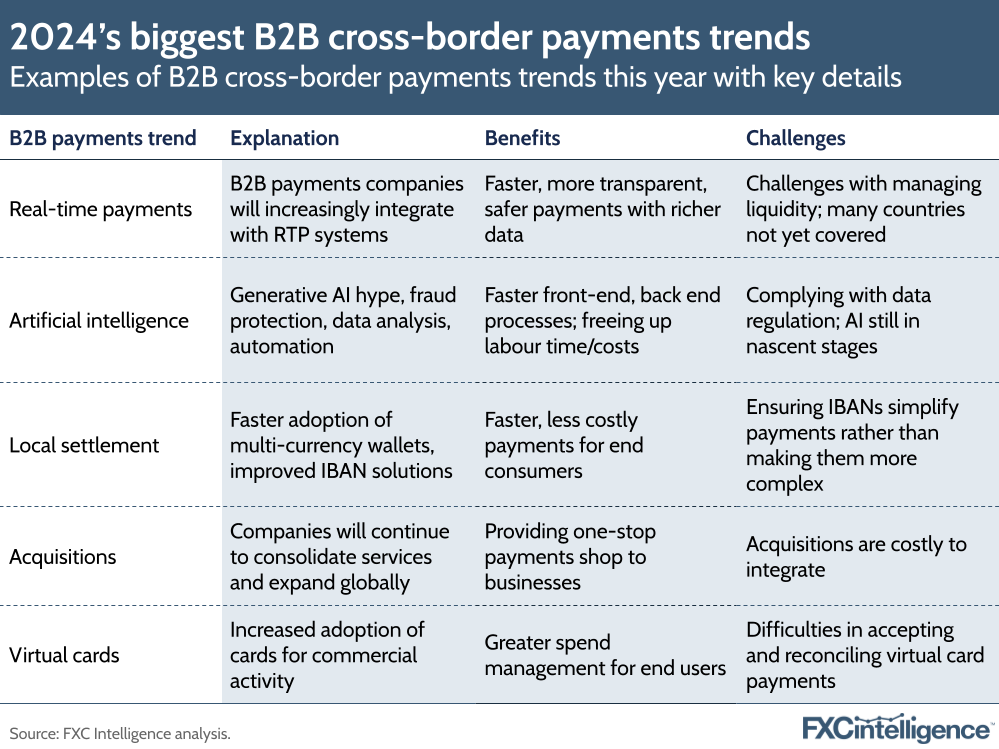

Real-time payments and interoperability ramp up

Speed, cost and transparency are the major pain points for businesses sending money globally. B2B payments experts say that real-time payment networks worldwide could help them to tackle these challenges in 2024.

