To understand what’s going on in China, we spoke to a number of leaders at the major players: Jeff Parker, Group MD at WorldFirst; Ning Wang, Chief Business Officer at PingPong; and James Huang, VP Greater China for Payoneer.

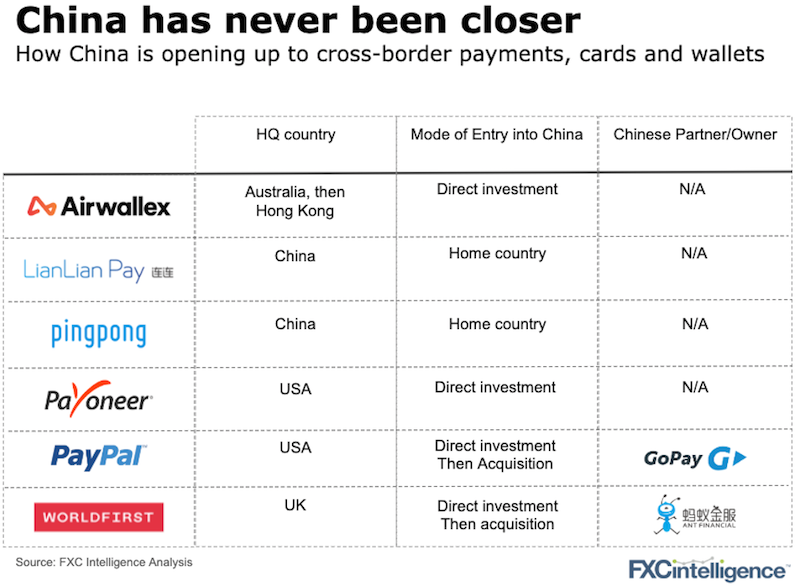

Entering the Chinese market is not easy due to the high regulatory and cultural entry barriers. Some players emerged organically in the country while others moved from the West to the East, including entering by acquisition.

We’ll try to distill what’s driving the market in into just a handful of takeaways:

1. Regulation

Firstly, no one wants to talk (officially) about regulation in China.

Two contrasting trends have been occurring in the market. On the one hand, regulation has been tightening. Western players who used to “piggy-back” off a local third-party player will now need to have their own licences to operate in the market.

Still, the People’s Bank Of China (PBOC), which is in charge of granting licences, is approving new players to enter the market if they meet certain criteria. Amex is currently making its way through the licencing process, and PayPal recently entered China through the acquisition of GoPay.

We would expect the smaller, unregulated players to slowly get squeezed out of the market but larger players, especially those enabling Chinese companies to operate globally, to find licensing solutions.

2. Localisation

Everyone agreed that the key to success in China was developing a fully localised product. What does this mean? A wide array of things: local language, local tech or it could be presenting pricing referencing the PBOC’s exchange rates.

Localisation creates a significant barrier to entry. As Ning Wang from PingPong says: “International players know that to be successful in this market, there is a need for localisation of the language, of the service. These players have to rebuild to enter China.”

And James Huang, VP Greater China at Payoneer, also adds: “And localisation, when you talk about localisation, you have to talk about both the business team, the operations team as well as the technology.

“If you want to be competitive in the field, you have to balance all three variables. One is the international infrastructure. Meaning your banking infrastructure, technology infrastructure, et cetera. Then you have to balance your domestic service, whether it’s talking about your operations, your onboarding, your KYC, etc. And then obviously the third is your local platform or user interface and technology.”

3. A more sophisticated customer

Chinese cross-border merchants are unique. As Jeff Parker, Managing Director at WorldFirst, puts it: “The way that Chinese merchants behave versus Western merchants is quite different with marketplaces. It’s a much bigger business in China and the tools that allow them to manage their business are more sophisticated than required by the UK or US.”

Although challenging, serving Chinese customers presents the opportunity to deliver more products and one of the holy grails in this sector – to develop an ecosystem.

4. Building ecosystems

Each of the players above are building ecosystems aiming to connect buyers and sellers in a closed network.

According to Jeff: “We believe there’s a really good opportunity to create an international payments ecosystem where you’re connecting the buyer and the seller. You can go to a much more trusted relationship. The funds movement can be instant and free. You can do things like escrow, you can do lending for both of those providers and you can build invoicing solutions.”

Doing so allows many more complementary products to be offered – especially around lending, invoicing and risk management. Ning Wang from PingPong affirmed: “PingPong, together with a number of payment providers, understands that we need to do more than just moving the money to develop our businesses.”

This view is confirmed by James Huang, VP and Country Manager for Greater China at Payoneer: “We strive to have more intimate relationships with our customers, and we try to go beyond payments. When you look at cross-border trading, the entire work stream, it’s actually quite sophisticated and complicated.”

Creating an ecosystem also lowers the cost of new customer acquisition as they can come from your own network.

As James says: “A lot of value added features that we’ve built on top of payments are what creates differentiating factors and customer stickiness.”

Anyone who can do this at scale can then hope to benefit from network effects and high valuations associated with that.

5. New opportunities for growth

Working with businesses who sell to consumers on the big marketplaces has been the main driver of growth in this market and will continue to be so. However, other segments appear to be emerging, such as selling to businesses as Jeff Parker from WorldFirst explains: “The B2B market is actually significantly bigger than the eCommerce kind of B2C market. It’s significantly more broken and slower and more complex. And we believe that there’s a huge opportunity to take that B2B market.

“I think our business could look quite different in terms of makeup in three or four years time. I think that B2B could be a significant proportion.”

Specialised channels within segments like mobile apps, travel and education seem to be fast growing as well.

China cross-border commerce is a large, complex, fast growing, highly regulated market with sophisticated customers – all the ingredients needed to support profitable continued growth of the incumbents. But don’t expect more than a handful of new players to try to enter the market, separate from whether the regulators then allow it.

[fxci_space class=”tailor-633421c50e147″][/fxci_space]