FXC Intelligence’s Daniel Webber spoke to Raj Agrawal, CFO of Western Union, about the company’s FY 2020 earnings results, digital focus and future plans.

2020 hasn’t been an easy year for many companies in the remittance space, but Western Union has still posted strong year-end results.

The headline-catching number for Western Union in 2020 is the $10bn in cross-border principal it added through the year, driven by its digital business. This is against the context of a pandemic-shrunk market, down 7% according to the World Bank.

Amidst a changing – and increasingly digital – climate, Western Union has been tasked with maintaining and growing its presence around the world and becoming a platform. But how did it achieve its 2020 results, and what lies ahead?

FXC Intelligence CEO Daniel Webber had a detailed discussion with Western Union CFO Raj Agrawal to find out more.

Topics covered:

- Drivers of cross-border principal growth

- The growth in account-to-account customers

- Western Union as a platform for banks and fintechs

- Walmart and exclusive vs non-exclusive agent relationships

- Digital and total customer counts

- The mobile wallet opportunity

- Trends in pricing

Drivers of cross-border principal growth

Daniel Webber: Firstly, well done. It’s not been the easiest of years with a sector that has shrunk in the year. Let’s start from the top line: that’s a very nice jump on the principal side. What do you think has really driven the increase in the principal?

Raj Agrawal:

Thanks for noticing. We’re very pleased with the results that we had last year. We were all dealing with a high level of uncertainty as we came into the second quarter of last year, so none of us knew exactly how things were going to play out.

To our satisfaction, the business, after declining bidding in the second quarter, had rebounded very nicely from the retail business standpoint. And we continue to have very strong digital growth.

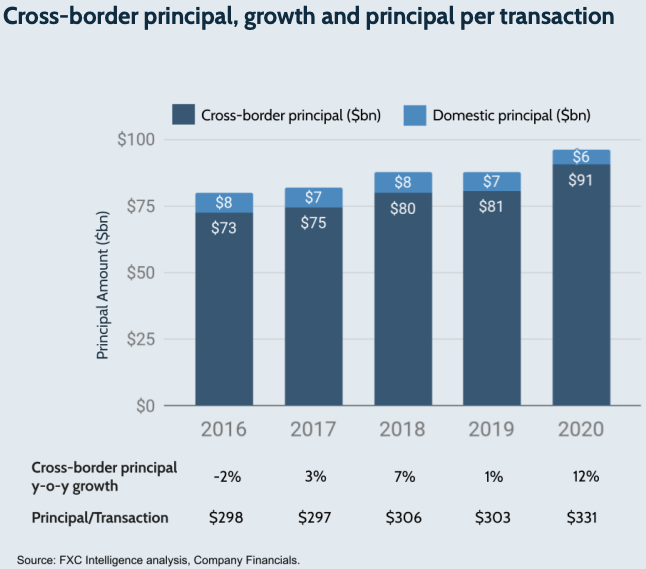

Our cross-border principal grew by 12% last year. And that is in comparison to the public estimate of minus seven from the World Bank, which they’ve [since] revised. They revise it typically a couple of times a year, so I imagine that we’ll continue to see revisions to what happened last year, because they continue to collect a bunch of data points.

We see it real-time in our business plans, what’s happened. And the digital part of the market was clearly one of the key growth drivers in the overall cross-border principals. That really was a star performer for the market and also a star performer for our own business.

However, retail continued to stabilise, so what we saw last year is that as we came into the second quarter, retail started to dip down quite a bit, but digital started to take off. And we were really well positioned with our digital business; we had already gotten into 75 send countries with our WU.com business.

We had a number of great digital partnerships. We had a lot of different connection points with account funding, and account payout. And we were really well positioned to capture, to catch if you will, all the customers looking for us in the digital space.

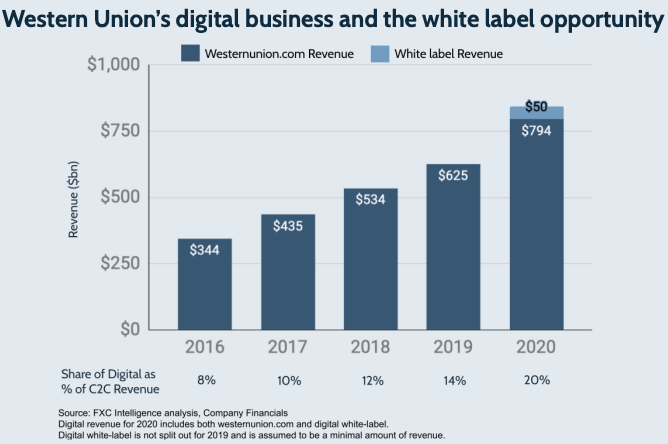

Not only did our retail business stabilise as we went through the course of the year, in the second half of last year, but we also continued to see very strong digital growth. This year we now see the digital business getting to be about a billion dollars.

