Intermex saw strong revenues in Q3, despite a slowdown in revenue growth compared to last year. In the latest in our Post-Earnings Call series, we discussed the recent results, key growth drivers and Intermex’s ongoing La Nacional acquisition with CEO Bob Lisy.

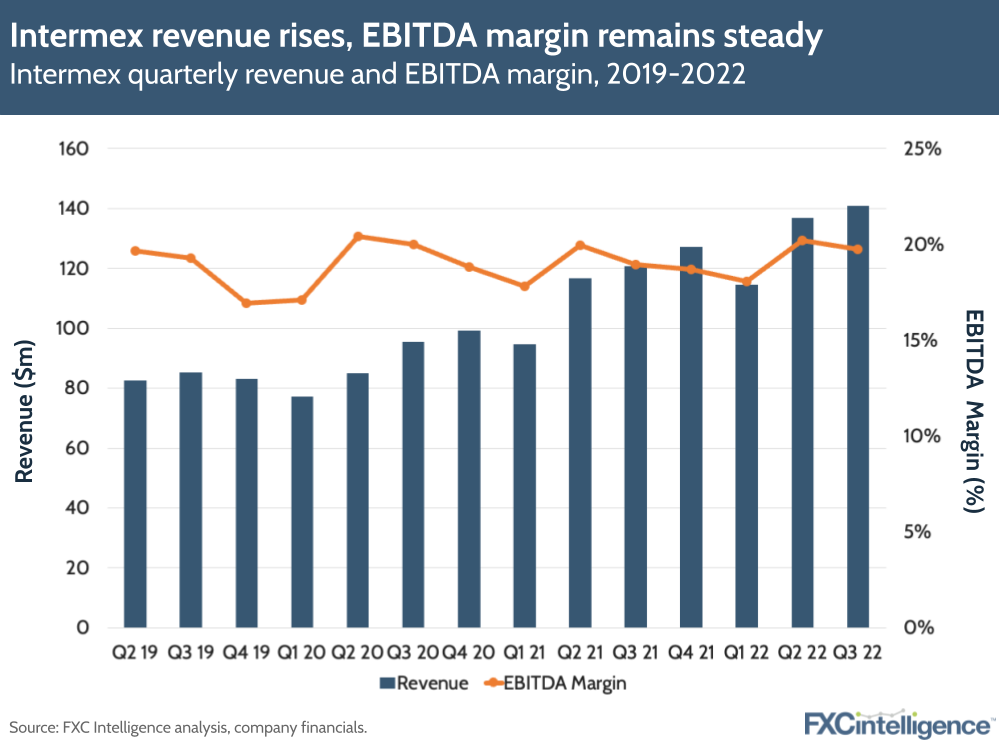

LatAm-focused remittances player Intermex has had another solid quarter in Q3 2022. Revenues increased 16.6% YoY to $140.8m (compared to 26% growth in Q3 2021), while adjusted EBITDA was $27.8m, up 21.5%. This gave the company an adjusted EBITDA margin of 19.7%, up from 18.97% in Q3 2021.

