FXC Intelligence’s Daniel Webber spoke to Intermex CEO Robert Lisy about the company’s Q1 2021 earnings results and future plans.

With a focus on essential workers and its retail agent network, Intermex did not see any meaningful dip in 2020 and the numbers through mid-May this year suggest growth for both top and bottom lines will continue on the upward paths set by previous years.

Unlike its competitors, Intermex is highly agent-focused, claiming a far higher number of transactions per agent, and is less focused on the opportunities in digital than other leading remittance players.

With this in mind, how does Intermex plan to continue its run of success?

FXC Intelligence CEO Daniel Webber had a detailed discussion with Intermex CEO Robert Lisy to find out more.

Topics covered:

- Drivers of revenue and transaction growth

- Leveraging the agent network

- Approach to marketing

- Unit economics and customer acquisition

- Digital business growth

- Beyond the pandemic

- Leveraging the Intermex platform

- Geographic expansion

Drivers of Revenue and Transaction Growth

Daniel Webber: Let’s start with your strong revenue, transactions and profitability. What’s continuing to drive that?

Robert Lisy:

Let me start from why our transaction growth is so profitable. I think it’s because it’s traditional; we don’t have a lot to do to go get it. And we’ve got a ton of ‘beautiful fish’ right in our front yard – in our retail business. Whereas Western Union and MoneyGram, the growth that they’re seeing, which is minimal – three, four percent of transactions – it’s coming all from the online business, which is really, really expensive to go and get those consumers.

Today we think that it still costs somewhere around $100, maybe as low as $60 dollars, to get a consumer on your site to do a transaction. And those consumers don’t necessarily stay long enough even for you to get a payback, even over time, just on the gross margin line. So one of the reasons profitability continues to be great is that we’re leveraging our business, and we’ve got a lot more growth to attain in a couple places where people thought, “Well, gee, they’ve grown so much; is there more to grow?”

Mexico and Guatemala have been tremendous growth vehicles for us and those margins continue to hold up really well. And they tend to be more profitable than other countries because they have a strong FX component. And that continues within that whole context; Mexico, Guatemala, El Salvador and Honduras. Those four countries together are 75% of all money sent from the US to Latin America and we’ve now achieved over 20% share to those countries.

Some of the numbers hit me really hard, in a good way. If I look at some of the days we had over Mother’s Day, and we’re doing more wires out of Hondouras than we used to do as a company just eight or nine years ago, and that’s crazy. We do more transactions to Mexico than we did as a company.

Then we start doing more transactions to Guatemala than we did as a company. When we start getting to our tertiary countries, we feel quite good about that growth. Behind those countries, then we have countries like Dominican Republic, Ecuador, Nicaragua, Colombia, Peru that have grown really, really well for us in the high 30s to low 40s. We think there’s a lot of business to be done there; it’s much more concentrated so it’s easier to go after. Part of the reason that was down the road for us is that we wanted to be at a certain place with Mexico, Guatemala, which are really the foundation of our business – that’s where you really can build a business on – and now, because the incremental cost of doing a wire to El Salvador, Dominican Republic, Honduras, whatever, is very low, we still make money on those on the edge.

Transactions continue to grow because we’ve got a much better plan than anyone. We’ve got the things we’ve always talked about. Our speed; the fact that we have better banking relationships and better banking solutions for agents; the fact that we know how to pick the right agents and that our average agent averages over 400 wires per month, which is probably 3 to 4 times what the industry averages. All of those things, we’ve taken that path of productivity in our agent network, versus ubiquity. So we have less agents than people that are much smaller than us, but because our productivity is so high, it drives a lot of wires.

That continues to happen, and we think the western states are really a big part of our next chapter. They’ve been a big part of our chapter, they did a lot of the growth, but we still have a penetration level in the west of the US, Mississippi, that’s a fourth or fifth as much as we have in the eastern states. And that’s just simply a matter of people hours and months, and putting enough people on the streets overtime to put agent retailers in the right locations to drive that business.

We have a license already to be a money transmitter in Mexico and Guatemala; two of the biggest countries, so you’ll see us start to build that. So we have a lot of plans. We continue to have a lot of free cash and we’re working on some things right now related to financing that will create a lot more free cash that will put us in a position, when we find a worthwhile acquisition, which we’re working on a few today, that we’ll have the cash there to be able to do those things in cash and not worry about having to finance them or get stock or anything else.

So we like the position we’re in and I think May so far has been great with Mother’s Day. We couldn’t have asked for better or stronger, and we continue to move forward.

Leveraging the Agent Network

Daniel Webber: Let’s talk about the agent network and your growth. How much do you feel you can leverage your existing agent network for growth in these new markets versus adding new locations and expanding?