The World Bank’s last estimate is, again, minus seven for this year. We think that that may be a little bit pessimistic, but we’ll see where they come out.

We still see our share growing again this year, for the same reasons. The digital is going to continue to grow. We see a retail business that is going to rebound this year. So we really positioned ourselves well as we come into this year.

Figure 1

Daniel Webber: You’ve added about $10bn of cross-border principal. There’s a lot of players in this space that don’t have $10bn of principal in total. Who do you think you’re taking that share from?

Raj Agrawal:

The market is comprised of three basic components. The biggest share of the cross-border remittance market, about half, is with the banks, because many people use their banks for moving money around the world. The other 50% is split between the traditional money remitters, so the traditional space that we’ve operated in, retail mostly. And then another 20% is with the digital players.

The people that are visiting our business are coming from the banks, because they were looking for online options, and from the other digital players.

And if you really think about what the banks are doing, we actually could be a provider for cross-border remittance services for the banks. We already are today, in our retail business. 70%, or I would say two thirds of our network globally, is made up of banks and post banks, and financial institutions.

And we have a number of fast-growing digital partnerships, for example with Saudi Telecom in Saudi Arabia. We also have our Sberbank relationship in Russia. Sberbank has been using the correspondent banking system to move money around the world for their customers.

But now that they’ve partnered with us, overnight, they got the ability to move money all around the world into 200 countries and territories in a real-time manner, because we can basically deliver money in minutes, all around the world at a retail location.

Banks that are also players in the cross-border remittance market may actually want to look at someone like Western Union that can provide a turnkey solution for them; something that’s better than what they currently use.

The growth in account-to-account customers

Daniel Webber: Bank to bank, account to account, is probably one of your fastest growing segments, driving the higher principal per transaction. Can you add colour around what that customer is like?

Raj Agrawal:

There are multiple factors in why the principal amount per transaction is at a higher level. It was up almost 10% last year, because of everything we saw. So, there are different things going on.

People who are remaining in our business, those are the people who have the higher ability to send, typically. They’re sending a higher principal amount, they’re sending it more frequently, and the needs to receive money around the world are higher than ever before.

I know it because I also use our business, I’m a Western Union customer. I use my mobile app to move money from the US to my relatives in India. And I sent more money over the last 12 months than I ever have before, to my loved ones, because either the travel industry is down or tourism is down.

So, the customer is sending a higher principal amount, because they are the ones who have the ability to send, and their recipients need money more than ever before.

Secondly, we have typically seen the principal amount going into accounts be double the normal amount of principal. Why is that the case?

Because money that’s going into an account is going to sit there for a while. It’s not for an immediate need, it’s something that’s going to be drawn down over time.

The recipients typically will use this for their ongoing expenses, or they’re improving something in their home, or whatever that might be. So money that’s touching their bank account is going to typically be at a much higher principal amount than we’ve seen in our traditional business, if you will.

Daniel Webber: Companies such as TransferWise, for example, have always been focused on account-to-account. Their average principal number is a couple of orders of magnitude larger than that principal that you just referenced.

Do you see Western Union beginning to focus more on that sort of customer: the white-collar, expat migrant worker, as opposed to the remittance migrant worker?

Raj Agrawal:

I really believe that Western Union is going to be the winner in the account-to-account space, and the online to account space, because we do what we do today on a global basis. We’re not just a corridor player; we do it in 200 countries and territories, and we’re absolutely going after the account-to-account segment.

I mentioned that half of the remittance market is with the banks. We really believe that we can be the backend provider to these banks, and we can do it in a branded way or non-branded way. It really just depends on what the partner wants.

We have already very strong capabilities, we have online sending capabilities in 75 send countries. I don’t know of any competitor that has that sort of breadth in terms of the ability to send. We have the ability for people to use their mobile devices in over 50 of those countries, so they can use their mobile device to do the transaction.

We can deliver money real-time into more than a hundred countries into an account, and many more just generally into the account system. Our goal ultimately is to be an omni-channel player, both sending and receiving.

We want the customer to be able to transact with us in whichever way is convenient to them on the sending side. So use their bank, use our online business, use our mobile app, use the walk-in location that may be convenient for them. And then pay out to a retail location if that’s how their recipient wants to get the money, or pay out to our great account payout network, which is also a way customers are using us.

They’re using us for different things. Every single customer has multiple needs, it’s not just the same need. So we’re going after a broad customer base, whether as you said, they’re the white-collar migrant or the blue-collar migrant, we don’t really care.