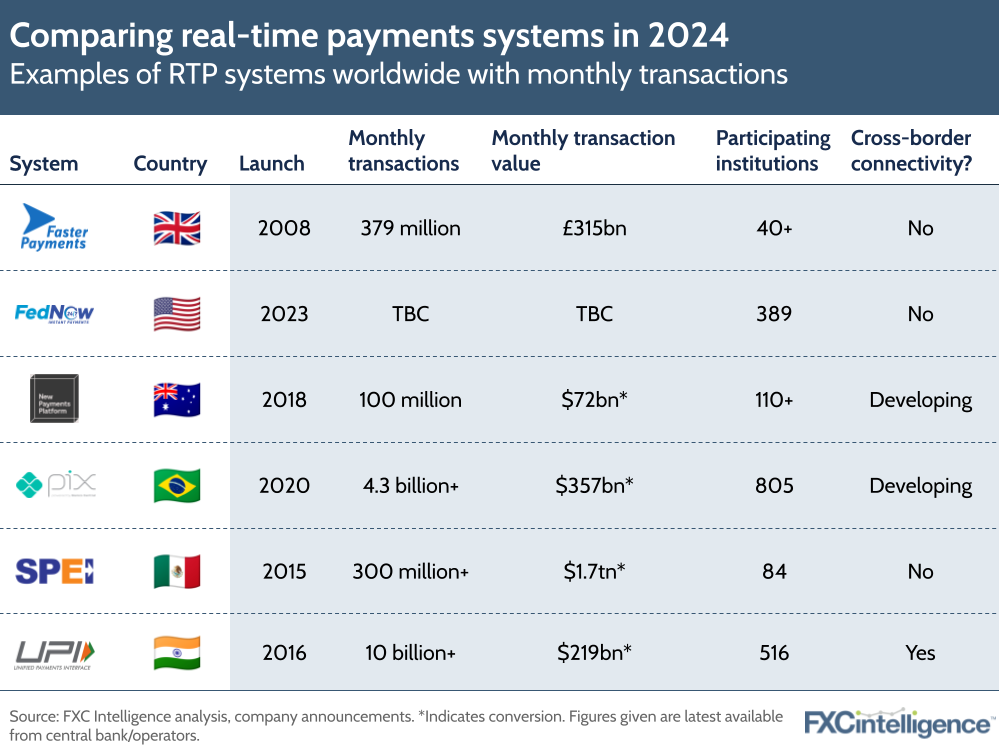

These networks – which include the US’s recently launched FedNow system or the UK’s Faster Payments system – enable 24/7 processing of domestic payments so that they are sent, cleared and settled instantly or within seconds. According to online sources, there are more than 50 of these real-time payments systems worldwide.

“We’ll see continued emphasis on real-time payments designed to minimise friction, with a strong focus on improving the overall customer experience,” says James Butland, VP Payment Network at Mangopay. “This involves user-friendly interfaces, faster settlement times and transparent fee structures.”

While real-time payments aren’t new, there has been a recent drive to connect up domestic instant payment systems to enable faster cross-border consumer payments, particularly in Southeast Asia. Singapore has so far connected up its system with those of Malaysia, Thailand, Indonesia and India, allowing travellers from one country to the other to make purchases by scanning QR codes.

When it comes to B2B payments, the next focus for companies in the space will be to continue to integrate fast local payment rails which, even if they aren’t yet linked up with others abroad, will speed up the movement of money across account networks within countries, cutting down payments delays.

“Real-time payments are becoming really prevalent as businesses try to expand,” says Cian Fitzpatrick, Transfermate SVP, Head of EMEA. “Our strategy is to get as real time as possible by connecting to real-time rails as they open up.”

Meanwhile, IFX Payments Product Director Rosie McConnell says that the company is looking at connecting to more real-time payment methods, but that there are still quirks around them that need to be considered. Although there are strict rules about the way money is represented to the end customer, often the liquidity doesn’t arrive until a bit later for payments companies, which can make the process harder to manage.

“Those methods are providing better service to consumers but for our business, it’s causing issues on the backend in terms of liquidity management, because it’s essentially like a mini-loan [to the customer],” she says.

Tied in with the concept of interlinking payment systems, upcoming changes to regulations around the world could make B2B payments faster and more secure. One example is the EU’s legal payments framework PSD3, proposed last year, which aims to harmonise and improve payments across the EU market.

A number of regional initiatives worldwide are helping drive changes to regulations, such as the EU’s Revised Cross-Border Payment Regulation and the Association of Southeast Asian Nations, as well as global initiatives, such as the G20 Roadmap for Enhancing Cross-border Payments.

“When rules are more aligned, transactions can speed up, become more secure, and flow smoothly across borders,” explains Matt Jackson, FreemarketFX VP, Relationship Management & Marketing. “It’s not just about dealing with paperwork; it’s about making transactions happen faster and keeping them really secure. As the rules come together, businesses can look forward to a better environment for using advanced technologies in their cross-border transactions.

Businesses will demand more transparent payments

Universal Partners CEO and Co-Founder Oliver Carson says that technological improvements mean that clients can track payments across instant payment rails in real-time, giving them better oversight of a customers’ supply chain. “We expect businesses to turn to FX providers with the ability to track the progress of transactions at any given time and those with access to real-time rails,” he explains.

McConnell sees payments getting faster as local instant payment methods connect across borders – but one of the biggest challenges for B2B cross-border payments is being able to track payments effectively.

“Interoperability is part of a conversation in the market at the moment,” says McConnell. “Intermediaries add cost and they add a delay, but the most annoying thing is that payments get sent and data gets totally corrupted. So that’s one of the main challenges: transparency and maintaining the integrity of the data.”

For this reason, McConnell notes that a key theme for this year will be financial institutions onboarding ISO 20022 standard for payment messages. Banks and payment companies are updating their systems to be able to accept and send ISO-compliant messages, which contain rich data that makes it easy to see where payments have come from. This makes reconciliation faster and also helps payment businesses to identify new product opportunities.

