A report exploring the current and future state of BNPL, in light of market downturns and the launch of Apple Pay Later.

For many consumers globally, the options for non-cash payments have traditionally been between credit and debit. However, the last decade has seen payment methods evolve significantly, particularly for ecommerce, including with the emergence of buy now, pay later (BNPL).

Also known as alternative financing at point of sale, BNPL first emerged a decade ago, with early entrants including Splitit and Affirm in the US, KueskiPay in Mexico and Alma in France. However, the pandemic-led increase in ecommerce has helped BNPL grow in prominence and popularity, particularly in Australia, New Zealand, Europe and later in the US.

Today, there are over 150 BNPL providers across the world. Partnering with merchants to offer a variety of BNPL services as a payment option at checkout, these companies represent a significant presence in the payments space, including in some cases for cross-border payments.

However, as the wider ecommerce space faces a downturn due to factors such as inflation, rising energy costs and supply chain issues, the BNPL industry has faced a more challenging environment. Leading player Klarna has announced it will cut 10% of its staff, while recent low revenue projections from other key players such as Affirm have disappointed investors.

Amidst this increasingly difficult atmosphere, a new challenger has entered the market: computer giant Apple, through an extension of its Apple Pay product. Apple Pay Later is initially launching in the US, although is likely to be expanded globally, and presents a significant threat to many established players.

Given this increasingly tough landscape, what lies ahead for BNPL companies and how do the 150+ global players differentiate as they seek to gain share amid the ecommerce downturn? This report explores the state and structure of the market, and where the key opportunities lie, with insight from key companies across the industry.

Section 1: The state of the BNPL industry

While consumer BNPL dominates the space, there is more complexity to the industry than may initially be expected. This section looks at the overall landscape and types of BNPL currently present in the market.

Consumer BNPL: Customer profile and benefits

Much of BNPL’s success so far has been due to what it offers to consumers, particularly compared to traditional credit products.

It enables those who do not qualify for traditional credit to make small purchases with little or no credit history, while removing the friction associated with traditional credit applications. Instead, it sees the process embedded into the shopping experience, making it a seamless part of the checkout process.

“BNPL is present in that shopping experience moment that they are having when they’re trying to get a specific product, giving them credit access to buy the product in order to complete the shopping journey,” explains Arvin Singh, CEO of Hoolah.

Companies that offer BNPL argue that it is democratising payments, providing increased clarity on potential trade-offs while increasing their control over how they manage and spend their money.

“If you bundle how equitable and how easy it is to access BNPL compared to the traditional alternative where they are paying interest on outstanding balances, then that lays the groundwork for BNPL growth,” says Simone Mancini, CEO of Scalapay.

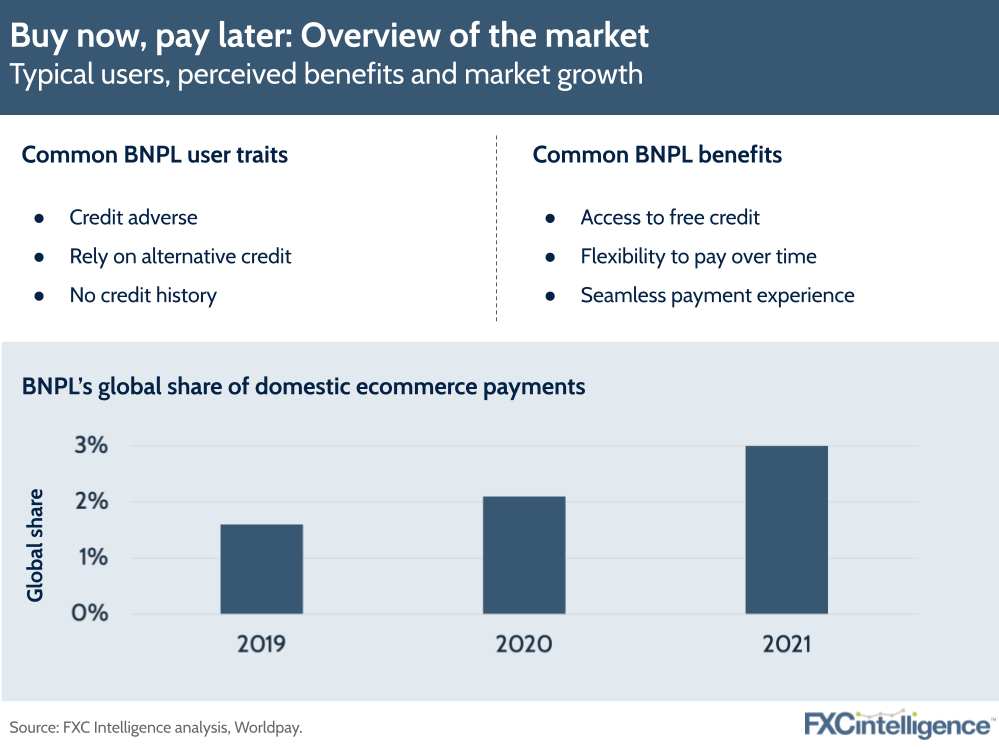

While BNPL remains a minority payment type, it has seen significant growth over the past few years, accounting for 3% of ecommerce payments globally in 2021, up from 2.1% in 2020 and 1.6% in 2019, according to research by Worldpay. Notably, it is also seeing greater popularity among younger consumers, in particular millennials and Generation Z consumers. Jeremy Wong, Head of Strategic Partnerships at Atome, also reports that it is seeing particular adoption among those without credit cards.

For such young consumers, BNPL matches expectations formed by other technologies. Generation Z and millennials grew up using smartphones and so expect a similar level of digitisation, transparency, simplicity and ease from their payment experiences.

“Some of our users may not ever go to a traditional product,” says Singh. “BNPL might be the product that they use now and in the future when it comes to making a digital payment.”

Some are also reportedly becoming increasingly averse to traditional credit solutions.

“Credit card usage has declined significantly in the last five years as the younger consumers prefer debit over credit,” says Zahir Khoja, General Manager North America, Afterpay.

“They want the benefits of credit, but they don’t want the debt that comes with it, only the flexibility to pay over time.”

BNPL is also providing credit opportunities for those who have traditionally been unable to access them, in particular those who are underbanked. For example, gig workers who may have a strong bill payment history may still be unable to access traditional credit or banking services, but can access credit through BNPL.

Figure 1

Buy now, pay later’s benefits for merchants

BNPL offers can vary significantly by provider, which risks confusion for consumers, and makes it necessary for merchants to select the solution that is best suited to their customers.

