With our Buyer’s Guide: Stablecoin Payment Infrastructure now being available to license (learn more about purchasing a subscription or read the executive summary), we’re unpacking the technical details behind stablecoin payments infrastructure. And this week, it’s time to focus on creation and redemption mechanics.

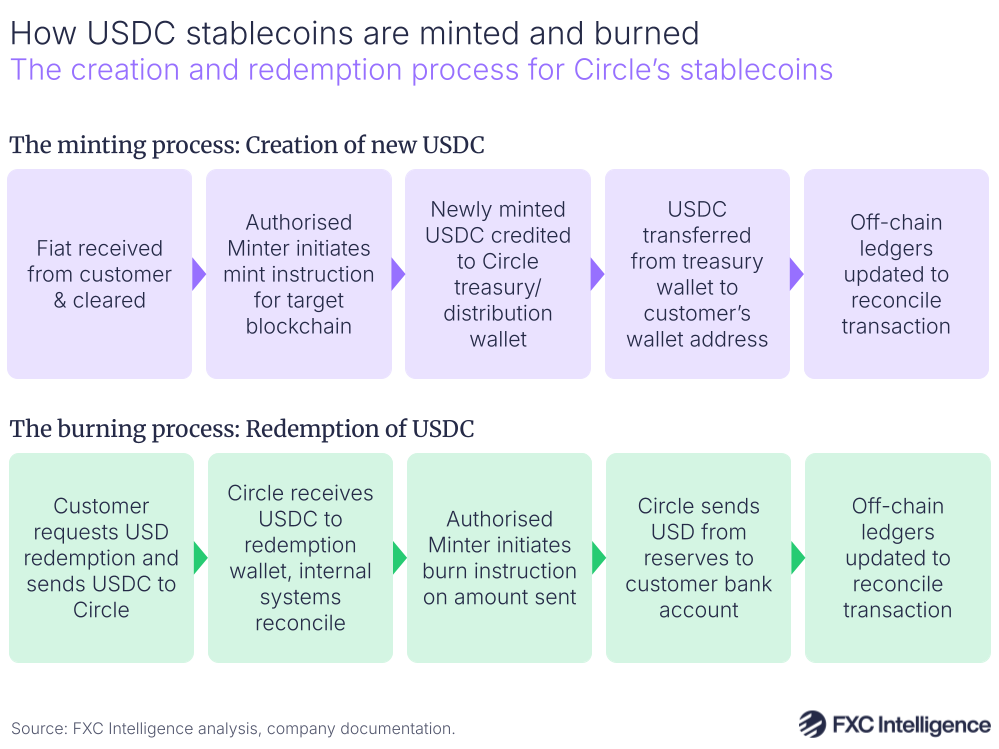

Stablecoins are pegged 1:1 with fiat currencies, but there are a number of crucial mechanisms to ensure their value is maintained. One is full reserves for their circulating supply, meaning that the issuer has enough money on hand to convert every single USDC, USDT or other stablecoin back into fiat currency if required. However, another absolutely critical element is the ability to create and destroy stablecoins as needed – processes known as minting and burning.

While this may sound fundamental, it needs to be executed correctly to maintain the integrity of a stablecoin. When new stablecoin tokens are created, they are ‘minted’ by an issuer upon receipt of the equivalent fiat currency from a user or institutional partner. However, when a user or institutional partner wants to redeem their stablecoin for its equivalent fiat currency, they can exchange it for fiat currency with the issuer who will ‘burn’ the token.

Each stablecoin token does not have a unique identifier, so in reality minting and burning adds or removes from the total supply, assigning or removing the value from the appropriate wallet in the process. When a stablecoin is minted, the issuer will typically first mint the tokens to their own internally controlled wallet and then transfer them to the customer’s address. Meanwhile, when stablecoins are burned, they are typically either moved to a dedicated redemption wallet and destroyed or moved to an inaccessible ‘black hole’ wallet.

It is important to note that while many payment players have direct connections to issuers such as Circle, Tether or Paxos to mint new stablecoins as required, this is not the only way to get stablecoins, and in many cases companies or users will instead opt to trade for existing stablecoins on exchanges or via partners instead. In this case, the stablecoin will move ownership but new tokens will not be created, meaning the overall supply will remain unchanged.

Lessons from the PYUSD accidental minting incident

The mint/burn approach ensures that the number of tokens in supply remain in line with the reserves the issuer holds, which is critical to the stablecoin’s integrity as a store of value. These processes are generally robust; typically only those with set administrative privileges are allowed to execute mints and burns as part of smart contracts.

However, there are occasional exceptions, the most notable being the 15 October incident involving PayPal’s stablecoin PYUSD. This saw its issuer Paxos accidentally mint $300tn – nearly twice the size of global GDP – of the stablecoin to one of its own wallets, before burning the same amount shortly afterwards.

Paxos confirmed that this was “an internal technical error” during “an internal transfer”, and although it has not published precise details, it is generally thought that this was the result of the wrong amount being entered as within a few hours the company minted $300m in PYUSD to the same internal wallet address.

While such incidents are extremely rare, they do happen occasionally, with the most notable other example being Tether’s 2019 accidental minting of $5bn, which it similarly burned soon after. As a result, the incident has raised questions about whether it should be possible to generate new tokens of a reserve-backed asset without new reserves to back it up, and whether there is a risk that this could occur with USDC. It is thought that while it may technically be possible for a similar error to happen with USDC under very specific circumstances, in reality this is very unlikely, with Circle’s controls to prevent such an occurrence thought to be more exhaustive than those of some of its competitors.

Meanwhile, an error involving burning too much of a stablecoin, rather than minting too much, is considered technically possible, but in reality is considered less likely due to multiple guardrails in place, including typically only being able to burn tokens held in an issuer’s own internal wallets or at addresses that have been frozen or blacklisted.

We’ll continue our look at stablecoin infrastructure next week. If you’re looking at adding stablecoins to your technology stack, FXC Buyer’s Guide: Stablecoin Payment Infrastructure is designed to identify best-in-class providers that fit your needs as well as helping you make sense of the market. Learn more about the guide’s independent, benchmarked vendor analysis and proprietary data, and how it can support confident stablecoin infrastructure decisions.