The global remittance market has been as noteworthy as ever in 2022. A variety of macroeconomic and geopolitical headwinds have had a large impact on the sector, and several look set to continue into 2023. However, there have also been positive shifts such as continuing improvements in transfer speeds.

The Russia-Ukraine conflict has resulted in millions of new migrants looking to send remittances. Alongside rising inflation and interest rates, the war has helped to fuel currency crises in a number of key remittance markets. Meanwhile, although Covid-19 lockdowns largely waned, their legacy is visible in an expanded digital footprint and the closure of some smaller operators.

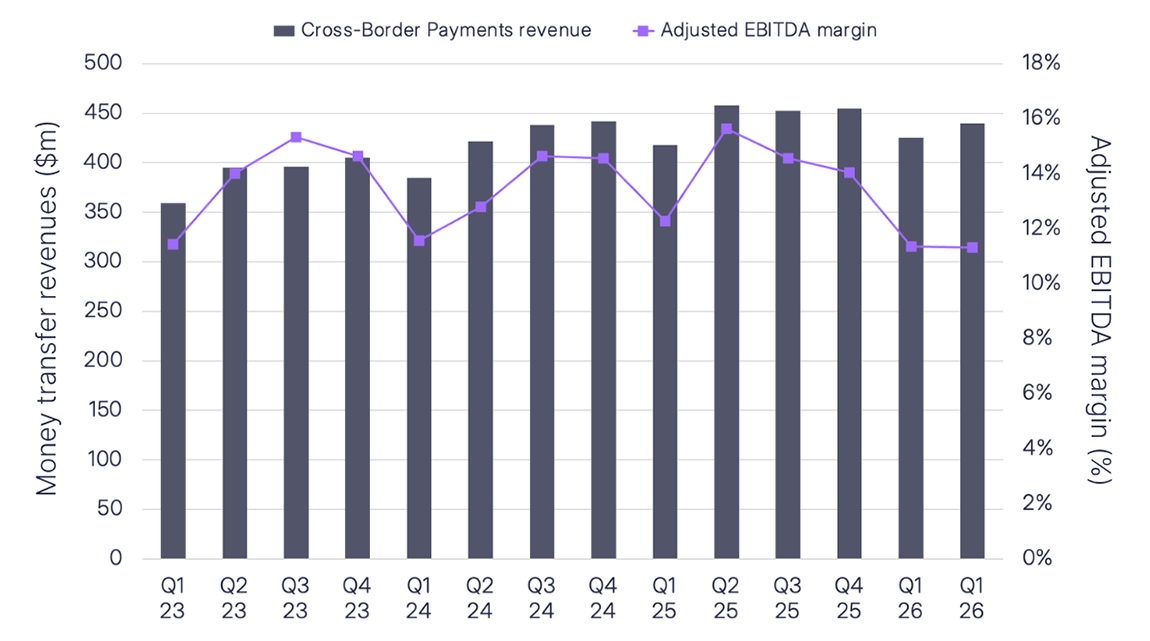

The overall cost of remittances to the largest receiving countries has stayed largely stable year-on-year, although there have been fluctuations in some markets.

The Russia-Ukraine conflict

The first quarter of 2022 ended with Russia’s invasion of Ukraine. Among other devastating consequences, it has also impacted Ukraine’s outflow of remittances and led to the introduction of economic sanctions against Russia that limit remittances to certain corridors. Some of these corridor changes include:

- Contact, Unistream and Zolotaya Korona have suspended transfers to Estonia, Latvia and Lithuania.

- Paysend initially only offered transfers from Russia to China, Tajikistan, Uzbekistan and the Kyrgyz Republic and eventually removed Russia from its sending countries altogether.

- Western Union suspended all services from Russia from 24 March 2022.

The conflict has also had a wider impact on the Eastern European and Central Asian regions. Countries such as the Kyrgyz Republic and Uzbekistan have dropped in competitiveness and have seen the price of remittances increase by 0.8 to 1.7 percentage points year on year. The Kyrgyz Republic moved from the 3rd least-costly country to receive remittances down to the 17th.