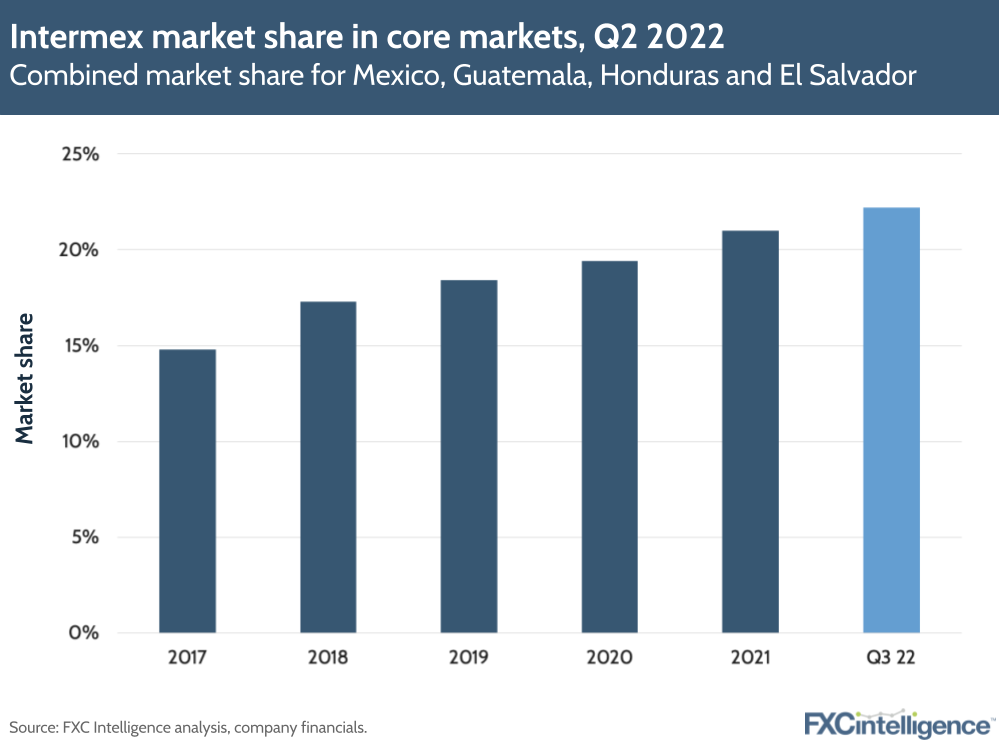

Intermex continues to grow its presence in core markets. Principal sent increased 17% to $5.5bn, translating to a 22.2% market share across the Guatemala, Mexico, El Salvador and Honduras markets (up slightly from 21.8% in Q3 21). The number of money transfer transactions increased again by 16% to 12.2 million, a new record for remittances.

Intermex has now completed its acquisition of money transfer competitor La Nacional’s US assets, with European assets still pending. After this is completed, Intermex expects to have more than 20% combined market share in seven markets that comprise 87% of all US remittances to LatAm and the Caribbean.

Intermex is still maintaining its omnichannel strategy, having grown the number of transactions deposited directly into bank accounts by 28%. The company also talked about its IMX direct software, which aims to simplify the wire transaction process for retail agents when they move onto the system by Q2 2023.