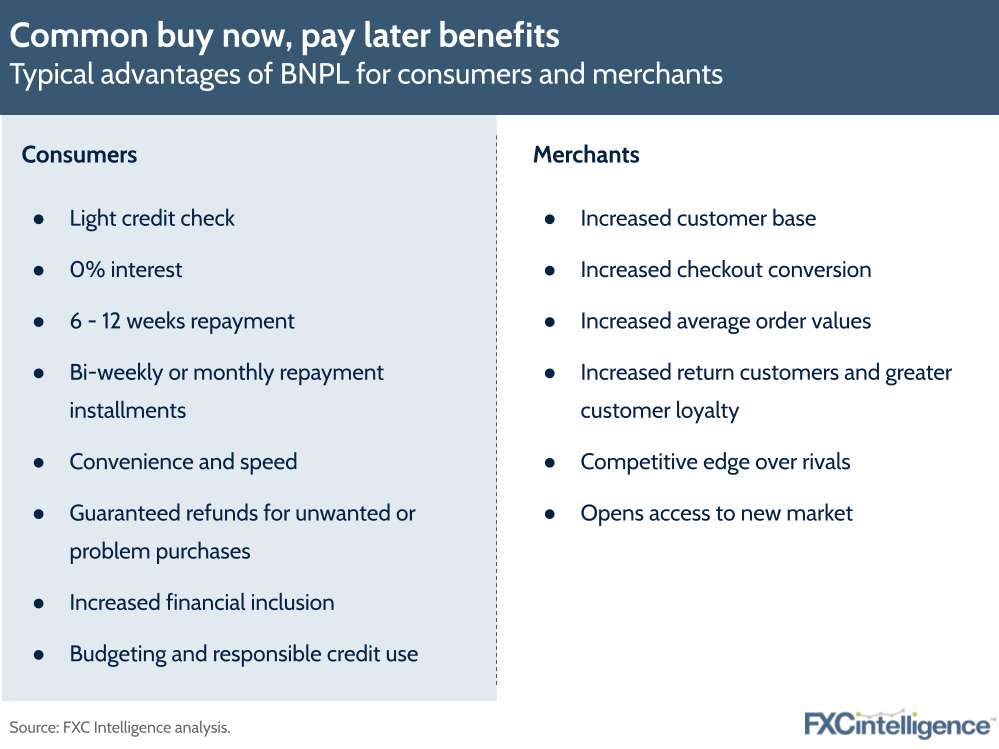

Most buy now, pay later providers carry out only light credit checks, enabling more consumers to access the service compared to many traditional credit solutions. BNPL therefore enables merchants to provide more choice to their customers, and so increase their sale volume.

According to Debbie Guerra, Head of Merchant Payments at ACI Worldwide, BNPL users often make larger purchases than they might have normally done with credit cards. This is due to the favourable interest, which is often at 0%, and the repayment period, which together increase checkout conversion and average order values.

“BNPL acts as a catalyst to increase spend or attract more customers when integrated effectively in the purchasing journey,” adds Scalapay’s Mancini.

Figure 2

Applications for BNPL: From mass consumer to B2B

As buy now, pay later has grown in popularity, it has been applied to a growing range of industries and use cases.

While mass consumer remains the leading application for BNPL, there are a significant number of companies applying the model to both niche consumer use cases and, increasingly, B2B.

Some companies are specifically catering to high one-off costs that are infrequent and which many consumers may not be able to afford up-front. These include to cover travel costs or to pay for a major life event such as a wedding, while some companies have iterated on the traditional layaway or car finance model to cover the purchase of vehicles or home appliances.

On the business side, companies are using BNPL to provide easy finance to companies, particularly SMEs. This helps combat liquidity issues related to customer payments, and in some cases can be used to automate the accounts receivable process.

Figure 3

Repayment of BNPL credit

In most cases, repayments of BNPL credit are taken from the customer’s linked debit card. These typically take the form of fixed, interest-free repayments in between three to six installments. Many providers, including Klarna and Sezzle, also require the first installment to be paid upfront prior to the transaction being processed.

While these practices are commonplace across the industry, the number of payments has provided an opportunity for some providers to differentiate, with some offering the option of considerably more installments. Payment frequency and late fees are also common areas of differentiation between providers.

Figure 4

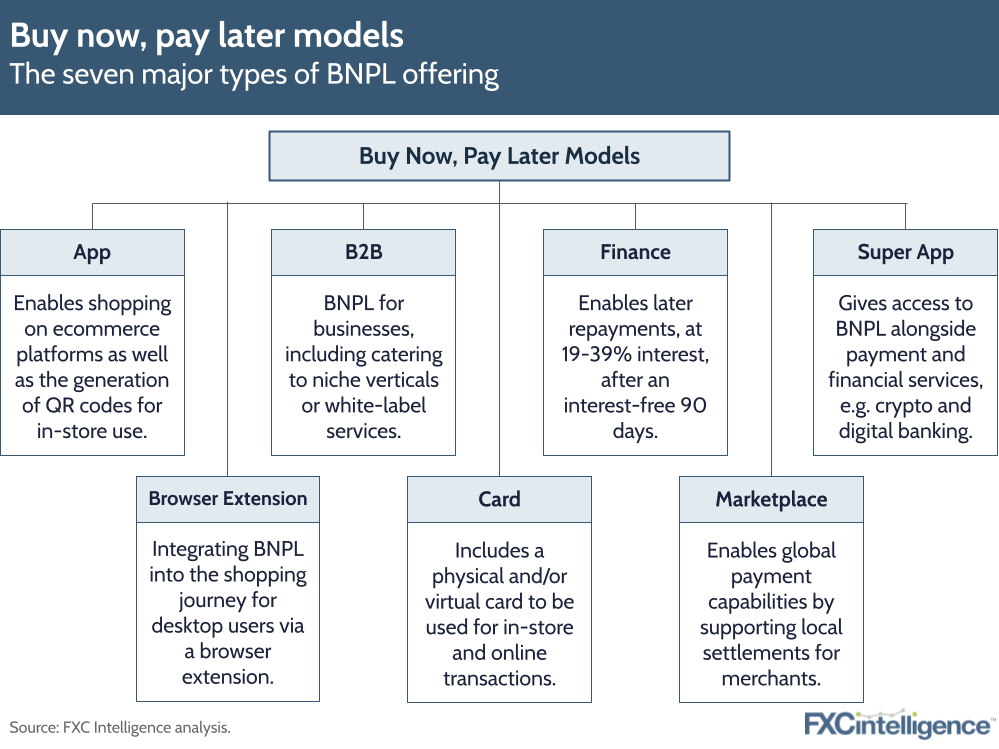

Key buy now, pay later models

While buy now, pay later companies are often characterised as a homogeneous group, there are in reality a wide range of different BNPL models that companies follow.

We have identified seven major models that cover the majority of BNPL offerings that companies provide. These are App; B2B; Browser Extension; Debit Card; Financing; Marketplace and Super App.

Figure 5

While there are some exceptions, most BNPL providers fit under at least one of these models. In some cases, companies offer a combination of two or more BNPL models. Klarna, for example, has a presence across the majority of models.

Figure 6

App Model

Companies with BNPL apps enable consumers to shop on ecommerce platforms from within their own app, providing the ability to pay for the purchase in stages in the process.