We just want them to use our business in whatever way is convenient for them, retail, digital on sending side, and retail and digital on the receiving side. And that’s really our vision, is to do that.

We already cover much of the world. Other players may have a better offering in a couple of markets or a couple of quarters. We are talking about a global business all around the world.

Western Union as a platform for banks and fintechs

Daniel Webber: I think you want to go down more the platform route, which is you’d rather be the full backend to the bank: not have to individually go after the customers, but just do the deal with the bank and then all their customers flow through you. And I think you said on many earnings calls, that the economics, the online margin of that is actually very healthy.

Even if the top line and bottom line look different, the online margin is the same. And I will further say, the valuation of your company as a platform play is more valuable than one having to go after top-line marketing spend. What are your thoughts on this?

Raj Agrawal:

You took the words out of my mouth. We are absolutely a platform player, and we’ve been that, and we’re going to continue to be a platform player and we can do even more.

I believe that a lot of well-known partners are understanding our capabilities. Amazon is not necessarily a big revenue provider for us today, but it’s a great example of how we can use our capabilities and services in a lot of different ways.

La Banque Postale in France doesn’t work with us because they like us. They like us also, but we provide a great service for their customers. Or Saudi Telecom in Saudi Arabia, we are really a white-label provider for their customers to do cross-border remittance services. So, we really believe that we can offer customers in both a branded and a non-branded way, and be very much a platform provider.

We’re now going into the Walmart stores, beginning of the spring of this year. Why is that? We’ve had a chance to go into Walmart stores before, but it was the right timing for us, because we are very much a platform provider of our services. And we believe that we’re going to win at the point of sale, even in a place like Walmart.

Walmart understands our strong capabilities. They know that we have great regulatory and compliance capabilities, they know that we can do global business, they know that we have a great distribution system, and they want to tap into that because they know that that’s what their customers want.

Customers recognise the Western Union brand, so we believe that we’re going to be winning in that relationship, vis-a-vis the other players that are there as well. So, absolutely. We really think we can provide services in a whole host of ways that we may not have done in the past.

Figure 2

Walmart & exclusive vs non-exclusive agent relationships

Daniel Webber: On the subject of Walmart, maybe you’re going to think about some of your physical location strategy slightly differently now, as opposed to one that used to be very exclusivity-driven. By definition, Walmart is a non-exclusive, but it’s a very big channel. Is there any colour you can add around how you’re thinking about that?

Raj Agrawal:

We’re really going after a lot of different kinds of accounts, and not every single account wants to use our services in the same way. Walmart has certain objectives, Saudi Telecom has certain objectives, Kroger has certain objectives, or you have a La Banque Postale who has certain objectives.

So we want to be able to be flexible to all those different kinds of partners, and we really ultimately make our decision based on the economics around something. Is Western Union going to be able to provide a differentiated service at the point of sale, and can we make money at it, and is it a good long-term relationship? Those are sort of the things we look at when we go into a partnership. It’s not just about is it exclusive or non-exclusive, because most of our network is still exclusive around the world, the key sending geographies, except for Russia and the Gulf states.

But then we have many examples of non-exclusive relationships all over the world as well, because it works for us, it works for the partner. In Africa, for example, we have many non-exclusive relationships, because you’re not allowed in most cases, the banks that we work with are not allowed to contractually have an exclusive relationship with us.

However, it doesn’t mean that they can’t work with us exclusively, because we have a gold standard, we have a silver standard and a bronze standard. And we may pay different commissions depending on the kind of relationship we have with them, although we don’t contractually require an exclusive relationship.

Because we operate in 200 markets, we’re always evaluating: what does the market require? What’s the best outcome for Western Union? What are the other channel distribution opportunities for us and our partners? So, it’s not such a simple decision around one factor, it’s many factors that we have to take into account.

Digital and total customer counts

Daniel Webber: 8.6 million is your first official print of a digital customer count. Is that 8.6 million sending, or is that 8.6 million on both sides of the transaction?

Raj Agrawal:

Yes, this would be more of a sending number.

Daniel Webber: 65 million was the number that I know was put out a couple of years ago at the investor day, now there’s 150 million – is that total customers?

Raj Agrawal:

Yeah, 150 million total customers; about half of them are senders and half are receivers. With the WU.com business, we’re just trying to highlight the sending capabilities we have and the sending customer, because that’s who we’re trying to acquire here and that’s who we create the account relationship with.

What’s really interesting, Daniel, is that one thing that we’re going to be testing out this year is much more of an account relationship that goes deeper with the sending customer. Can you imagine if Western Union could actually provide other kinds of products and services to their customer base?