On the other hand, many operators have introduced promotions and reduced fees throughout the year to facilitate transfers to Ukraine, as well as neighbouring Poland. Prices for remittances towards the two countries are 0.3-0.7 percentage points cheaper overall and the countries’ respective rankings in regards to the cost of sending have also improved – Ukraine, for example, has moved from the 27th least-costly country to receive remittances up to the 15th.

Economic and currency crises

Geopolitical tensions and macroeconomic instability often create dysfunctional currency markets, resulting in parallel exchange rates used for FX transactions. Remittance providers respond by adjusting their margins to the local parallel exchange rates rather than the official exchange rates, creating biased pricing and generating considerably negative margins on certain services. Some of the markets that have experienced particular challenges include:

- Bangladesh has experienced high volatility in the foreign-exchange market, resulting from a shortage in foreign reserves starting in the second quarter of 2022. A new initiative has recently been launched by the government whereby all direct transfers into the country will receive an additional 2.5% straight to the recipient’s account; it is hoped this will encourage more transfers through legal channels as the price of USD has reached BDT 120 in the unofficial parallel market. Transfers into the country remain very competitive as Bangladesh has the lowest overall pricing in 2022.

- Pakistan continues to be strongly affected by the balance of payment crisis, while the government has restricted all outflows of currency from the country. Some outbound remittances are possible under extenuating circumstances such as medical and educational purposes; other transfers can only be sent if both the sender and the receiver have a domiciliary account in foreign currency. Nonetheless, remitting to Pakistan has become more competitive, as prices have marginally decreased year-on-year, and the country became the third least-expensive country to receive money in 2022.

- Nigeria experiences continuous shortages of foreign reserves and a depreciation of the naira in the unofficial parallel market. Similar to Pakistan, outbound remittances are limited to transfers where the sender and receiver have a domiciliary account in USD. This is part of the Central Bank of Nigeria’s plan, announced in December 2020, which aims to improve the efficiency of the foreign exchange market and provide more liquidity. Despite some of these challenges, the prices of money transfers to Nigeria have largely stayed the same year-on-year.

- Lebanon is similarly experiencing an ongoing economic crisis, exacerbated by the Covid-19 pandemic, resulting in foreign currency liquidity shortages. Remittance prices have marginally increased year-on-year and Lebanon remains the most costly of the major remittance markets. Additionally, providers are substituting the Lebanese pound with USD as the principal payout currency for remittances to Lebanon.

- Sri Lanka’s economic difficulties continued from last year, meaning ongoing pressure on the rupee. The country moved from the 7th least-costly country to send remittances down to the 11th in 2022.

- Yemen continues to face a humanitarian crisis as a result of the civil war and parallel FX rates remain prominent. The overall cost of sending remittances to Yemen has decreased since 2021 and is reflected in its improved ranking to the 7th most competitive country to receive money transfers in 2022.

Covid-19, transfer speeds and changing payment methods

Covid-19

During the peak of the Covid-19 pandemic, many operators and banks limited their remittances services. Some banks closed their branches, while other providers stopped dealing with cash payments to limit the spread of the virus. In 2022, much of Covid’s impact on the sector has waned as providers either resumed their operations or closed altogether.

Speed of transfer

The speed of transfer from the sender has increased to almost all key remittance receiving countries year-on-year. We expect this is part of ongoing improvements in providers’ digital offerings.

Payment methods

Throughout 2022, we have noted that fewer providers are allowing credit cards to be used to fund transfers. This trend is especially notable for sending from the US, where interchange fees are significantly higher than Europe, where prices are capped.

For example, in the US, Walmart2World stopped accepting credit cards at agents’ locations at the tail end of 2021 and Pangea followed suit in 2022. By Q4 2022, SmallWorld only accepted payments by debit card in the US.

Looking forward to 2023

The current economic headwinds and ongoing crises are likely to continue into 2023, meaning that further changes can be expected in the coming year. In particular, we expect to see more changes in pricing to key markets over the next 12 months as countries and providers respond to these continued headwinds.

However, we can also expect other developments to shape remittances. Further improvements in the speed of transfers is likely to enhance the remittance experience on certain corridors. We also expect there to be a continued shift to alternative payment methods such as digital wallets in 2023.