This may also enable users to access a particular BNPL service with an ecommerce platform that would not be available by simply browsing their site or app normally. For example, Klarna is not available at Amazon’s checkout, however Klarna’s app enables consumers to use the company’s services to buy from Amazon.

In some cases, BNPL providers also generate a scannable barcode or QR code from their app, which can be used to make in-store purchases. BNPL providers with apps include Affirm, Sezzle, Splitit, Perpay, Paypal, Klarna and others.

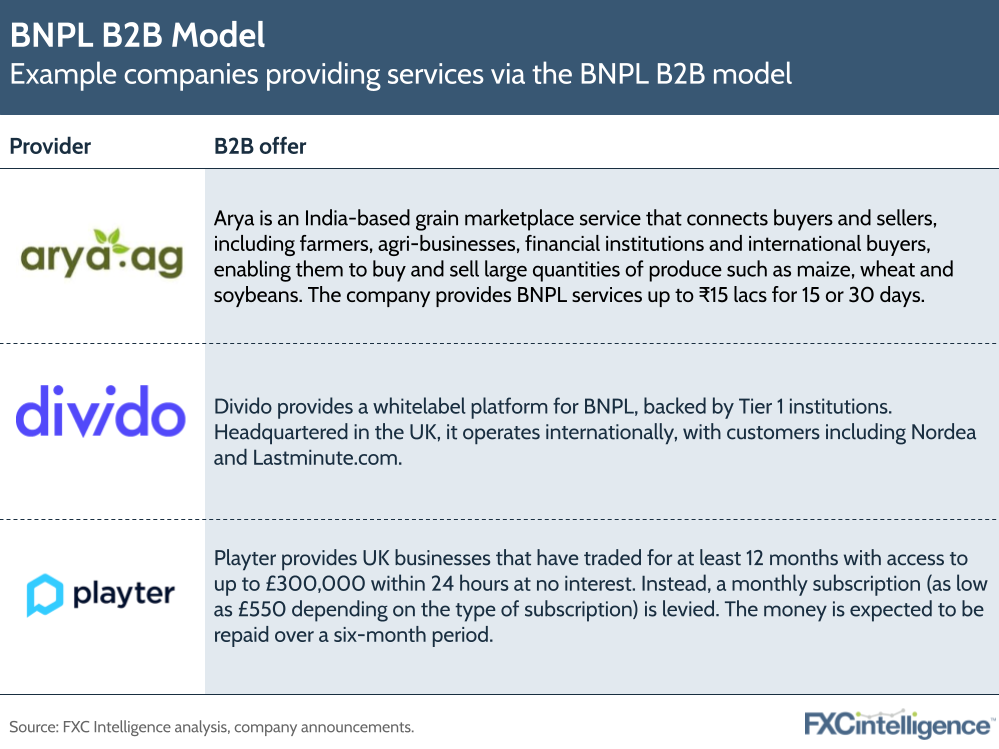

B2B Model

Some fintech companies are finding success in the BNPL space by catering to the needs of companies, rather than consumers. This often takes the form of services for specific industry verticals, often with terms designed to suit the particular needs of a certain type of company. However, there are also a small number of white label providers such as Divido that power branded BNPL services.

“With a whitelabel retail finance platform, you have three players in the mix: the lender, the merchant and the platform,” said Divido CEO Todd Latham. “The lender gets to set credit on their terms, the merchant gets to control and optimise the user experience, and the platform gets to oversee everything in order to tailor their service.”

Figure 7

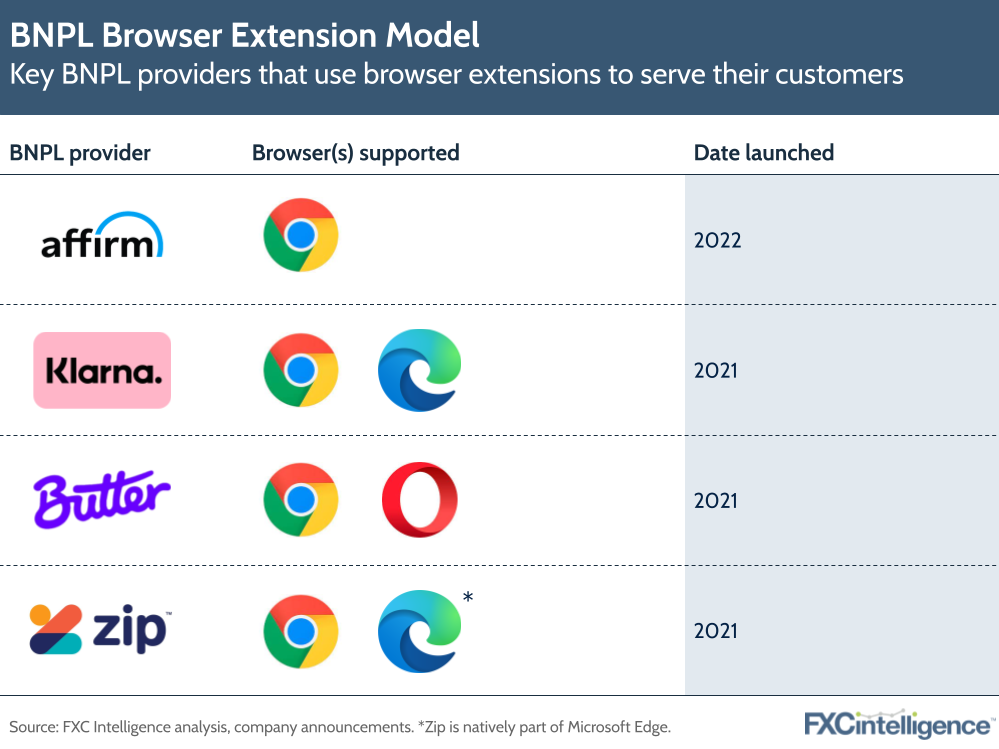

Browser Extension Model

Some BNPL providers are also making the integration of BNPL into shopping journeys hassle-free with optional in-browser BNPL extensions. Primarily designed for desktop users, this typically enables customers to use BNPL to pay for products at any ecommerce site they visit.

In the case of Zip, this does not even require customers to install an extension to use. In November 2021, the company partnered with Microsoft to make the service natively available within its Edge browser. The partnership, which has been met with criticism, enables customers to apply BNPL to any online purchase of between $35-1,000 using the browser.