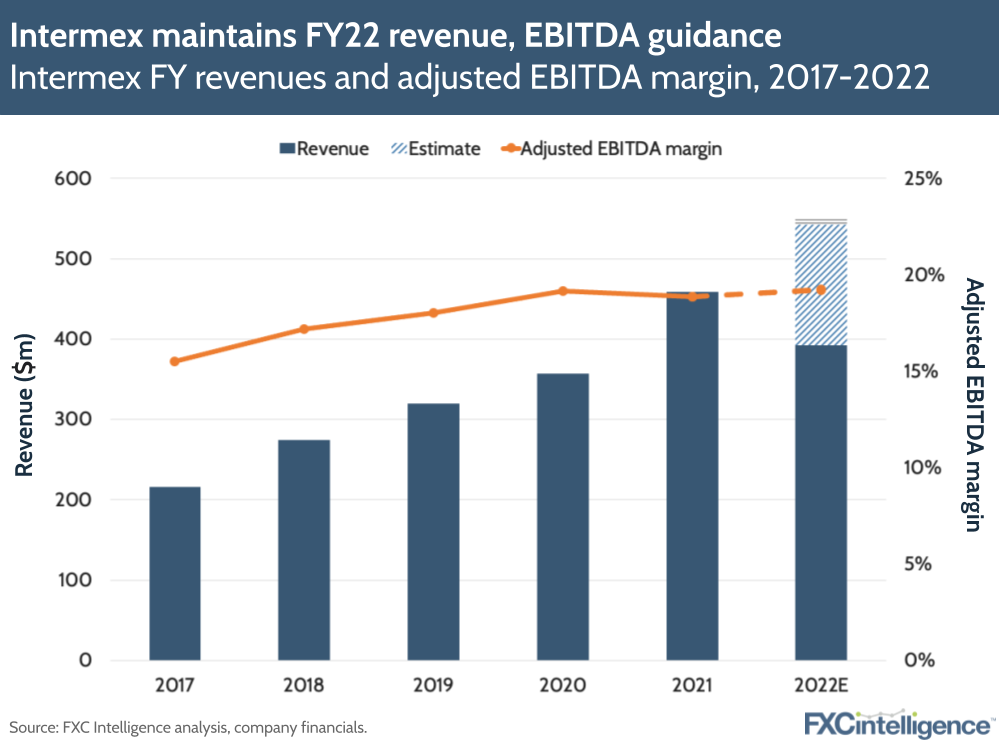

The company continues to project revenues of $542m-$551m for the full year, an increase of 18-20%, and an adjusted EBITDA of $104m-$106m. I spoke to Intermex CEO Bob Lisy to find out more about what’s driven growth in the quarter, Intermex’s digital strategy, its European expansion play and more.

Intermex growth drivers in Q3 2022

Daniel Webber:

Talk us through the drivers over the last quarter that have been supporting the growth and profitability in the business?

Bob Lisy:

We continue to grow. Our business has been strong throughout the country, but it’s slowed down a bit. Where we’ve typically seen revenue around 20% or more growth, we dropped to 16.6%.

We continue to add wires at a high pace, but we’ve got a bigger base number. The law of big numbers is coming into effect. There’s been a slowdown in Mexico and Guatemala, and we’ve been able to persevere through that and still grow close to 17%.

Had we executed everything perfectly, we could have probably still achieved 19-20% growth. There’s a lot of opportunity out there, and we execute better than anyone that’s ever been out there in the field. You can see this from our cohort group: Western Union with a huge negative EBITDA, MoneyGram with a slightly negative EBITDA and Ria barely growing their EBITDA. There’s still an opportunity for us to ratchet up further, and that’s what we’ll be focused on doing in the fourth quarter and going into next year.

However, it’s gotten a little tougher out there. When it slows down, everybody scrapes for wires more, so the small guys get more ravenous and they’ll discount even more. We’re just battling our way through that. The thing that we’re always proud about is that we didn’t sacrifice top-line growth. It was almost 17%, so it was still pretty solid, but for at least 17 out of 17 quarters we found a way to at least meet, if not exceed our EBITDA targets. We did it again, even through a challenging quarter.

We feel like we’re pretty good at persevering, even if it slows down a bit, and still finding ways to be able to hit the EBITDA and the profit numbers regardless.