“As more financial institutions and payment systems embrace ISO 20022, a more standardised and globally consistent framework for data interchange is likely to emerge, fostering collaboration and reducing complexities,” says Jackson.

Meanwhile, Paytrix CPO and Co-Founder Eddie Harrison notes that while online retail experiences are seeing constant innovation – shopping via livestream on platforms like TikTok, for example – the underlying infrastructure supporting payments is still running on dated infrastructure. However, this could change in 2024.

“Up until now, attempts to upgrade the systems for cross-border payments have been tinkering around the edges,” says Harrison. “I think in 2024, we’ll start to see the emergence of digitally native, cross-border payment solutions that provide genuine and comprehensive global capabilities rather than the reskinning of legacy infrastructure.”

Settling cross-border payments in local currencies

Driving change and interconnectivity in legacy payments takes time, and many cross-border payment infrastructure aren’t yet good enough to support this, particularly in emerging markets.

“On the ground, we know that current cross-border payment options, especially those of traditional finance, are not adequate,” says SUNRATE CEO and Co-Founder Paul Meng. “The difficulties of conducting business are exacerbated by the requirement for businesses to have bank accounts in each foreign market in which they conduct business. This can be more difficult for companies intending to operate in emerging markets.”

Several of the companies we spoke to said that integrating with local payment rails will be crucial in 2024. According to Fitzpatrick, the biggest change in the market has been moving from focusing on international to local payment rails.

“[Transfermate] was one of the quickest to market in realising that the only way to circumvent an international transaction is to turn it local,” he says. “You can only do that by having the ability to hold accounts and move money locally all over the world.”

Continuing a trend from 2023, Carson says that customers will look to settle cross-border transactions in local currencies, as opposed to sending USD to countries in APAC, Africa and Latin America. “We expect more businesses this year to shift towards using local currencies to avoid paying currency charges between suppliers and distributors,” he says.

Rapyd VP EMEA Sarel Tal explains how the company aims to integrate all the world’s payment rails into one global platform, through which businesses can accept payments, send money and hold funds globally. Rather than businesses having to have separate bank accounts for different regions, they are instead able to access and move funds through a single API.

“Reconciliation has always been an issue, but as you move into global payments, it’s becoming a bigger issue, because now you reconcile across multiple currencies, across multiple rails and data feeds from many providers,” says Tal.

Tal adds that interest rates rising significantly have boosted demand for fast B2B cross-border payments. With Rapyd’s platform, companies can collect payments in countries without needing to repatriate the money and use those funds to disburse locally.

Meng, meanwhile, talks about the potential of partnerships for driving faster payments in 2024. Last year, SUNRATE partnered with Mastercard to allow businesses to send money to a number of emerging Asian markets, including Thailand, Philippines, Malaysia, Vietnam and China.

“In the near future, cross-border payment delays and friction can be reduced by integrating real-time data into the payment systems through the use of AI, machine learning and other technological advancements,” says Meng.

