UPI and Pix – India and Brazil’s respective instant payment systems – have transformed the payments landscape in their home countries. We’ve analysed the latest performance and trends across both platforms, as well as the extent to which they are seeing cross-border development.

Pix and UPI are both account-to-account payments models enabling individuals and businesses to send and receive money instantly. Pix allows users to send money to other users via a Pix key – a unique identifier that securely links to a user’s bank account – or make payments to businesses using a QR code. Similarly, UPI allows users to make payments or send money directly to other users by inputting their UPI ID into a UPI-enabled app such as PhonePe, Google Pay or Amazon Pay.

However, there are key structural differences. For example, Pix is owned, operated and regulated by Brazil’s central bank, Banco Central do Brasil (BCB), but while UPI is regulated by the Reserve Bank of India, it is owned and operated by the government-backed entity National Payments Corporation of India.

UPI was launched several years before Pix and is operating in a country with a much higher population than Brazil, and as such has a significantly higher number of users and transactions though its platform. Pix has grown significantly in a short amount of time however, with 174 million individual consumers using the system as of March 2026 – approximately 82% of Brazil’s population (based on UN population figures cited by Worldometer). By comparison, UPI had around 400 million users as of January 2026 (according to a speech by the RBI’s Deputy Governor), which would account for approximately 27% of India’s population.

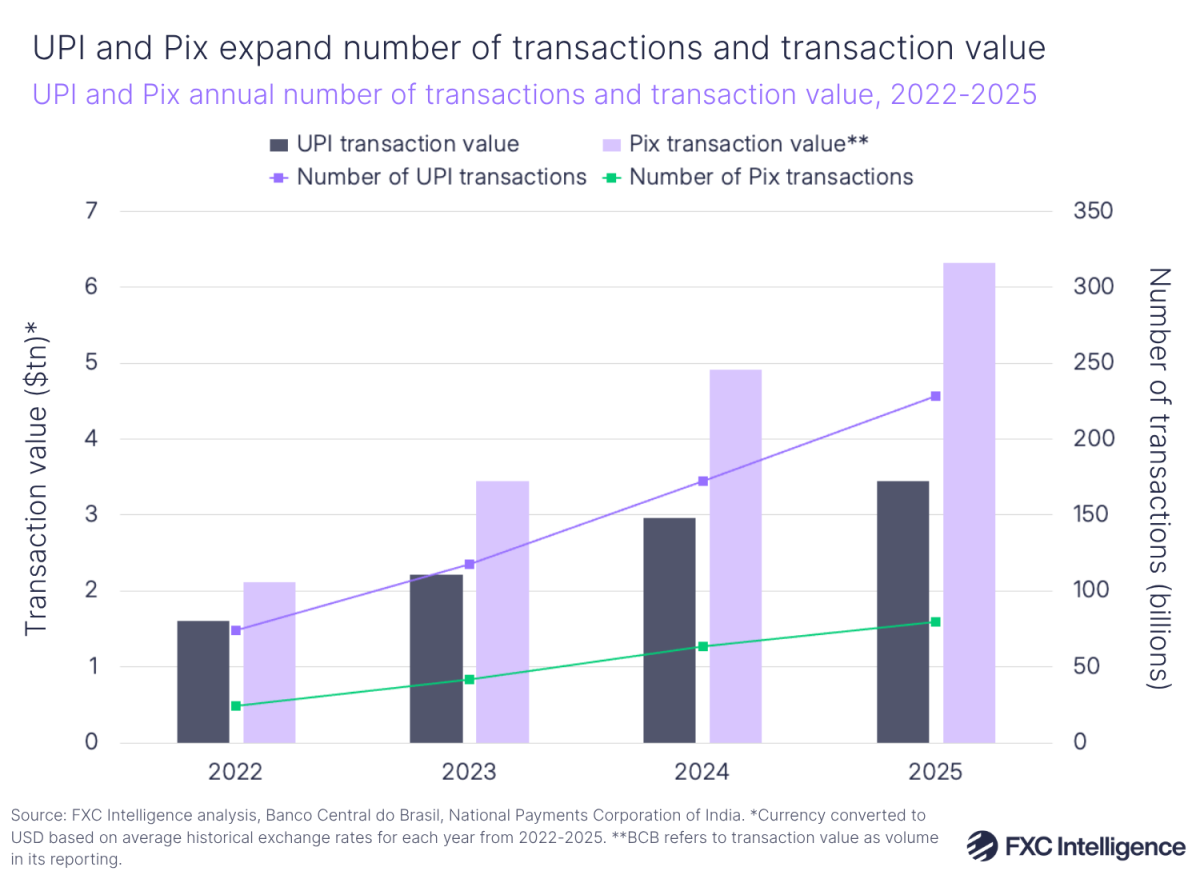

Transactions passing through Pix and UPI continued to grow in 2025, though not as fast as in previous years, suggesting the systems are now moving into a more mature phase. Based on our analysis, transactions passing through UPI in 2025 rose by 33% YoY to 228.3 billion, while the overall value of transactions rose by 21% to INR 299.7tn ($3.4tn). The faster growth for UPI transactions than the amount of money processed may reflect UPI’s role in enabling high-frequency, low-value payments in India.

Meanwhile, Pix’s transaction values (referred to as volume in BCBs reporting) grew 34% to BRL 35.3tn ($6.3tn) in 2025, while the number of transactions rose by 26% to 79.7 billion. A key driver has been the growing share of large Pix payments being made by businesses. This is shown by the BCB’s breakdown of Pix transactions processed through Sistema de Pagamentos Instantâneos (SPI), its core infrastructure which accounts for the majority of Pix transactions. SPI transactions occur through banks and other financial institutions that are direct participants in SPI, which means they are directly connected to the infrastructure and can initiate and settle payments on their own, while non-SPI transactions refer to payments institutions that are not direct participants, meaning they settle Pix transactions through intermediaries that are direct participants.

Despite only accounting for 4% of Pix SPI transactions in March 2026, the number of B2B Pix payments grew by 54% YoY and accounted for 52% of Pix’s total SPI transaction value. By comparison, P2B and P2P payments accounted for 46% and 40% of SPI transactions respectively, but make up an 11% and 24% share of overall transaction value.

Both Pix and UPI have added new features as they have developed, raising a question about both systems’ cross-border potential. The NPCI has enabled UPI to be used in other countries, with a specific focus on remittances from countries with large Indian diasporas, as well as Indian travellers paying abroad. NPCI has its own subsidiary, NPCI International, that is focused on expanding UPI acceptance in foreign countries, and in February 2026 piloted ‘UPI One World Wallet’, a payments service allowing foreign visitors to make UPI payments without needing an Indian mobile number or bank account.

Meanwhile, a specific timeline for linking Pix to other systems across borders has not been formalised, but the concept has been explored. Comments from former BCB President Roberto Campos Neto in 2023 suggested the bank was working towards enabling international transactions through Pix and the BCB is also working with more than 60 central banks on the Bank for International Settlements’ Project Nexus, which aims to create interoperability across instant payments globally. In the meantime, several payment providers have filled in the gap by launching international solutions that connect Pix’s domestic rails in Brazil to cross-border infrastructure. One example is PagBrasil, which through its International Pix solutions allows Brazilian consumers to use Pix in other countries, as well as allowing foreign travellers to use the payment method via their banking app while they are in Brazil.

For both UPI and Pix, current cross-border developments have been country-specific and focused on fulfilling demands of key regions for those countries. However, as these systems continue to prove out the strength of account-to-account payments in these markets, we may see them continue to expand their role in global payments through further integrations.