Standard Chartered remains one of the key banking players focused on cross-border payments. Despite interest rates continuing to affect its transaction banking services in Q4 2025, the bank reported growth in its Corporate and Investment Banking (CIB) division over the full year, with much of this driven by strength in its cross-border payments network.

Standard Chartered reported 6% growth in its overall full-year revenue to $20.9bn, while its CIB division, which is responsible for most of the bank’s cross-border income, saw revenue rise by 4% to $12.4bn (11% excluding the impact from interest rates).

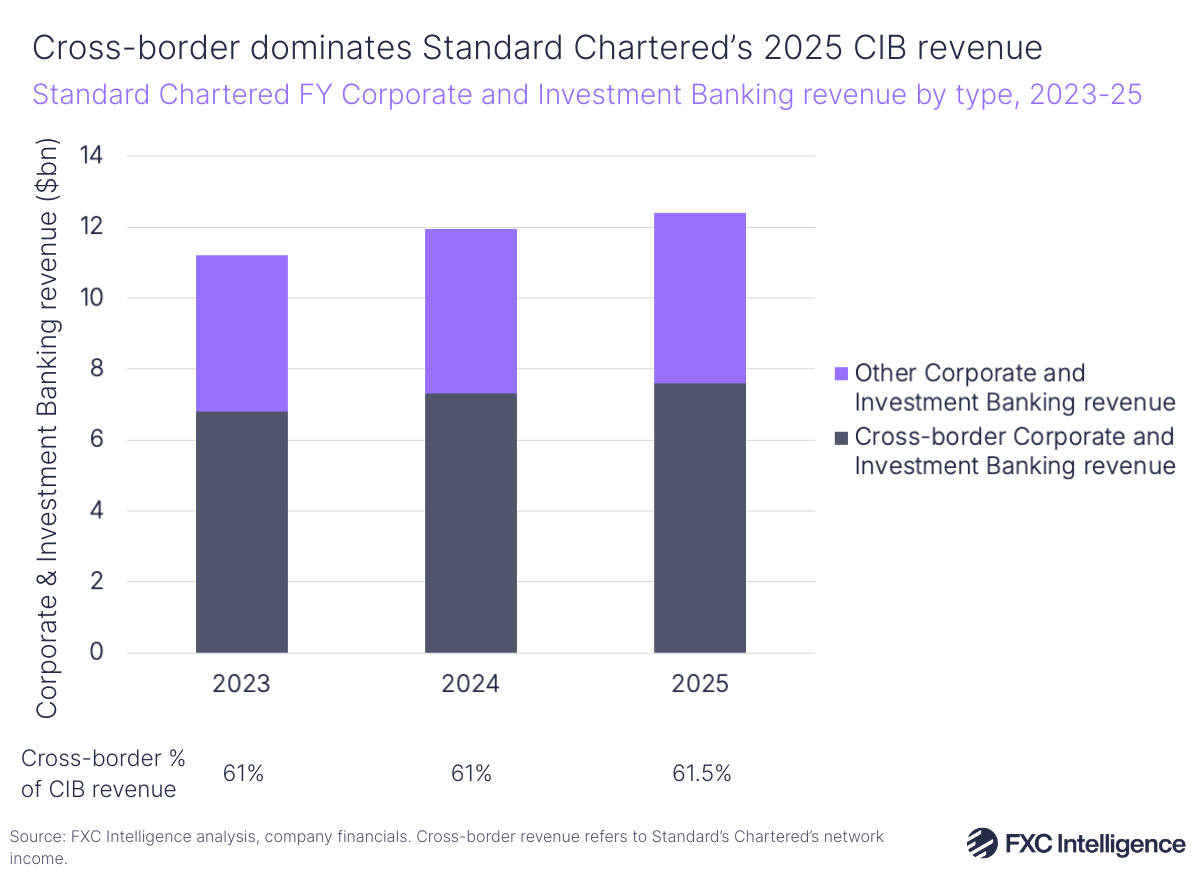

Cross-border revenue, which Standard Chartered refers to as network income, rose by 4% to $7.6bn in 2025, and has grown by a CAGR of 10% from 2019 to 2025. This meant it accounted for 61.5% of CIB revenue in 2025, slightly up from 61% the previous year. Standard Chartered restated its intention to drive network income to make up around 70% of CIB income in the medium term.

In total, 54% of CIB income was contributed by financial institutions, up from 51% the prior year and in line with Standard Chartered’s medium-term target of around 60%. It also met its goal to exit around 3,000 clients in 2025 to increase its focus on larger cross-border clients.

Despite CIB revenue in Q4 remaining flat compared to the previous year, the company did note that the share of this revenue attributed to network income was 67.4%, up from 63% in Q4 2024, highlighting the continued importance of cross-border to this division even as it faces headwinds.