Figure 8

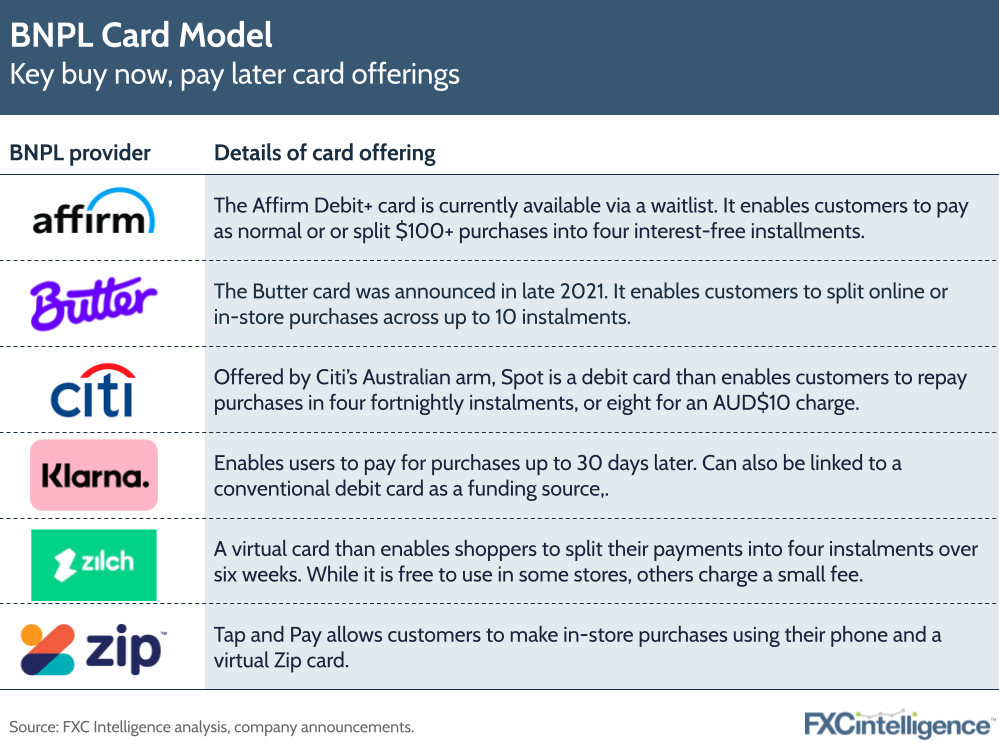

Card Model

BNPL providers that employ a card model offer either physical and virtual cards as part of their service. In some cases, these function like conventional debit cards and also have a BNPL function, while in others they function in a similar manner to a charge card.

In the case of virtual cards, these are issued through the company’s mobile app. They can be used at merchants that accept Visa or Mastercard (depending on the issuer) card payments both in-store and online. These cards come either as single-use for a fixed amount or are reuseable with a set limit, depending on the provider.

Figure 9

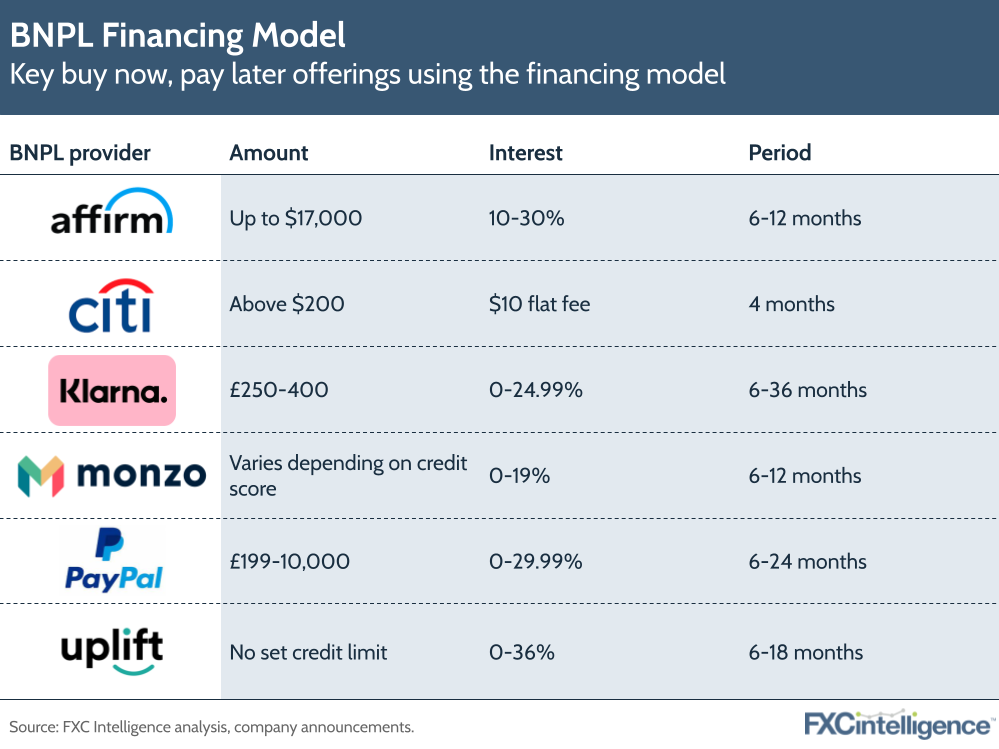

Financing Model

Some BNPL providers use a model that is closer to traditional financing, enabling longer payment periods beyond the typical interest-free period of 90 days. In these cases, users often choose a term length to suit their needs, and typically are borrowing at an interest rate of between 19%-39%. Such loans generally come with a fixed interest rate, monthly rate and due date.

BNPL providers such as PayPal, Klarna, Affirm, Sezzle and Uplift offer finance solutions with interest on purchases such as electronics, furniture, fitness equipment and travel worth $500-$3,000. This is repaid monthly over a period of 6-36 months with interest. For high-cost purchases, this model is perceived to provide cheaper credit and easier payment terms than traditional alternatives, although it comes with a hard credit check, which is often not required for other models.