AI to boost fraud prevention and analytics in 2024

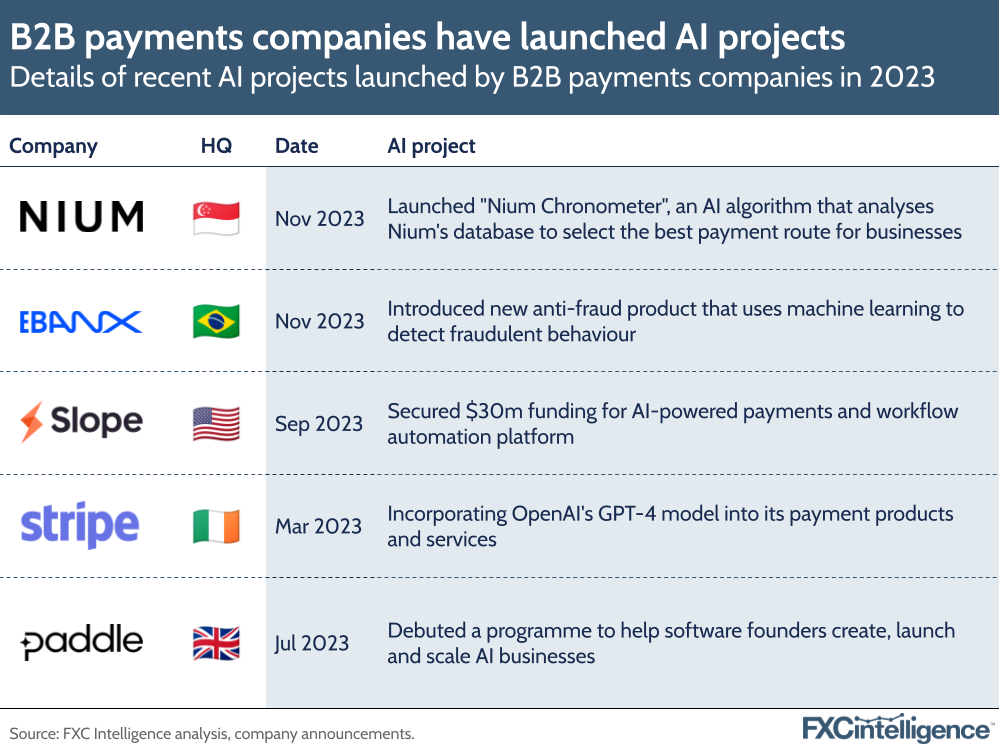

OpenAI’s ChatGPT kicked off a new wave of artificial intelligence hype in 2023, and this is likely to persist into 2024, though it could still be some time before benefits are realised.

AI has already been used across a variety of purposes in payments, but generative AI could enhance this. For example, AI can be used to analyse large customer datasets so that businesses can make more informed decisions; predict cash flows coming into the business; and replace manual processes involved with payments processing such as reconciliation.

“During 2023, large language models proved to be a versatile tool for increasing efficiency and providing data insights,” says Carson. “AI monetisation will be a significant trend for the payments industry in 2024, offering additional analysis capabilities throughout the varied payment routes and methods, whilst also providing real-time data to further enhance currency transfers.”

A big use case for AI at the moment is fraud detection, particularly after a year in which the wider financial industry has come under increasing scrutiny. The UK, for example, saw a 22% rise in automatic push payment fraud in the first half of 2023, according to banking trade association UK Finance.

Through machine learning, AI tools can be trained to detect fraudulent behaviour, flag it and prevent payments from ever leaving user accounts. This is the principle behind Mastercard’s fraud detection tool, which a number of banks are already using to protect customers.

Rapyd has also been exploring the potential of AI in combatting fraudulent payments, and is continuing to add AI capabilities to tools that will provide unique insights to customers and help them save money.

“These are unbelievable tools and the capabilities are insane,” says Tal. “Customers can save money not only on costs and through discounts, but also getting the payments faster so that they can save on interest rates.”

IFX Payments is currently exploring the role of AI in compliance and reconciliation, according to McConnell. While she says she doesn’t expect the company to be at the forefront of AI, she is “bullish” about the opportunity for clients.

“At the moment, it’s about preparing our data for the moment when these products come out so we can leverage them as soon as possible, and looking at low-hanging fruit like compliance,” she says.

But while AI projects continue to dominate the financial space, the role of the human still needs to be considered. SUNRATE’s Meng says that an optimal B2B payments experience is not “purely digital” and that in this field specifically it is even more important that businesses have the ability to connect with a dedicated (and preferably human) representative who can help solve issues as they arise.

“At the end of the day, consumers prefer to speak with businesses face-to-face about their needs and wants, which is considerably more challenging to do digitally and can exacerbate a sense of distance between them,” says Meng. “Ultimately, clients seek out individuals who can empathise with their circumstances, an attribute that AI and machine learning technology is (currently) unable to provide.”

Multicurrency wallets, IBANs and commercial cards

Besides integration with payment rails, the companies we spoke to said that there could be some new trends around B2B cross-border payments products in 2024.

Tied in with the localisation trend mentioned earlier, Butland says that 2024 will see the accelerated adoption of multicurrency wallets, which empower users to seamlessly hold and transact in multiple currencies using real-time FX rates. “This would aim to simplify international purchases without traditional currency conversion hassles,” he explains.

“We can expect to see continued advancements in FX solutions with real-time rates, automated hedging and integration with treasury management systems empowering businesses to optimise costs, enhance treasury control and ensure operational efficiency in the dynamic landscape of cross-border transactions.”