Because customers, they love the Western Union brand, they trust us. So, why couldn’t we go get more share of their wallet, for other things that would be sort of connected to the kinds of things they do with Western Union anyway?

We have the Western Union bank in Austria, and we’re going to be testing out some very basic financial services offerings with customers later this year. I put myself in the shoes of a customer because I am a customer, but I would love to have an account, like a bank account relationship with Western Union where I could maybe store money, I can use that money to send to my loved one. I don’t have to necessarily get it from my separate bank account.

Maybe my recipient also has an account relationship with Western Union, which is something we haven’t done before here. The recipient having the same kind of bank account, type of relationship, where maybe I can move money between us very easily, or maybe my recipient can draw money every month as they need the money.

There are lots of different use cases here, of how we can extend the relationship that we have today in the digital world. And Western Union is better positioned to do that than anyone else, because of the brand strength we have.

We’re going after we’re going after the migrant community, in terms of providing more value to them in the kinds of things that they’re already doing. So, they’re already using our business in a transactional way.

We want it to be an ongoing relationship, where they’re very sticky customers and we’re providing them all these other kinds of services that might be connected to their remittance offering.

The mobile wallet opportunity

Daniel Webber: You’ve expanded a lot on the wallet side and the payout outside, as well, right? Which I guess is also possibly seeding a Western Union wallet eventually in some markets; that’s the logical step.

Raj Agrawal:

Absolutely. You don’t need it everywhere, because not every country that would work well. But in many places it would work really well. I would love it if I could send money to pay the bills of my relatives directly, if they somehow connect it to their account with Western Union.

There are lots of things that we’re just thinking through, and we’ll have a lot more to say about it, hopefully by the end of this year, on how that testing is going. Because that could be the next evolution for Western Union: more services for the customers that we have today on the branded side. On the non-branded side, we want to package our capabilities and offer it on a white-label basis, so really going after both areas.

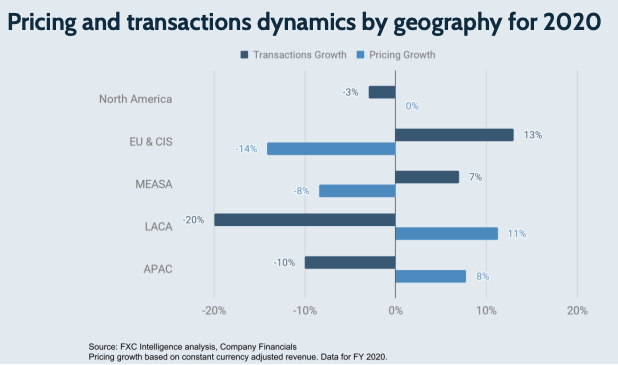

Trends in pricing

Daniel Webber: Let’s just talk quickly about pricing. Maybe you can help us strip out a little bit of the white label. Because obviously the white label stuff is in a lot of the numbers, and so any colour you can show on the pricing trends, aside from the white labels, or maybe the retail and the digital side, that would be interesting.

Raj Agrawal:

You’ve done your homework, obviously, you’ve seen how much the white label business is skewing the numbers, and that’s really a mixed impact more than anything else.

Beyond that, I would just say that look, the overall pricing environment around the world continues to be very stable in nature. We haven’t seen any significant pricing pressure, when you look at our business on a global macro basis. Having said that, we have 20,000 corridors, where customers are sending money from and to, and we’re always moving pricing up and down.

Our ultimate objective is to acquire more customers, and build the funnel of customers because that really becomes the lifeblood of how the company reforms in the future. And that’s really been the strategy around WU.com, for example.

Last year, we were doing dynamic pricing in our WU.com business, to really go after more customer acquisition. Because customers last year were looking for a way to send money online, and we wanted to catch their attention, we wanted to catch those customers.

We had promotional pricing, and we had various kinds of strategic pricing that we put in place. And that’s really what led to the 30% growth in this 8.6 million customer number, is because of that dynamic pricing strategy. What I can tell you is that we wouldn’t be able to get to a billion dollars of revenue in our digital business.

Figure 3

Daniel Webber: If the price was zero, there wouldn’t be any revenue.

Raj Agrawal:

Exactly. We’re doing things in the right way there. And retail continues to come back, we think our retail business is going to rebound this year and have some growth. All of those things are really fitting in nicely.

The thing I would leave you with, is that we really believe that we improved our competitive positioning last year, given everything that was going on. Because we had the ability to keep investing, we had the ability to withstand some of these market pressures, and we’ve come out on the winning end, I believe, with the share gains that we had last year.

I really think we’re better positioned today, competitively speaking, than we were at the beginning of 2020.

Daniel Webber: Raj, this has been great. Thank you for the time.

Raj Agrawal:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.