Figure 10

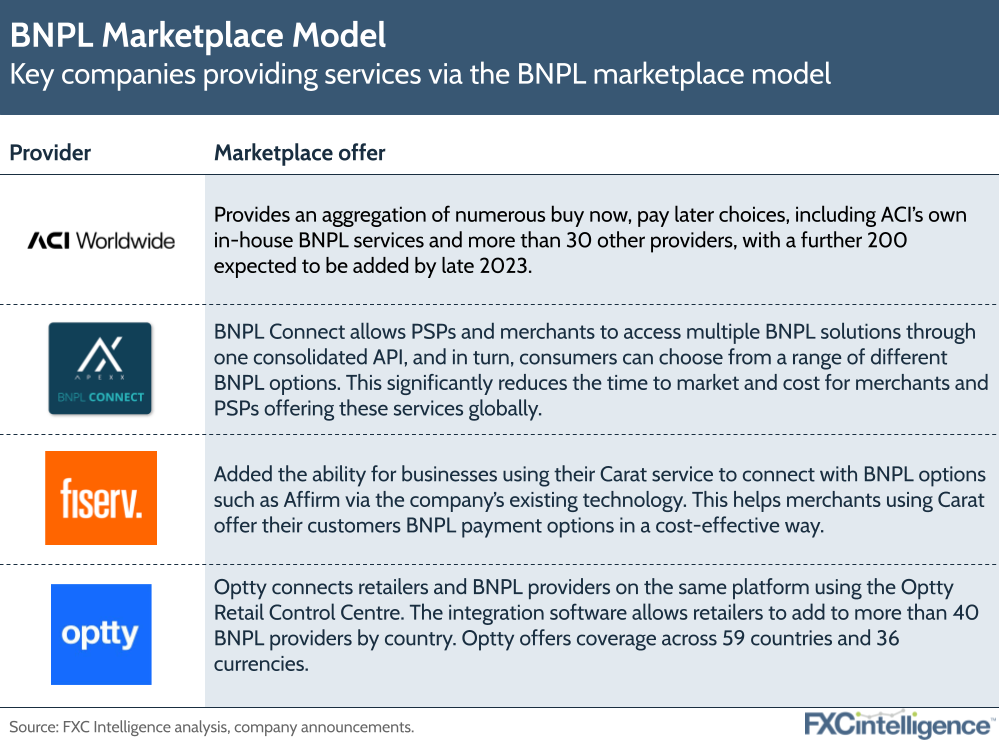

Marketplace Model

This model enables merchants to offer global payment capabilities via local BNPL settlement. This sees the companies that follow it provide access to global BNPL providers, which are displayed at checkout when applicable to the consumer. This enables merchants to offer BNPL services to an international audience in situations where BNPL providers do not serve customers internationally.

In some cases, this model enables merchants to offer multiple BNPL options to individual customers, potentially increasing their chance of being approved for the service.

Figure 11

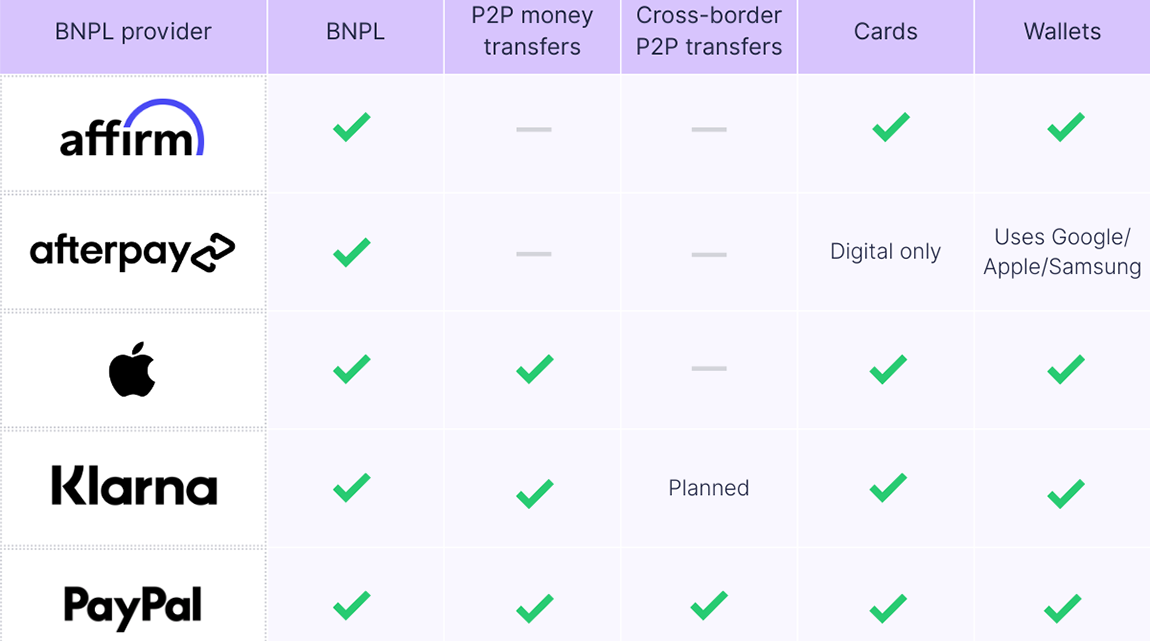

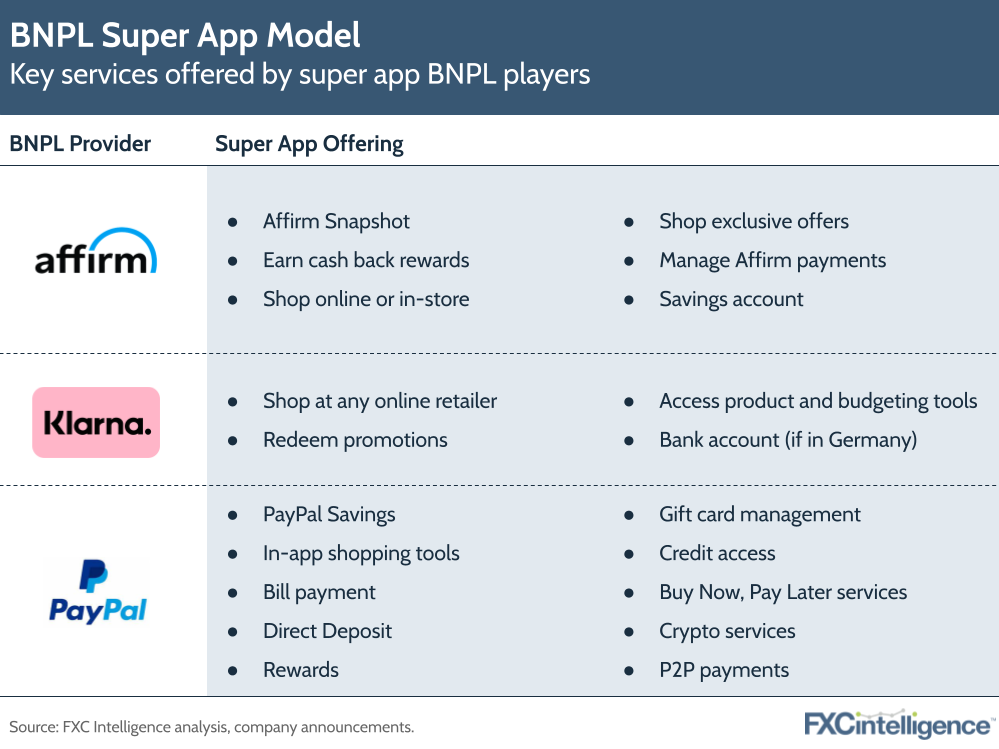

Super App Model

Some BNPL providers are beginning to explore the use of super apps, giving their users access to a wide range of services including BNPL. Other bundled services include payments and financial services. One of the BNPL providers offering this is Affirm. The offers a super app that offers services including budgeting tools; crypto trading; cash-back tracking and outstanding payments monitoring.

Others have also announced moves into this space. For example, in February 2021 Klarna launched bank accounts for users in Germany, and says it plans to expand the service elsewhere. Meanwhile BNPL player FinAccel is planning to launch into digital banking and larger-ticket loans as it secures a 75% stake in Indonesia’s PT Bank Bisnis Internasional.

However, not all BNPL providers are open to having super apps because they see them as contradictory to their proposition, and instead plan to focus on acquiring customers via merchants.