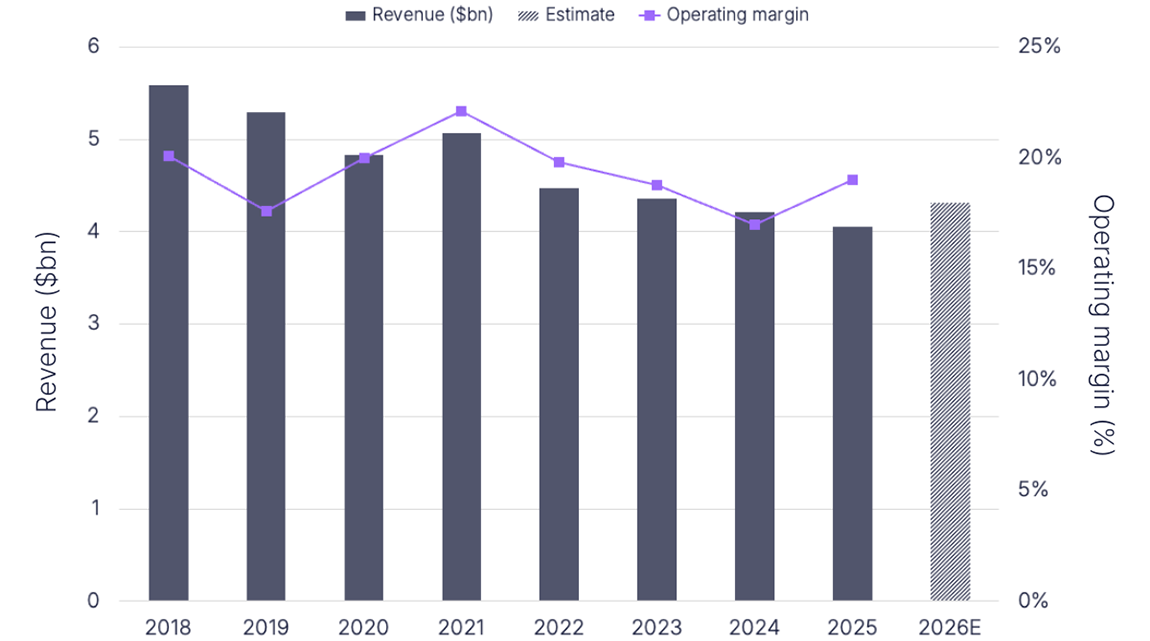

Figure 1

Impact of economic downturn in core markets

Daniel Webber:

What do you feel about the current economic headwinds going forward?

Bob Lisy:

We define a recession, for instance, as the economy shrinking. In Mexico, we stopped growing in the high teens, and we’re growing in the low teens – it’s still a great market. You can’t grow in the high teens forever. It’s been incredible growth that really started about the time of the Trump administration, ran all the way through Trump and through the first year or so of Biden.

It was probably coming to an end, and then we had the government incentives that were put out there that buoyed the economy a little more, putting money either in the hands of the direct sender or in the hands of the people that might hire them.

Those are factors that slowed it down but, to be clear, it’s not contracting, it’s just slowed from the tremendous growth that it had for several years.

Figure 2

Intermex’s approach to adding new agents

Daniel Webber:

What’s your approach to adding new agents?

Bob Lisy:

The number of agents we added isn’t really a great indicator of anything. Really, the more important piece is the quality of the agents that we’re adding.

When I first took over, this company had over 5,000 retailers. I’ve cut it down to 2,000, and we grew throughout all of that. Western Union doesn’t do any more business to Latin America than we do, and they’ve got 75,000 retailers capturing 10 times as many wires in the US as we have.

It’s about productive retailers in the right neighborhoods. Our average retailer probably does four to five times what the average retailer in the industry does, because we precisely place them in the right neighborhood. We do an onsite business review to understand how many wires we’re going to be able to get from that retailer. We just wouldn’t add them if we couldn’t get 150-200 wires per month within the first few months.

In terms of the customers, that is an ultimate offshoot of putting up new retailers. Sometimes, when you put up new retailers in areas where you haven’t been, you’re going to see new customers because they haven’t been exposed to your brand. That growth in new customers is pretty solid. That, along with the same-store growth that we have, drives overall business growth.