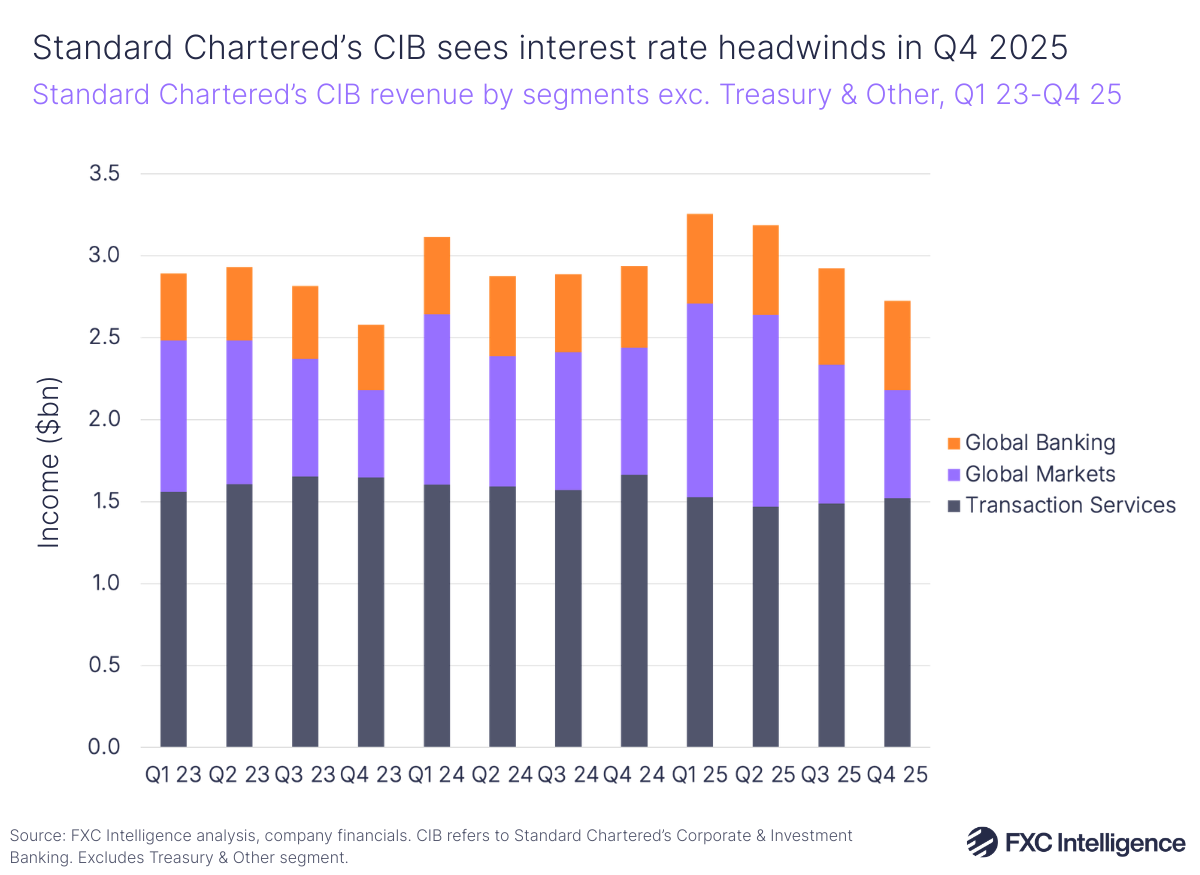

Revenue for Standard Chartered’s Transaction Services segment – the biggest contributor to CIB incomes by segment – declined by 9% in Q4 2025, driving an annual decline of 7% to $6bn. The biggest drop within this segment was seen in Payments & Liquidity, which saw revenue fall by 10% to $4.2bn in 2025. The bank linked this to lower interest rates and margin compression, which decrease the bank’s income from the segment even as flows rise.

On the other hand, Global Banking – Standard Chartered’s investment banking arm – saw revenue rise by 15% to $2.2bn in 2025. Global Markets, which comprises FX and risk management solutions, noted a 12% rise to $3.9bn in 2025 on the back of a 15% increase in flow income (day-to-day income from Global Markets services such as foreign exchange). Both of these segments also benefitted from growing trade and investment flows – in particular for countries in Africa and the Middle East (AME), with intra-AME network income rising 19%.

Despite the negative impact from lower interest rates affecting transaction services, Standard Chartered Group CEO Bill Winters said that the company’s network income global reach is benefitting the company as “Chinese and international corporates diversify manufacturing and shift their supply chains”. The bank noted growing activity for China to countries in the Association of Southeast Asian Nations (ASEAN), as well as China to Africa.