Figure 12

Banks in the BNPL space

The success of buy now, pay later has seen several banks launch their own solutions in the space. These typically make the BNPL process a part of a customer’s banking experience rather than an externally agreed loan, and often enable BNPL to be added after the purchase has been made.

Figure 13

Section 2: Opportunities and challenges in BNPL

The BNPL industry currently faces significant upheaval and uncertainty, however there remain significant opportunities as the market continues to mature and evolve.

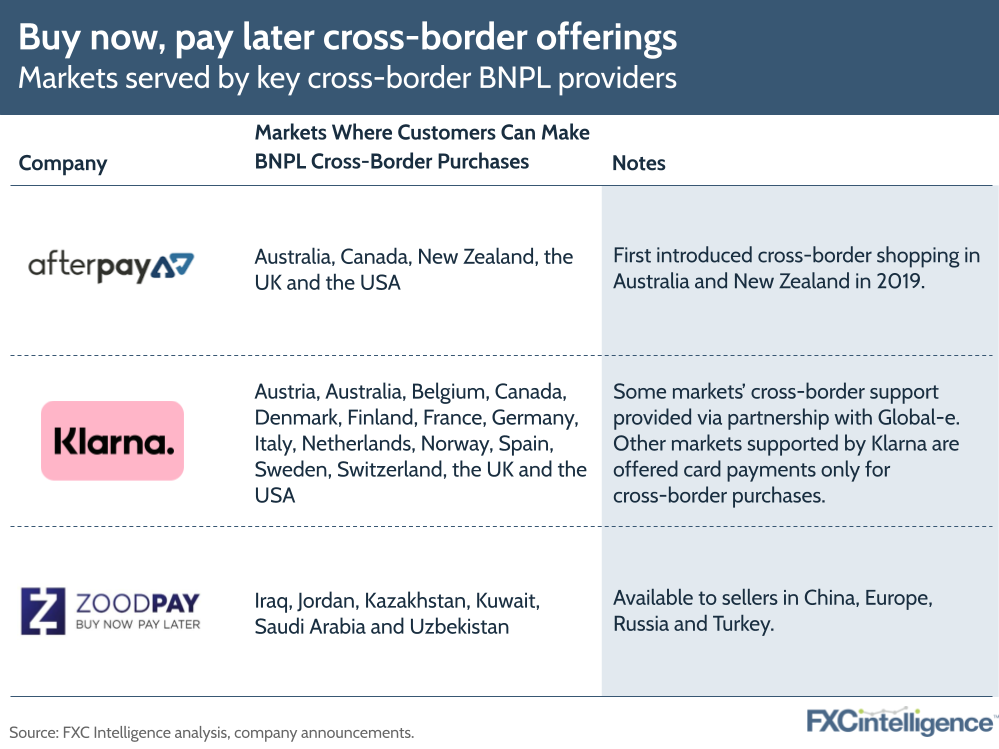

The cross-border payments opportunity

As a growing share of ecommerce, cross-border payments remains a vital opportunity for any industry operating in the space. However, offering BNPL cross-border comes with challenges.

First and foremost, there is the issue of risk. BNPL runs the risk of default, and in some regions of the world debt recovery is harder to enforce than in others. As a result, many companies have so far opted to avoid the complexities of extending cross-border, with those that do have such a service typically restricting it to countries where they have on-the-ground operations. In other cases, they may choose to restrict some aspects of their service in some markets.

For example, a highly fragmented region like Asia involves different regulations, compliance requirements and logistics issues. This is why when Atome onboards a merchant, the risk team establishes restrictive categories or high risk categories that impact how it provides its service.

However, this is by no means the only challenge. Cross-border BNPL comes with cultural differences that impact how merchants sell their products, how products are perceived by customers and how they can be best communicated. Different local payment methods, expected checkout experiences and levels of trust or literacy may also pose a challenge.

For example, Scalapay built BNPL models to localize and increase acceptance of prepaid cards in Italy because prepaid cards account for 30% of ecommerce in the country. However, the company could not use the same model in Germany because such card usage is lower. Instead, the company’s model was adapted to accept bank-to-bank payments.

According to Arvin Singh, CEO of Hoolah, cross-border buy now, pay later is like running a separate business in each country because the marketing is different. He also emphasized that localization is particularly important because the language and currency is likely different.

However, BNPL also provides benefits to the cross-border process. For Uplift, cross-border BNPL is able to bridge those differences for merchants and give them very simple access to commerce in those countries.

“This is where we can add the most value,” said Tom Botts, Chief Commercial Officer of Uplift.

“We have done over 3,000 odd integrations across these countries, so we understand the landscape quite a bit and I think there’s a lot of value in doing that across North America.”

He acknowledged that markets can be different even within countries, taking Quebec in Canada as an example. Not only is the language different, but the regulations differ from every other part of the country.

Cross-border BNPL therefore needs to understand these cultural and regulatory differences, as well as determine an effective risk profile, in order to be successful.

Figure 14

Regulations and financial protections

In almost all countries, consumer credit lending regulations exclude BNPL providers from their scope. In the UK, for example, as fee-free credit agreements that are repayable in less than 12 months, BNPL services fall outside the Financial Conduct Authority’s (FCA) purview. The lack of formal regulation has prompted warnings that this could be the next Wonga-style scandal to hit the financial sector.

BNPL providers have nevertheless complied with relevant laws in their host countries and in some cases have followed best practice approaches in anticipation of future, tighter regulations..

For instance, Uplift, a travel BNPL provider, operates under the US Regulation Z, a federal law that standardises how lenders convey the cost of borrowing to consumers, restricts certain lending practices and protects consumers from being misled. Zilch, meanwhile, recently announced it was partnering with Experian to start the reciprocal reporting of credit data for affordability checks in BNPL loans.

Jeremy Wong, Head of Strategic Partnership at Atome, said that the company relies “on local legal teams and legal councils to actually advise [them] on how to be compliant”. He believes that there will be appropriate guidelines introduced that will encourage innovation, but not at the expense of consumer debt.

However, there has been a continued push for BNPL regulations across countries, especially to combat abusive practices related to repayments and to build trust in the ecosystem.

Hoolah’s Singh, is of the opinion that the BNPL ecosystem should include the voice and perspective of regulators because they have a strong interest in protecting customers, which he sees as a natural evolution of the industry.

Uplift’s Botts, meanwhile, believes that the increase in the size of BNPL loans will increase regulatory interest in BNPL, both from a consumer protection standpoint and in order to bring it in line with areas such as credit cards and mortgages.

Some of the regulatory challenges include:

- Customers spending more than is intended or more than they can afford to repay.

- The lack of clarity involved when presenting terms and conditions.

- Credit rating being affected by late repayment.

Several independent bodies have advocated for better transparency, lower costs, financial product information and better budgeting tools than alternate credit decisions made by consumers. BNPL providers insist that for every BNPL application submitted, there is information available on what BNPL purchase the consumers are about to make, what that option is, what the modality looks like and visibility on how their information is going to be used.