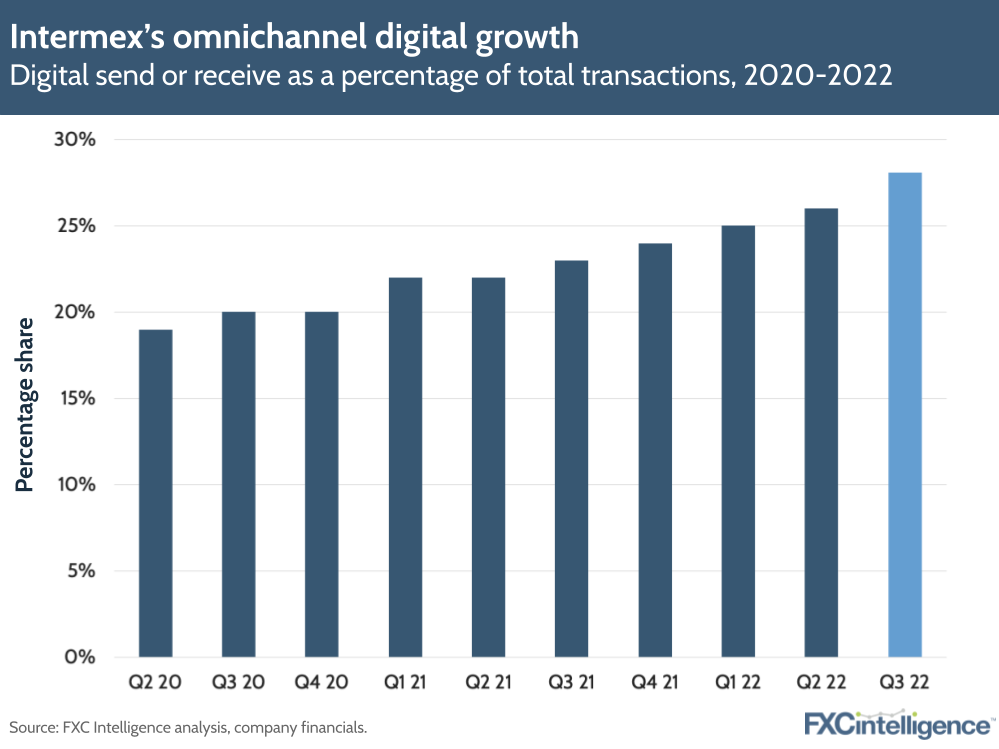

Figure 3

Digital versus retail customer acquisition

Daniel Webber:

How are you navigating the increase to digital, while still making agents happy?

Bob Lisy:

The two do not meet. We’re not advertising to our retailer consumers that they ought to go to digital. We get our digital customers either unsolicited or they pick up our advertising on the internet, and we direct them to our site. It’s really not a problem for us at all with our agents today.

Obviously, agents benefit if we have a stronger product, which means more wires being paid to digital bank accounts, because it might drive more wires through their locations. However, I don’t think there is a big difficulty, because we’ve never said we’re trying to move people to digital. We’re trying to give the consumer every possible choice to send, and every possible choice to receive, so we’re agnostic.

Agents probably have a bigger issue with some of the other companies out there that have said, “We’re trying to move our business to digital. We think digital is the future”. We’ve never really been those guys. We’re growing digital by the sake of its value for consumers.

Most consumers that are retail are only retail. Most consumers that are digital are only digital. There’s an overlap, but a very small one. It’s not like you’re going to be converting people that don’t have bank accounts to digital. They’re going to be at retail. So, unless you’re right in the agent’s face doing that (which we don’t) there doesn’t seem to be any issue right now.

Figure 4

Digital receive growth

Daniel Webber:

What’s driving digital growth on the receive side?

Bob Lisy:

It’s the companies that want more connectivity, more integration and more entanglement with the consumer receiving. When that person comes in to receive money, they’re going to try to incentivise them in any way they can to open an account, so that they have those funds and they’ve got the ability to charge service charges on it.

Most of it’s driven by [banks like] BanCoppel, Banco Azteca and Banorte. They want to get that customer out of their lobby, for one, because that’s expensive and they’d rather they use the ATM. Secondly they create entanglement where they’ve got funds with that consumer and ATM fees, debit card fees and everything else that all banks want to have.

That’s the start of it. There might be some consumers that say it would be easier for them to receive the money to their bank account. However, a lot of it is the outreach by the banks that are trying to drive people there, because it’s better for the banks.

Daniel Webber:

Have you seen any increase in uptake or demand on the e-wallet side?

Bob Lisy:

Not a lot in absolute numbers. The percentages might be good for the e-wallet that we offer in Mexico and a couple other places, but it’s a really tiny piece of our business still.

Update on the La Nacional acquisition

Daniel Webber:

Any additional colour you can provide on the La Nacional acquisition?

Bob Lisy:

Ultimately, the back room will be shared with Intermex and it will be a marketed brand that will have its sales force in the US. It will probably drive about 600,000/700,000 wires a month, which is about 12%,13% of how big we are today. It’s going to be very profitable and very concentrated, mostly in the Eastern Seaboard.

When we integrate that, it’ll lower a lot of costs. There’s an opportunity for a margin of up to 10%/11%. It’s a much lower gross margin, so the EBITDA margin is going to be lower, but it can be a business that’s probably somewhere between $7m-$10m in EBITDA (where it sits today).