Robert Lisy:

When I say a new market like Dominican Republic, we already do a million wires a year.

I think that’s indicative that our network we have today will drive wires to these countries and they are driving wires to these countries and it’s our existing network. What I mean by existing, some of them may be new agents that are added, but they’re not necessarily specifically added for Dominican Republic or Ecuador or whatever.

There’s another part to this, though. The concentration of Ecuadorians in the US, Dominicans, Colombians, is much more concentrated than Mexicans or even Guatemalans. And so, you probably need 400-500 zip codes, 400-500 retailers, versus 8,000 retailers that we have for Mexico Guatemala to really tap into that business. Some countries you might need only a couple hundred retailers. So when you look at that across our salesforce, where we’ve got 70, 80 people between inside, outside and everything else, it’s not a big effort for us to target the retailers we need to drive wires to these other countries that have been secondary, tertiary countries for us.

Approach to Marketing

Daniel Webber: What do you need to add on the marketing side to drive that growth?

Robert Lisy:

Well, that’s the beauty of retail. You don’t really market it; we spend very little money – about a million dollars a year. All of our marketing budget is grass roots. Sometimes we’ll spend a million and a half to two, but it’s very, very basic. The way that you get wires is that we go out and visit agents that do wires today. We’re not bringing people to retailers today that never did wire before. We’re going to tap into a volume that exists in that retailer today.

When we’re going out, typically it’s a solution sale and we’ll go in and we’ll say, “Hey, I noticed that you have company X to the Dominican Republic. Are you happy with their service?” “Well, no, I’m not. There were some wires that weren’t paid and I don’t have the right bank account.”

Now we’ll start to offer them to our solutions as well. “Would you be interested in converting those wires to us if we could do this, this, this and this, if we could solve those problems?”

So it’s more about a solution sale to get the wires than it is about the market. We’re not spending a lot of money to drive people to retail. That’s the beauty of retail, while the opposite exists with online: it’s all about marketing and you’re spending marketing dollars, typically social marketing vehicles to really drive people to your site to do wires. So a very different proposition.

Western Union and MoneyGram spend money, but they spend it ineffectively. So I was watching a fight this weekend and in the corner it said Western Union. The branding is institutional, but it doesn’t do anything – there’s no call to action. So they spend useless money that doesn’t do anything for them.

We spend money at the grassroots, at retailers. Our small guys competitors will do the same, they have less resources, but at the end of the day, their quality of service, their inferior technology, the fact, they don’t deliver wires on time, bad banking relationships, all of that will tear customers away, regardless of how much they market.

Unit Economics and Customer Acquisition

Daniel Webber: Some players virtually give the service away for free. How do you think about the unit economics in the space?

Robert Lisy:

It’s not really though that they’re giving the service away for free. Their revenue per wire is not the problem. The problem is the cost of acquisition of the customer.

The consumer might pay $10, $11 all in with FX, but it costs a hundred dollars to bring him to the site. And he did three wires, maybe if you’re lucky, and he’s gone. So you’ve brought in $33 in gross margin, and now you have SG&A to come from that and you spent $100 to bring him to the site. That is the issue with online: the revenue growth can look great. The problem is the market really doesn’t deal really well with this, they don’t really look at the unit economics.

If people really asked the Wises, the Remitlys and the WorldRemits: what are your unit economics, what does it take to drive a customer and how much does it take? You wouldn’t care if they’re growing at a 100% or 200% because you can’t grow profitably.

That’s the thing that it’s really the challenge for those companies. And frankly, I’m looking forward to them going public, because more people are going to see that this is not – Look, online is going to get bigger and bigger, it’s going to get a bigger share of business. But I believe to Latin America for our core consumers, five years from now, more people will be sending money at retail, than online. A lot more: I think there’ll be maybe 70/30 at the very most. I think 10 years from now, they’ll still be a vibrant business.

So these guys that are fighting for a share today that’s 15 to 20% of the consumer and the most unprofitable segment in terms of acquiring a customer – that’s what’s going on today. I’d love for them to go public and have to lay out their wares and say, “Here’s what it costs me to get a customer, and here’s what that customer brings me.” I don’t think they’re going to be valued as highly as they are today without that information being public.

Profit can be unimportant for a long time as long as the gross margin makes sense, but you can’t make money on this because of the advertising costs; the unit economics don’t make sense.

I understand the advertising in SG&A, but it’s totally related to bringing in the customer. You can build up a big model and your SG&A stays relatively flat. But in this case, their biggest SG&A spend is totally related to how much their revenue grows. And that’s the problem with this.