Hoolah also agrees that when it comes to using the BNPL service, there’s a high level of transparency needed to ensure that customers’ financial wellness is guaranteed. Meanwhile, Afterpay highlighted the company’s tools to block customers from getting additional BNPL services if they are at risk of accruing unsustainable debt.

On a B2B scale, Atome provides capabilities for banks and financial institutions to score their customers, or perform risk assessments/ EKYC through its B2B risk underwriting engine.

Some companies, including Uplift, also have tools to check a customer’s credit rating as part of the application process, as well as provide the ability for customers to request interest-free pauses to repayments.

“We don’t give them more than they can afford because that’s not fair to customers,” said Botts.

“It is a very thoughtful process in terms of ensuring that we are not placing undue burden on consumers in order for them to realize their dreams and take the trips of their lives.”

Conscious of inevitable regulatory change, many BNPL providers are willing to comply with any BNPL regulations that are to come.

“We welcome the opportunity to work hand in glove with regulators, to make sure that we are meeting high standards and delivering a positive consumer outcome while ensuring we protect their data,” said Zahir Khoja, General Manager North America, Afterpay.

BNPL financing and profitability

Many buy now, pay later companies are venture capital (VC) funded, and so are often highly growth orientated, with a focus on disrupting traditional industries and rapidly driving up their valuations.

In most cases, finance for loans is provided by banks or other financial services companies, who typically take a cut of each payment.

However, profitability can be elusive. The BNPL industry is a highly competitive market with a high turnover but low margin. Most BNPL providers make money from the 2-8% transaction fee charged to merchants on every purchase. This makes partnerships with large retailers a priority. Late payment fees are another source of revenue, although not all providers have these.

This makes finding profit a largely unrealised goal, but one that is providing increasingly challenging as the space struggles with a drop in consumer spending.

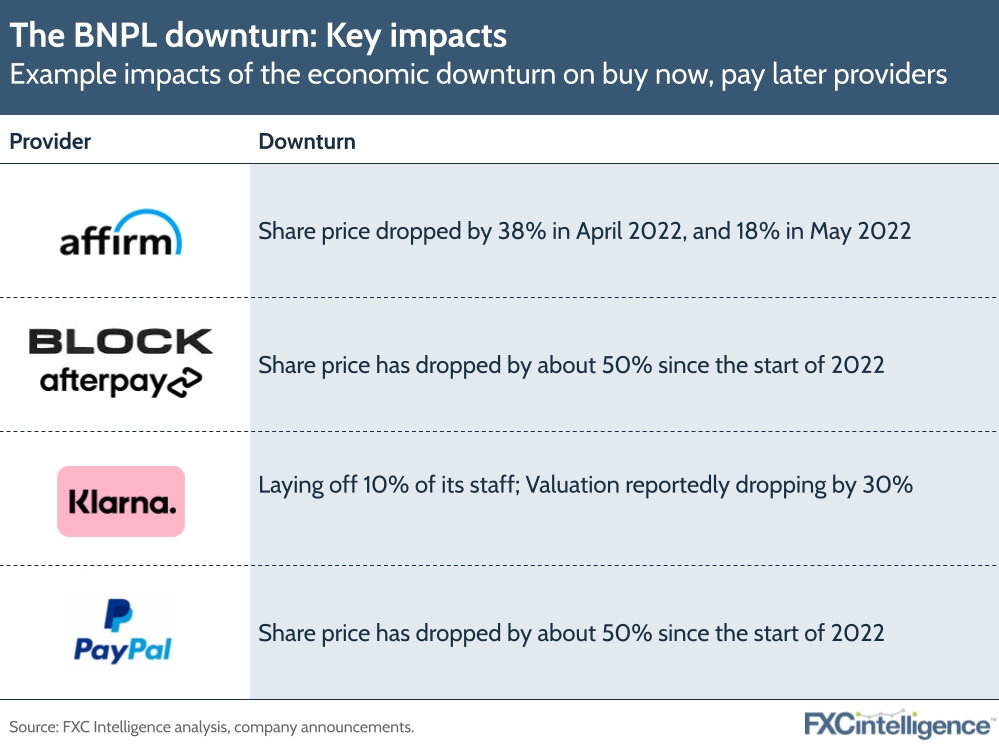

The buy now, pay later downturn

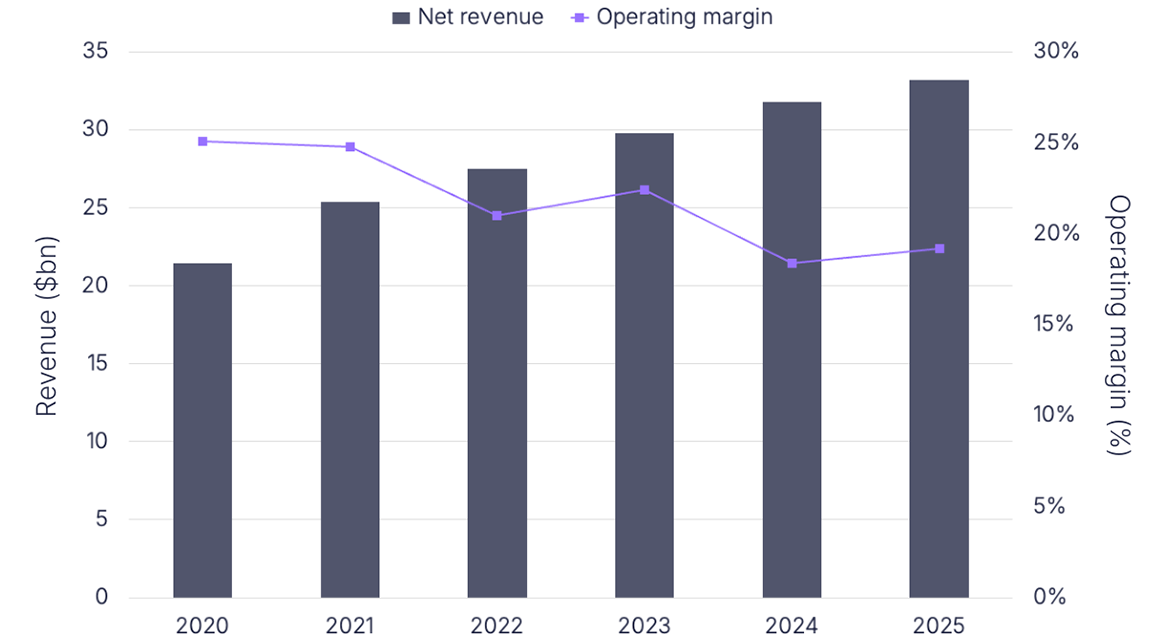

Inflation, rising operational costs, changes in consumer sentiment and the war in Ukraine have all introduced some uncertainty to the BNPL industry. Several BNPL providers such as Affirm, Paypal and Afterpay owner Block have witnessed plunging stock value. Credit losses keep accruing, which is reflected in Klarna’s net loss rising in Q1 2022.