Harrison also says that the system for International Bank Account Numbers (IBAN) – originally introduced in a bid to erase the distinction between cross-border payments in Europe – has not been able to effectively speed up money movement for businesses. However, he predicts that this year could see a sea change with the introduction of better IBAN solutions.

“The reality is that IBANs are often only functional on a very local basis — with transactions across borders often treated, illegally, as foreign payments; or differences in IBAN formats leading to unnecessary rejections,” says Harrison. “This is a particularly common issue with single or multicurrency IBAN solutions. In 2024, we’ll see the emergence of genuine solutions that allow businesses to operate with a truly local footprint across all individual countries in Europe and beyond.”

Commercial cards will be another big product in 2024, says SUNRATE’s Meng, as businesses will “demand more spending limits and increased security for their B2B transactions”. The industry could also see an increased use of virtual cards – i.e. card numbers that are generated for a specific transaction. These cards offer a much greater control over spend and who can use funds.

“Research by Mastercard also showed that virtual cards have tremendous cost savings potential, and that is why we predict that businesses will increasingly turn to principal members of card schemes, as commercial cards are to become well-utilised as a form of business payment this year,” says Meng.

Meng adds that the adoption of new B2B payment services in 2024 will be heavily influenced by user experience, as “businesses want the same degree of convenience that they enjoy in personal transactions”.

Rebundling payment services for businesses

For business customers, historically the goal may have been to enlist B2B payments companies to carry out one particular service type – for example providing a FX hedging solution for a particular corridor, or offering an IBAN solution. While this single-service approach may have previously benefitted businesses, says Harrison, it’s also resulted in some of them having several different B2B payment providers covering different bases, making them harder to manage.

He argues this year could therefore see B2B payments providers expanding into new areas to offer increased value to consumers – a “rebundling” of services of sorts as, in the past, high street banks tended to offer most financial services for businesses and individuals. This could soon be the case but with specialised payments companies.

“We’re already seeing B2C and B2B fintech pioneers starting to extend their range of services into adjacent spaces,” he says. “And I think this consolidation will continue in 2024 with a great rebundling, particularly in the B2B space. For consumers, this will increasingly take the form of a superapp, whereas for businesses it will be via a super API.”

Rapyd’s Tal says that in the past most customers may have used the platform just to collect or just to disburse funds, but this has changed, particularly as the company has evolved to service larger corporates. “I think most of our new customers are using multiple capabilities across multiple jurisdictions or countries,” he says. “Adyen, Stripe, WorldPay – they’re all adding additional services.”

For IFX, McConnell says a key part of their strategy for this year will be providing the right value-added services to customers, giving them the right products at exactly the right time in their journey, and personalising products to suit certain requirements. For example, this could be tweaking IFX’s IBAN product so that it more adequately suits a legal firms’ requirements.

“On B2B, I think it’s just always gonna be a little bit behind on the current kind of consumer trends,” she says. “In the same way that consumers have had a bit of a boom in better financing, better payment flows, that’s now happening in the B2B space as well.”

Acquisitions and consolidation in 2024

While last year saw a general downturn in acquisition according to FXC research, B2B payments were still in the biggest category of acquiring companies in 2023, as we saw in our B2B roundup piece for 2023.

Many B2B payments-related acquisitions last year were to consolidate or expand services, such as Australian money transfer provider OFX’s acquisition of Paytron, through which it aims to increase the value of its B2B clients beyond spot payments, or American Express acquiring Nipendo to create and streamline a new B2B payments process.

Other acquisitions were about expanding services into new geographies. See Italian bank Nexi’s acquisition of Spanish B2B provider Paycomet, or UK-based B2B player Equals acquiring Belgium-based Oonex.

In the case of Rapyd, Tal says that 2024 could be the “year of Africa”, and that the company has built a joint venture with a large African media company. The company has also just launched its card acquiring business in Singapore and is well integrated with local payment rails in the region.

For Transfermate, Fitzpatrick says that around 70% to 80% of business payment flows will always come from the US, Europe and the UK as these are the heaviest markets. However, APAC represents a significant opportunity that the company continues to explore.

“When you start thinking about marketplaces and about the volume of funds that are moved through that region, it’s phenomenal,” he says.

