PayPal’s net revenue rose 9% to $7.0bn (10% excluding the impact of FX) in Q1 2023, driven by a 10% rise in total payments volume to $354.5bn.

Better-than-expected ecommerce activity gave a boost to PayPal’s unbranded checkout solutions, particularly merchant payments service Braintree. However, despite beating expectations, PayPal’s share price fell by around 15% in the wake of its results. Various analysts attributed this to a lower-than-expected operating margin outlook for 2023 and the tighter margin ecommerce part of the business driving its growth.

PayPal’s total payment volume (TPV) was driven by a 13% rise in payment transactions to 5.8 billion, with transaction revenue growing 6%. Branded checkout and unbranded processing volumes grew 6.5% and 30% respectively, with outgoing CEO Dan Schulman claiming that the company’s unbranded volumes are now roughly equal to that of similar products from Android and Stripe. Meanwhile, volumes across P2P solutions (including PayPal, Venmo and Xoom) rose 2% to $91bn.

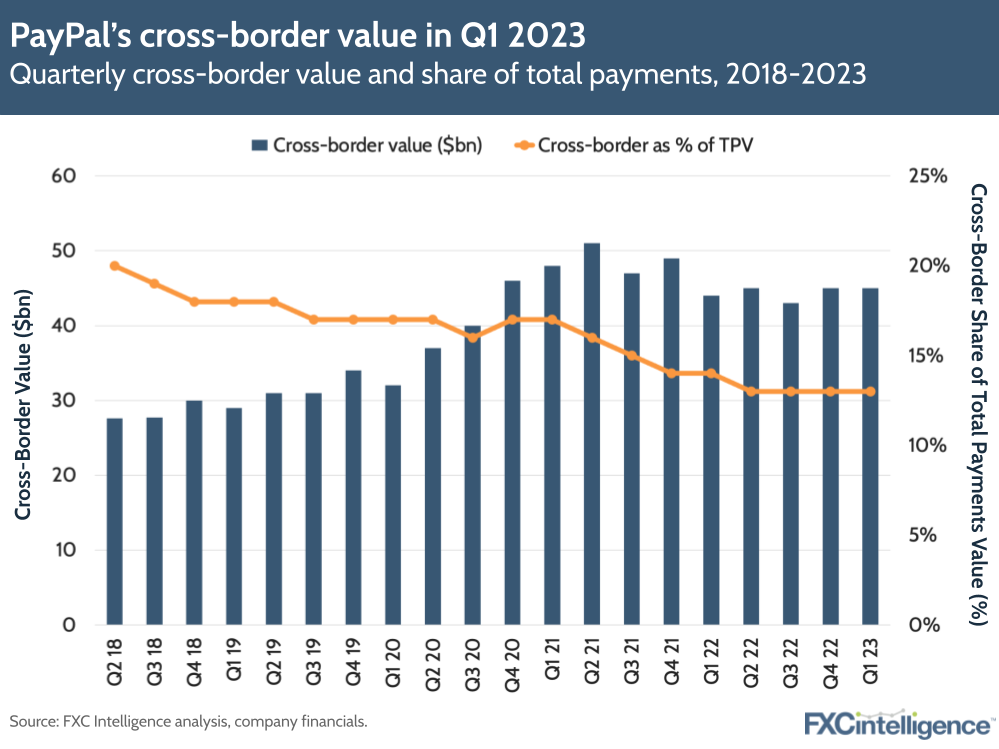

Cross-border volumes were flat at $45bn (up 4% excluding FX impacts), which accounted for a 13% share of PayPal’s overall TPV. This share remains lower than during the pandemic, but the company notes that it is primarily ecommerce related, meaning travel recovery hasn’t had much of an impact. Volume continued to be driven by payments between European countries, but was offset by softness in the EU-UK and US-China corridors.

Hidden away in the earnings call was one of the most important comments from the CEO for our sector: “That [cross-border payments], of course, has a higher yield to it overall.” This is confirmation that cross-border disproportionately positively benefits revenue at PayPal, but the exact numbers are not separately reported.

PayPal ended Q1 with 433 million active accounts, up 1% YoY (though this fell compared to Q4 22). Of these accounts, 45% were outside the US, and while international revenue accounted for a lower amount of overall revenue this year at 41%, it still grew 7% on a FX-neutral basis. By comparison, US revenues grew 13% YoY.

These revenue gains pushed the company’s non-GAAP operating income up to $1.6bn, while the company’s operating margin rose around 200 basis points to 22.7%. Schulman said that operating expenditures could decline by as much as 10% this year as the company finds new ways to reduce costs and drive profits. For example, it may be able to use merchant data-driven AI systems to help reduce costs and create better services.

Looking forward, PayPal still hasn’t given specific revenue guidance for the full year, but did say it expects its operating margin to expand by 100 basis points. In Q2, it anticipates revenues will grow by 6.5-7% on a spot basis.

How does PayPal’s pricing compare to other ecommerce players?