Rising operating costs have posed a particular issue for the industry, which is running on a low margin. Due to competition, merchants cannot be charged higher fees nor can consumers be charged more or even at all.

Some of the BNPL providers currently have a freeze on hiring. In early June, there was a staff layoff announcement by Klarna using a pre-recorded video message. The Swedish company is laying off around 700 staff after speculation that it is seeking a new round of investment (up to $1bn) that could see its valuation drop by 30% to $30bn.

Despite the exponential growth of the BNPL industry and the market becoming saturated with new entrants, these recent developments coupled with the broader macroeconomic issues and regulatory additions have a negative impact on the industry as well as on investors’ confidence.

Figure 15

Section 3: The introduction of Apple Pay Later

Apple’s announcement that it is launching a BNPL service as part of Apple Pay has potentially profound impacts for the industry.

An introduction to Apple Pay Later

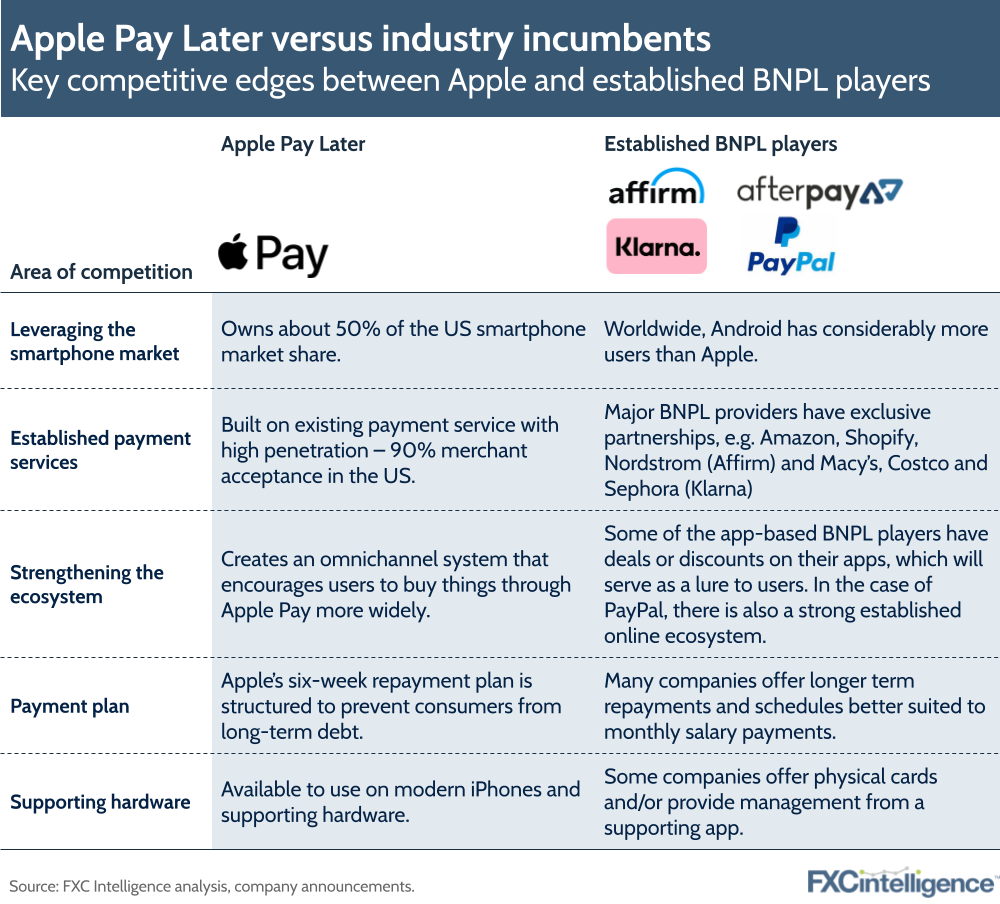

Technology giant Apple announced in June that it was launching Apple Pay Later as an addition to its payment products later this year. The announcement, which was made at the company’s annual Worldwide Developers Conference in Cupertino, California, included that the Apple BNPL product would be rolled out as part of the upcoming iOS 16 for iPhone.

Apple Pay Later will allow customers split the cost of a purchase made through Apple Pay into four equal payments over a period of six weeks, with zero interest and fees. It will be available everywhere Apple Pay is accepted online or in-person, using the Mastercard network.

While there is initial financing from Goldman Sachs, the company is ultimately looking to bring this in-house.

Apple is expected to enable consumers to borrow up to $1,000 per purchase, although the exact amount will be determined by a combination of their credit rating and other factors, including their Apple ID.

The impact on the wider BNPL industry

As Apple Pay is accepted by over 90% of US retailers, Apple Pay Later has an instant network unparalleled by most other major BNPL players in the US market. Apple will therefore be in direct competition with other BNPL companies, including Klarna, PayPal, Affirm and others.

This makes the offering a potentially lucrative revenue stream for Apple, which is expected to make money from each Apple Pay Later transaction via merchant fees. The company’s wider Apple Pay service may also see a boost, bringing additional benefits to the wider ecosystem.

For the wider industry, it has caused concerns around the ability for smaller brands to compete, however others have welcomed the development as a sign of market maturation.

“Apple’s foray into Buy Now, Pay Later is evidence that the market is maturing,” said Todd Latham, CEO of Divido.

“A highly respected brand entering the marketplace shows that BNPL is not only here to stay, but will continue to innovate. This, coupled with incoming regulation, demonstrates that the checkout finance sector is gearing up for long-term success.”

Figure 16

However, while the company poses a significant threat in the US market, where it has the potential to ultimately claim the title of market leader, its international prospects are not as strong.

While in the US, iOS is the leading smartphone operating system, with around 50% market share, the company does not have as high market penetration internationally, accounting for less than a third of phones worldwide. This includes some regions with a strong BNPL presence such as Europe, although the UK and Oceana do both have a slightly higher number of iOS users than Android.

As Apple handsets define the total addressable market for Apple Pay, and therefore Apple Pay Later, any expansion beyond the US is therefore likely to prioritise markets where both BNPL adoption and iPhone usage is high, such as the UK and Australia.

Even in the US, Apple is not going to be able to convert all its Pay customers to Pay Later. Some Apple users, for example, are likely to prefer to continue to make purchases with their credit cards to gain points and rewards instead of the BNPL service.

However, for established BNPL players in the market the company does pose a threat, with one of the biggest protections likely to be from partnerships. A number of the key BNPL players have exclusive partnerships with large retailers, which gives them access to more shoppers and lends them brand loyalty.

Elsewhere, additional services through super apps or online solutions such as browser extensions are likely to help provide additional protection, although it is ultimately going to be up to individual brands to successfully communicate to potential customers about why their service is superior.

Apple Pay Later is undoubtedly going to take market share from other major players. How much, and who from, is ultimately going to be determined by strong products and stronger communication.