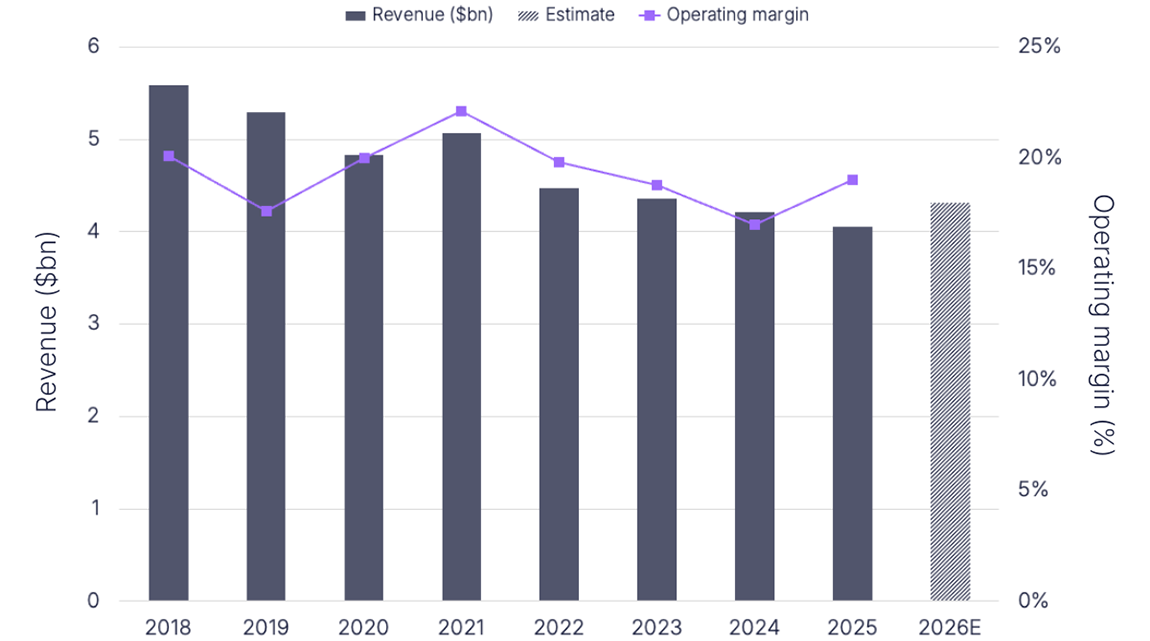

Figure 1

Intermex revenue and EBITDA margin, 2016 – 2020

Pricing and Principles

Daniel Webber: Your actual revenue grew slightly faster than your transaction count. What did that mean for pricing?

Robert Lisy:

What it’s due to is the average principle amount per send to Mexico and Guatemala increased. Remember, one component of our revenue is that we get an FX exchange. So our prices were relatively stable, but people sent more money. Because they sent more money, we made more on FX primarily, but even more wires were over a thousand dollars, so that we had more that were higher fees than $10. So it was driven mostly by the increased principle amounts.

Digital Business Growth

Daniel Webber: Your digital business is obviously growing and you’ve put out some nice numbers on it. What are you seeing on that customer and what proportion is retail customers moving over?

Robert Lisy:

It’s a small number, first of all, because we have a huge retail business and a small digital business. What we found, last time that we ran the numbers on this, and I think we need to do it again now after April, but we found there’s a group of customers that do both. Those that do both were more likely to come back to retail than they were to go to digital-only.

So those customers that shared, and did both with us, whether they came into retail or whether they came into digital, tended to do both over time. And if there was a leader, in terms of which way they migrated at the end of the day, more of them migrated, in the sample size that we had, towards retail versus digital.

In the backdrop of all that, we continue to work on our online business. We’ve invested a lot of money into front-end technology. The business continues to grow well. One of our third-party processing agreements that we have with Amigo Paisano is growing very, very nicely.

Our card business is beginning to grow; we just hired a guy from Netspend to come in. So we’ve been picking off a lot of talent; we just made an offer and he’s accepted to a guy from Western Union for our Latin American business on the ground there. We’ve always thought that internal Latin America is a big opportunity; it’s really just Western Union and MoneyGram competing there.

Figure 2

Intermex’s performance before and during the pandemic

Beyond the Pandemic

Daniel Webber: Of the trends you’ve seen, what do you think was transitional from the pandemic and so will revert back when things get closer to normal?

Robert Lisy:

Our quarter has been pretty normal, so it’s hard for me to say.We came back to work full scale in the fall last year; had our sales people back in the field. We kept everybody fully employed, even during the worst days of the pandemic, and they made calls to retailers instead of personal visits.

That’s part of the reason we grabbed so much business, because our competitors laid people off, but we kept people fully employed and went after the business. So for us, not much has changed.

