To mark the launch of Buyer’s Guide: Stablecoin Payment Infrastructure (learn more about purchasing a subscription or read the executive summary) we’re focusing on the technicalities behind stablecoin payments infrastructure. And this week, we’re moving on to stablecoin reserves.

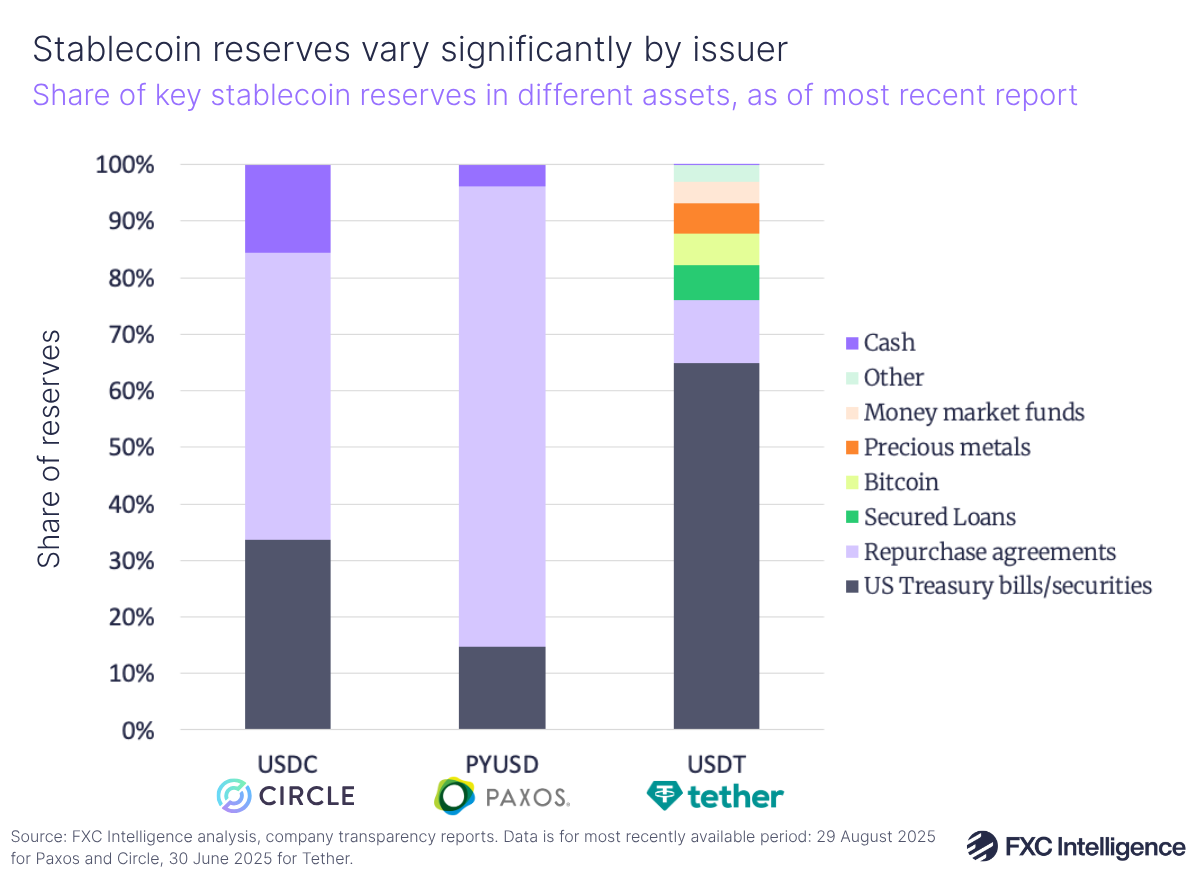

It’s fairly well understood that stablecoins are backed 1:1 with their equivalent fiat currency, however the nature of those reserves, how they are managed and why that matters is not always as clear. While it varies across different issuers, the majority of stablecoin reserves are not typically held in cash. As of the most recent transparency reports available, around 16% of Circle’s USDC reserves were in cash, while PayPal’s stablecoin PYUSD, which is issued by Paxos, held 4% of its reserves in cash. Tether-issued USDT, meanwhile, had less than 1% of its reserves in cash at the date of its last transparency report.

The most popular alternatives are US Treasury bills and repurchase agreements (short-term, collateralised loans based on US Treasury securities), and together with cash these make up the entirety of Circle and Paxos’s reserves, in compliance with the US GENIUS Act. However, Tether, which does not need to comply with the legislation, also holds some of its reserves in a variety of other forms, including bitcoin and precious metals.

Maintenance of stablecoin reserves is a careful balance between liquidity and earnings. Issuers need to be able to redeem stablecoins on demand, which requires ready cash, however interest earned on reserves is a critical source of revenue – and often, such as in the case of Circle, the primary source. As a result, issuers need to ensure enough cash is on hand to meet expected immediate demand, with some leeway to support unexpected surges, and store the rest in forms that can be easily redeemed but which they can earn greater yields on.

Short-term Treasury bills are a popular option because they can typically be liquidated within a day and mature quickly, with favourable yields. As of 29 August, for example, all of those held by Circle matured within three months. Repurchase agreements are similarly liquid, although in both bases funds cannot be released instantly. As Tether has a greater number of options for how it stores its reserves, it holds far less in cash, but similarly balances its reserves between liquidity and yield.

In order to ensure trust in a stablecoin’s reserves and comply with regulations, issuers typically hold reserves separate from corporate assets, such as via the Circle Reserve fund, and make use of third-party custodians, which in Circle’s case is BlackRock. Issuers also publish attestations of their reserve holdings and makeup from a third-party accounting firm, typically a Big Four company, each month, and undertake regular full audits of their financials.

However, despite this, there remain some potential risks. If there is a sudden very large surge in demand similar to a bank run, issuers could deplete their cash reserves and have to redeem other assets, which could cause delays in providing users with their funds. There is also a small risk associated with holding large amounts of cash too. In 2023, Circle very briefly saw the value of USDC detach from the dollar, known as a de-pegging, when Silicon Valley Bank – then a major holder of its cash funds – collapsed. This was resolved quickly, and Circle has since increased the robustness of its reserve security, however it does highlight potential challenges for issuers.

We’ll continue our look at stablecoin infrastructure next week. If you’re looking at adding stablecoins to your technology stack, FXC Buyer’s Guide: Stablecoin Payment Infrastructure is designed to identify best-in-class providers that fit your needs as well as helping you make sense of the market. Learn more about how it can help your organisation and express interest in purchasing a subscription.