Recent world events and increased geopolitical tensions have renewed conversations across the globe about reducing reliance on the US dollar. China in particular has promoted usage of the yuan and has reduced US dollar volumes flowing in and out of the country in recent years.

According to the Bank for International Settlements (BIS), the yuan made up just 9% of global FX volumes in 2025, while the US dollar accounted for 89%. Despite this disparity, China is actively engaging in efforts to reduce its reliance on the US dollar – something that can clearly be seen in its non-bank cross-border payment volumes.

China’s State Administration of Foreign Exchange shares monthly data on outbound and inbound non-bank cross-border payments, showing that since 2017 yuan usage has grown significantly in transactions in both directions.

Since March 2023, the yuan has made up a larger share of outbound payments from China than any other currency, accounting for over 50% each month in 2025, while the US dollar fluctuated around the 40% mark. For inbound payments to China, the dominant currency has shifted month-by-month throughout 2025 between the US dollar and the yuan.

Looking at China’s non-bank outbound cross-border payment volumes for the whole of 2025, the yuan increased its share by 1.7% YoY to 53.9% while the US dollar fell 1.2% to 40.5%. The yuan also remained dominant for inbound payments to China despite a marginal YoY increase for the US dollar – sitting at 49.5% and 46.7% respectively.

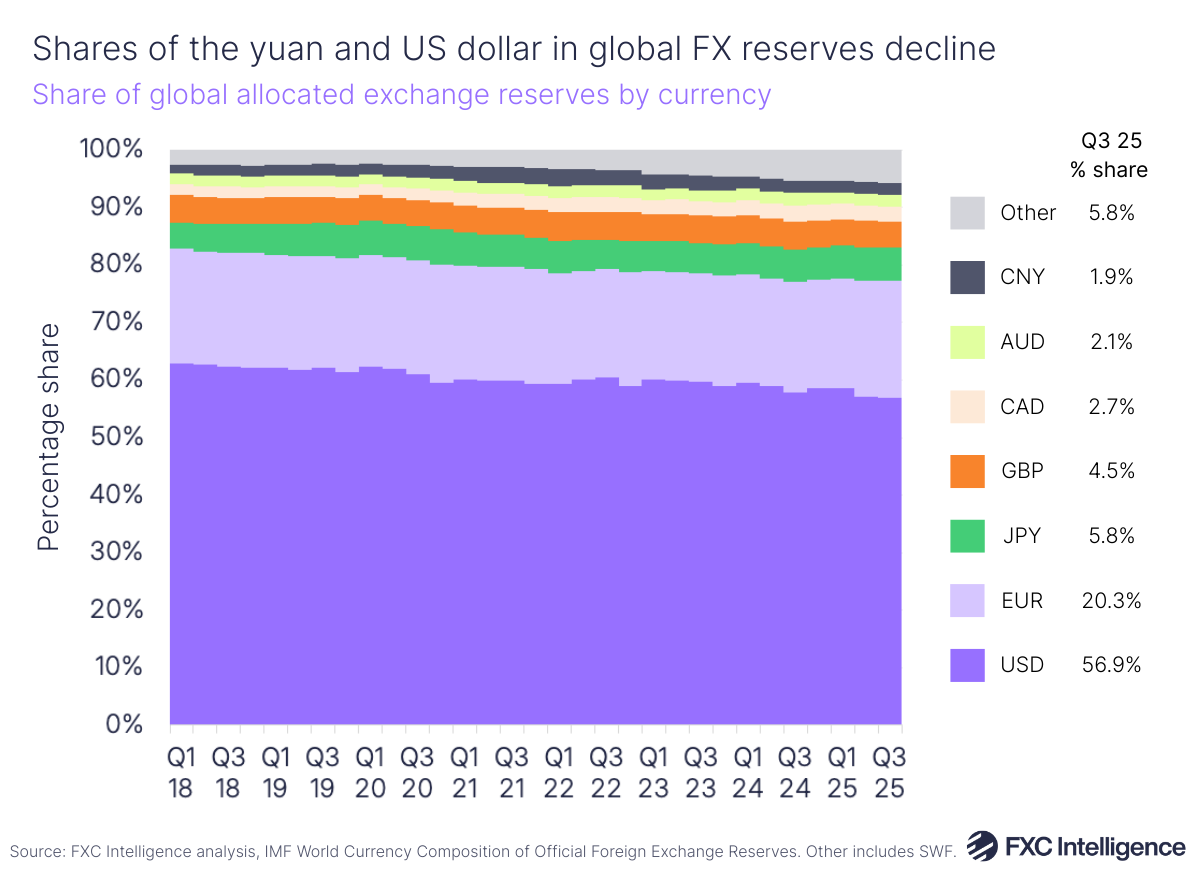

Despite continued success for the yuan for cross-border payments in and out of China, the currency has failed to make similar progress on a more global scale. According to the IMF, in Q3 2025, the most recent period data is available for, $251bn of global allocated foreign exchange reserves were held in yuan. This represents a 1.9% share of the $13tn total of allocated reserves – a 0.2% decrease YoY.

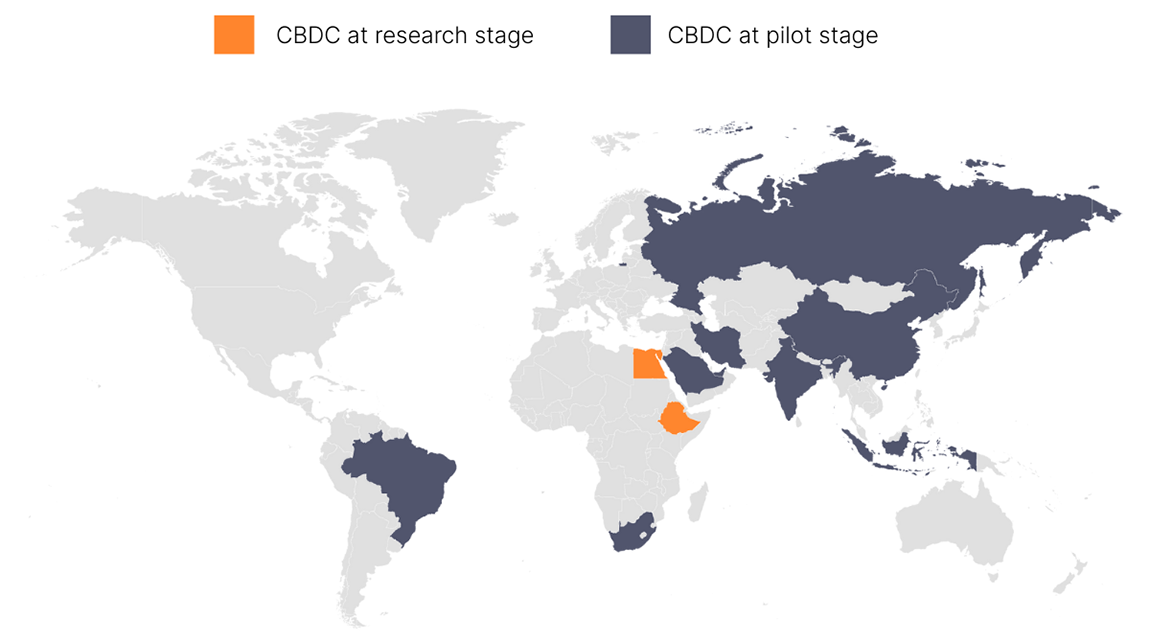

Although the yuan’s share is yet to increase significantly, efforts to strengthen its influence both domestically and internationally continue, particularly as global confidence in the US dollar wanes. The People’s Bank of China (PBOC) began paying interest on digital yuan balances on 1 January 2026, becoming the first CBDC globally to do so and moving away from the widely selected non-interest-bearing models for CBDCs elsewhere. Days later, the PBOC discussed plans to improve infrastructure to support cross-border yuan usage and explained that it would encourage its financial institutions to improve their cross-border financial services. Through these efforts, China is looking to increase global usage of its currency, bolstering its influence and reducing costs for Chinese companies.