The customer’s not going to change. The thing about our customers is, they have to go out to work. So people will ask, well, why wouldn’t they just go online? Well, because they’re going out to the fields to pick the oranges, the apples and the peppers, and because they have to go out to wash the cars they wash, or build the buildings they build. Our people are mostly critical workers, essential workers, who have been working all through it. So nothing really changed in their life.

If you went into the neighborhoods where we were six months ago, during what some people thought was still the height of the pandemic, our retailers were just as busy as ever. We had one quarter, the second quarter last year, [where it was down], but even then we still beat our EBITA year-over-year and actually did more wires than we did the year before. But then we were really very much back to normal by the third and fourth quarter. Fourth quarter, we grew EBITDA almost 30%.

For us, our customer is the essential worker. They’re still picking our crops, washing our cars, building our fences, building our decks and all the things they did. And that’s still going on. That’s been going on throughout the pandemic.

Leveraging the Intermex Platform

Daniel Webber: You’ve mentioned a bit about leveraging your platform, and potentially even your own network. How are you thinking about opening up to other players?

Robert Lisy:

We do the platform now. Our digital platform, we sell it, we sold it to three companies today. We’re processing for them, their early stages, and we’ll be selling it to more people. So we absolutely believe that we can be co-branded – because it’s necessary, we’re the branded entity and the license entity so we’ve got to be co-branded with these guys – but we feel we’ll continue to do more and more of that.

The retail network, if it’s worthwhile, but what we don’t want to do is distract our salespeople from a $5 gross margin Mexico transaction to be selling a phone card or something like that where we make 4, 5 cents. It’s not worthwhile.

Some of our less savvy competitors, even the small guys, have gotten into being distracted and trying to do too much. And there’s still a lot of opportunity out there with Latin American money transfers.

So we will put these through our network as they make sense. We have our own money order product we do today. We have a bill payment product we do in conjunction with someone else, but we do these things only if they add value, not just to add more problems.

The last piece is our payer network. We have our own private network – about 10% of our wires go through our own retailers that no one else accesses, and we’re likely not ever to share that with anybody because we see it as a real competitive advantage. The rest of the retail payer network, is a network that anybody can get. They might not get the same prices, the same co-op promotion from the lead guys, but they can access it, it’s easy enough to access.

Geographic Expansion

Daniel Webber: We’ve already talked about the opportunity to go to some of the other states, and you’ve also mentioned Canadian outbound, African pair markets. How are these different geographies coming along?

Robert Lisy:

We’ve been in every state but Hawaii for a long time. So it’s just a matter of how early stage. The states west of the Mississippi tend to be earlier stage, but it can be a little misleading because California is a later state for us with a huge amount of opportunity and it’s also our biggest state. States like Arizona, Nevada, Colorado, Utah, California, Texas, those are all huge growth opportunities for us, and they continue to be, and we’re going to be focusing on them even a little bit more this year as our business heats up. We’re ahead of our guidance. We’re going to put some more sales people on the street to build our agent network even faster in those outbound countries.

Canada continues to grow, but Canada is not going to be anything like a US state. It’s small, it’s a nice place to be. Today we’re still in Ontario, Canada and it’s continuing to grow.

Canada’s outbound market is much more diverse. In the US, you can make a living off of just sending to Latin America, but in Canada you need Vietnam, and you need a lot of other countries to be able to attach to the entire market. It’s tougher and so we’ll work through all of that.

Africa, we still think there’s a big opportunity for us, but it’s growing slowly. We think it’s going to be a great next group of countries to be in, but it’s going to take some time to build that. Nigeria – everybody will tell you that Nigeria has changed now where they don’t want wires coming in their local currency. They want it to come in dollars, so we’re making some adjustments as everybody is there. And that’s really key in the market.

Daniel Webber: Bob, this has been great. Thank you for your time.

Robert Lisy:

Thank you.

The information provided in this report is for informational purposes only, and does not constitute an offer or solicitation to sell shares or securities. None of the information presented is intended to form the basis for any investment decision, and no specific recommendations are intended. Accordingly, this work and its contents do not constitute investment advice or counsel or solicitation for investment in any security. This report and its contents should not form the basis of, or be relied on in any connection with, any contract or commitment whatsoever. FXC Group Inc. and subsidiaries including FXC Intelligence Ltd expressly disclaims any and all responsibility for any direct or consequential loss or damage of any kind whatsoever arising directly or indirectly from: (i) reliance on any information contained in this report, (ii) any error, omission or inaccuracy in any such information or (iii) any action resulting there from. This report and the data included in this report may not be used for any commercial purpose, used for comparisons by any business in the money transfer or payments space or distributed or sold to any other third parties without the expressed written permission or license granted directly by FXC Intelligence Ltd.