The strategic value is in opening up a whole new continent and doing business in Spain, Italy and Germany. It’s profitable today, and they go to a lot of other countries out there because that’s a broader spectrum of corridors (it’s not as concentrated as the US) and the acquisition will open up all those corridors out of the US as well. We’ll have wires out of Europe outbound to those places, and we’ll be able to upgrade with the quality of service we provide and our know-how to build out that European niche.

Europe is much more likely for the consumers to be banked, and since they don’t have a quality online product, that’s going to put us in a position to build our online business out of Europe through those bank consumers. We just closed on the US, but we’ve still yet to close on Europe, with final approval expected in late Q4 or early in the new year.

The role of big box retailers in remittances

Daniel Webber:

How’s the competitive environment with Walmart and other big box retailers? Have you seen any change?

Bob Lisy:

Walmart is not a player in this industry. Anybody who has a lot of locations and sells wires can do a number of wires. For example, Walgreens probably do about 10 per location, but they have 7,000 locations, so it’s really easy to do 70,000 wires. Our top location does 12,000 wires a month. You could put our top five locations together and it does more than 7,000 Walgreens.

Walmart is never going to be the leader, because nobody has a good reason to get on a bus, subway or bicycle and go past 60 money transfer locations on the way. When somebody goes to Walmart to buy clothes, they might also send a wire. It’s great for Walmart to have that as an addition, but not so great for the money transfer company.

Secondly, Walmart does it under their terms, so the margins are really low. The quality of service for your customers will be low, because the person’s got to get in line to do a money transfer. Given all those things, we don’t find it to be productive. We want our customers in a setting where the quality of service is better.

In 2005, when we sold Vigo, Western Union had a 40% market share. Western Union is very much driven by being in the big box stores. Today, with that same group of products, Western Union probably has a 22% share. They lost 17 percentage points. They mostly lost that because the business moved from big boxes to retail, and they weren’t able to catch enough of it with Vigo, because Vigo was an inferior product after what they did to it.

Walgreens, Walmart – all these companies are set up to service the general population, and there’s 33,000/34,000 zip codes in the US. Only about 3,500 of those are important for the Latin American community. You get a lot of unproductive places that are really not going to drive wires, and they’re just useless. By sheer numbers, they get some that do drive wires, but even their best won’t do what an individual one will in the right zip code. It’s more about rifle shot, and it’s not about a Gatling gun when it comes to remittances internationally.

Daniel Webber:

What allowed the smaller players to suddenly start taking share from the big box retailers?

Bob Lisy:

It was retailers going and putting up Western Union when they didn’t know how to do it. Then Ria, Orlandi Valuta and Vigo came around and empowered those smaller retailers.

Western Union started with domestic and ubiquity, because to go domestic, you need ubiquity. They went into all the big boxes, because it would cover zip codes throughout the country. However, the Latin business is point to point, so when you do that, it’s a different model, and they never really responded to that by going into the zip code, zip code by zip code.

Crypto in remittances

Daniel Webber:

MoneyGram just launched a crypto product for its customers, and Western Union is reported to be filing trademarks for a crypto product. What are your thoughts on crypto for this customer base?

Bob Lisy:

Some people, if they can’t compete in some things, pick another avenue that may not even be worth competing in. Instead of putting their resources in retail, they’re always looking for some big announcement. I never believed in crypto, and certainly never believed in it for our customers.

There’s something I always envision when thinking about crypto. As 200 workers are filing out of the farm, instead of giving each of them $150 for their day’s work, am I somehow going to give them a bitcoin? Then they’re going to take that bitcoin, convert it at retail and send it, but you can’t spend bitcoin at the little tienda in the little village in Mexico. I send it to my wife, but then maybe bitcoin goes down 20% while she’s holding it before she can turn it into pesos. It just doesn’t make any sense.

Not only aren’t people asking for it, it actually brings negative value to the consumer. That’s what I don’t understand.

Daniel Webber:

Bob, thank you.

Bob Lisy:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.