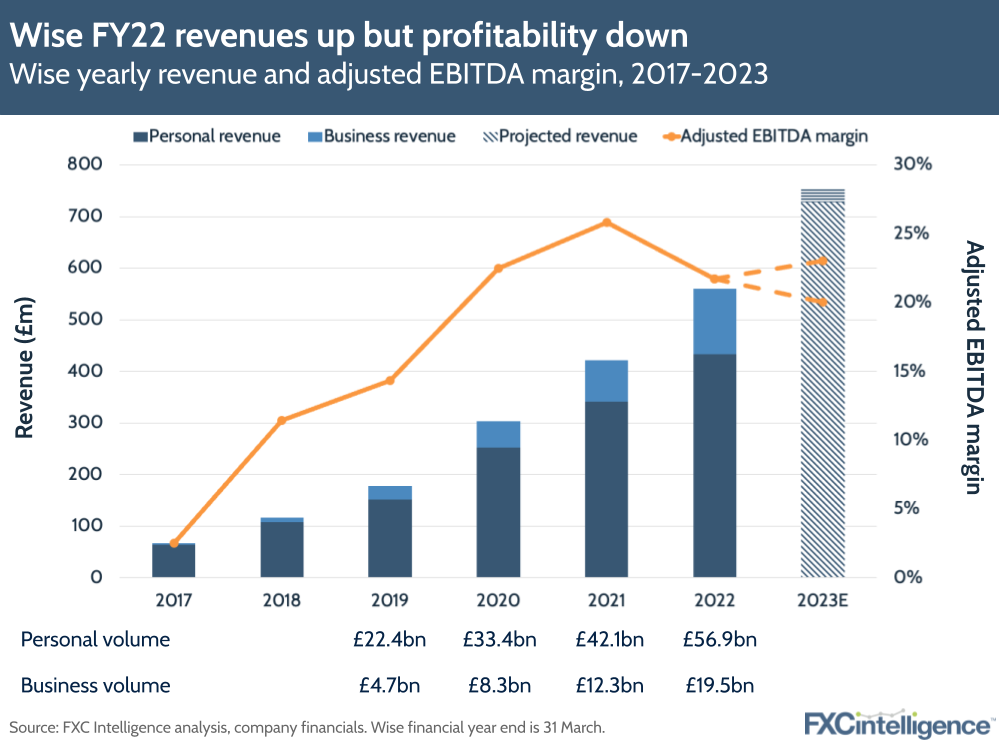

Wise reported its first full year earnings as public company this week, for FY22. Whilst growth continues to be strong, margins substantially declined. This not-quite-as-profitable growth, potentially exacerbated by a Financial Conduct Authority investigation into Wise CEO Kristo Kärmann’s taxes, caused a sharp drop in the company’s share price this week, down over 20% to all-time lows.

Covering calendar year Q2 2021 – Q1 2022, Wise’s FY22 results beat its previous projections, with the company increasing revenue by 33% year-on-year and gross profit by 43% YoY. Some of the key takeaways:

- The company’s EBITDA margin declined from 26% to 22% YoY and is forecast to remain at lower levels for FY23. Wise attributed this to increased investment in its teams, products and marketing. Investors may be fearing these cost levels may be required to sustain the growth, pushing longer term profitability down.

- The newer Business segment continues to climb at a faster rate than Personal, with the number of Business customers increasing 34% compared to Personal’s 24%. Business volume per customer also increased 18% to £47,700, compared to a 9% increase in Personal volume per customer.

- Overall, Wise saw its customer base grow 29% between Q4 2021 and Q4 2022 to now stand at 4.6 million, with overall volume increasing by 40% to £76bn for the year.

- The company also reported gains in price and speed, with average customer prices dropping to 0.61% in Q4 2022, while 49% of transfers are now instant.

- The company’s multicurrency Wise Account saw an increase in adoption, seeing launches in Brazil, Malaysia and Canada as well as the launch of Assets in the UK. This follows Wise seeing more of its customers using more features, enabling it to realise higher revenue per customer.

- In terms of geography, the company’s revenue by region remained relatively similar in terms of share to 2021, showing the growth is coming from all parts of the globe. Europe’s share grew from 32% to 33% of revenue, while the UK dropped from 23% to 22%. Asia Pacific remained flat, while North America increased from 17% to 18%, with the rest of the world seeing a half-percent drop in share.

- Looking forward, Wise projects revenue to grow between 30-35% in FY23, while its EBITDA margin is expected to remain at or above 20%.