Concerning APAC, Universal Partners’ Carson says that he expects to see a continued shift in payments from China to other countries, including European nations, as currency depreciation is helping to reduce the cost of transactions made in the Turkish lira and similar currencies.

On a wider note, he adds that over 70 elections taking place worldwide in 2024 are expected to cause exceptional volatility between many different currency pairs, which will have an impact on business’ FX strategies. This is also true of countries staving off inflation with varying levels of effectiveness.

“Businesses will be looking for ways to ensure that they are not exposed to these risks early in the year, when placing annual supply contracts, as election cycles begin to gain momentum,” says Carson. “These catalysts for volatility are truly global.”

How pricing will change going forward

A common theme in the consumer money transfer space is the extent to which new technologies, business models and infrastructure could help drive consumer money transfer costs down. When it comes to costs in the B2B space, competition could help drive pricing in the same direction.

“I believe that like many other markets, [B2B payments] will commoditise with respect to pricing,” says Tal. “As more and more providers start providing these services, the costs will go down, especially for companies like Rapyd. We collect and disperse locally, so we can actually use these funds on a local basis, and that really affects the cost of FX.”

Transfermate’s Fitzpatrick says that a lot of instant payment rails being introduced worldwide enable transfers at a lower cost, which in turn passes on benefits to end customers. But while the overall goal of the industry is to drive down FX costs, businesses will still need to monetise payments.

He explains, “We need to remember that businesses exist to make money, so where is that monetisation piece? In the world of cross-border payments, it is absolutely on FX.”

Stablecoins and CBDCs in 2024

For B2B payments (and payments more widely), the potential of cryptocurrencies as an actual payment method is still somewhat in flux, with many still seeing them as more of an asset. However, stablecoins and central bank digital currencies (CBDCs) are generally seen as less volatile options when it comes to payments, as their value is pegged to another asset (most often currency).

The influx of stablecoin and CBDC projects in 2023 (see below) looks set to continue in 2024, particularly as governments look to capitalise on the benefits offered by crypto while also maintaining control of a centralised payments system. While it’s not expected that stablecoin payments could be widely adopted for B2B payments any time soon, it’s interesting that two companies we spoke to mentioned stablecoins as a key trend for 2024.

Data from Coin Metrics and Visa shows that over the course of 2023, up to the end of Q3, the total amount of transactions with stablecoins was $5tn – a figure that FreemarketFX’s Jackson believes will be higher in 2024.

“Using CBDCs in B2B cross-border payments gives us a digital option supported by the government, mixing the reliability of regular money with the efficiency of blockchain technology,” says Jackson.

FXC has discussed the potential of stablecoins for cross-border payments, following the collapse of TerraUSD in 2022, which cast doubt over the idea that stablecoins are a safer choice than pure cryptocurrencies such as Bitcoin or Ethereum. However, since then there have been a swathe of stablecoin projects in the space, including PayPal introducing its own USD-backed stablecoin in August last year.

Carson says that while the company doesn’t expect to see mass adoption for digital currencies in 2024, the ongoing rumble of CBDC announcements last year and in 2022 will continue with more pilots and scheme linking announcements.

“Stablecoins will continue to have an impact in some of the more exotic currency corridors and pure crypto to move further from a payment use case to an investment product,” he says.

B2B payments will continue to see disruption in 2024

The trends noted above speak to a B2B cross-border payments industry that is still in growth mode, and the influx of new and upcoming businesses could drive further disruption in the space in 2024.

Ultimately, B2B payments may still be playing catchup with the consumer money transfer space when it comes to digitalisation. There are still some obstacles in countries around the world that are standing in the way of faster, more transparent, more secure and less costly cross-border payments.

However, established companies’ moving into the space and the number of new B2B startups popping up worldwide indicates the potential of this sector. FreemarketFX’s Jackson says that B2B payments will be part of a wider global push towards digitalisation in financial services this year, as businesses’ expectations of payments are evolving.

“The seamless payment experiences you have in your personal life are setting the bar for B2B payments,” he says. “These evolving expectations will act as a catalyst for the adoption of innovative solutions and technologies.”

In 2024, we’ll see more moves by B2B payments companies to automate their processes, consolidate services and integrate with real-time payment infrastructure to reduce costs, while delivering better products and services to customers.