In January, Reuters reported that India’s central bank could soon make a new payments proposal for countries in BRICS – the intergovernmental organisation comprising Brazil, Russia, China, India, South Africa and several other countries. Under the proposal for BRICS’s next summit, these countries would link their established central bank digital currencies (CBDCs) to enable easier cross-border trade.

BRICS has long been rumoured to have aspirations to create a single unified payment system, but what can the cross-border payment space take away from recent developments in the bloc?

BRICS countries have for years discussed potential systems that could make it easier to move currencies across borders. These include BRICS Pay, a decentralised cross-border payments messaging framework for BRICS+ countries (i.e. including the 11 BRICS nations and nine partner nations); BRICS Bridge, which would use distributed ledger technology to enable local currency transactions; and BRICS Clear, a system allowing direct settlement of cross-border transactions.

If the reported proposal from the Reserve Bank of India goes ahead, it will appear to represent another move to create a region-focused alternative cross-border payments system, with some reports linking it to the BRICS Bridge concept. This would be similar to the mBridge platform currently being tested by central banks in China, Hong Kong, Thailand, the UAE and Saudi Arabia. It will also build on a 2025 declaration at BRICS’s summit in Brazil, which saw members push for interoperability between payment systems to speed up cross-border transactions.

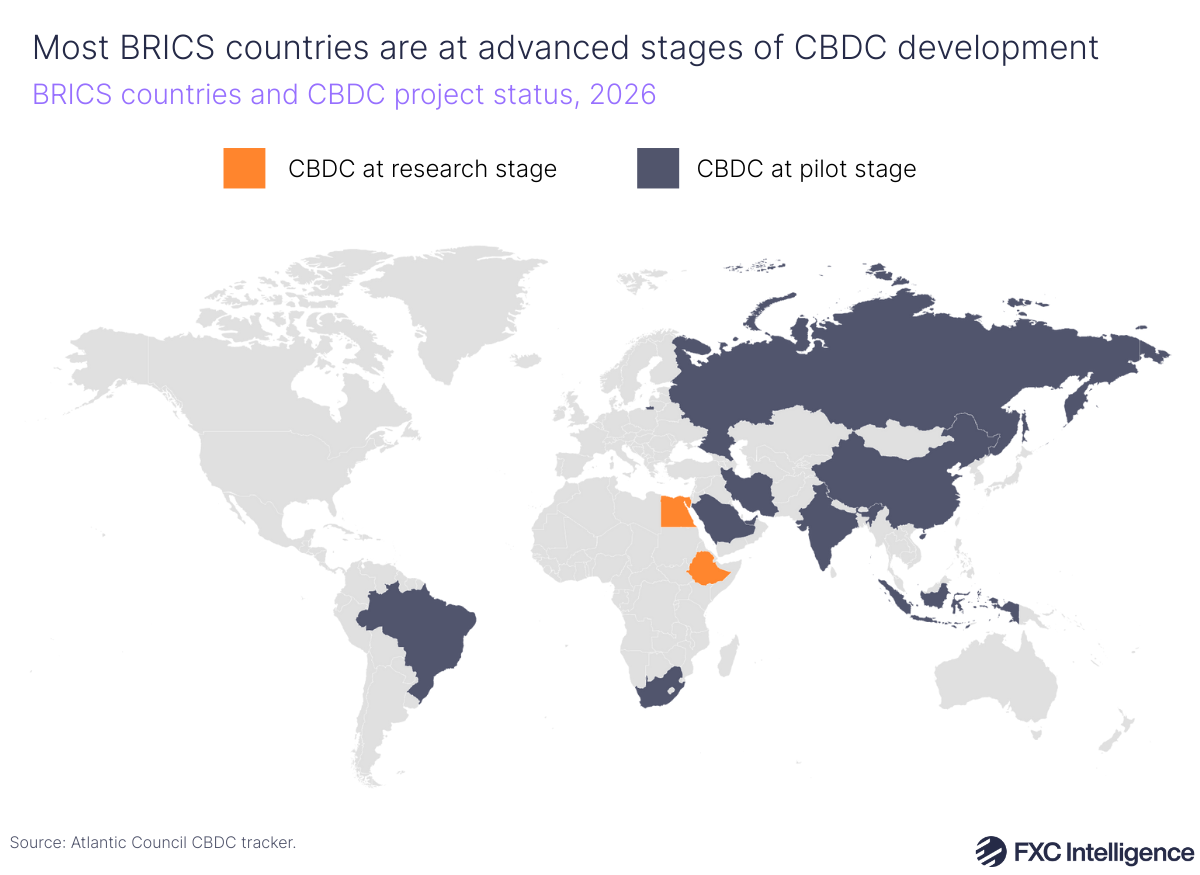

Several countries within the BRICS network are at relatively advanced stages of CBDC developments compared to other countries globally, with China, India and Brazil all having run pilots of their respective CBDCs. Linking these currencies would theoretically enable faster movement and settlement of currencies in local systems, allowing the countries to bypass traditional correspondent banking networks using Swift.

While development and discussion around these payment concepts continue to evolve, they serve to highlight how payment systems globally could grow more fragmented based on geopolitics. The world’s dominant rails for moving money across borders, including correspondent banking networks and Swift, remain strongly embedded in cross-border payments and are largely owned or managed by parties in Western countries.

By implementing systems that focus on trading through local currencies, countries within BRICS would be able to reduce the need to rely on the US dollar to enable FX trades through correspondent banks, as well as their exposure to sanctions that Western countries can place on those systems – the most significant example of this was Russia being banned from Swift in 2022.

The proposal of linking CBDCs across BRICS is still a reported item for discussion rather than a fully confirmed plan, and would rely on several things happening. One source told Reuters that it would require agreements about interoperable technology, as well as how the system is governed. Countries would also have to agree on how to settle imbalanced trade volumes, with one potential solution being bilateral FX swap arrangements between central banks. All of these systems would require consensus and could take time to develop, which has been a significant challenge since BRICS first proposed its cross-border initiative back in 2015.

In the case of BRICS, moving towards interoperability would rely not just on agreement between countries, but also whether they are individually able to successfully introduce CBDCs for payments. Having said this, for the wider cross-border payments industry, the recent developments with BRICS highlight the growing interest in interoperability between payment systems within specific regional blocs, particularly during a period of significant geopolitical upheaval.

For cross-border payment providers, staying aware of developments across regions such as BRICS will be crucial for their strategy, particularly as more systems emerge that move outside traditional banking networks. In these cases, building more partnerships to ensure interoperability across corridors will be even more important.