Last week, Stripe announced a new Series I funding round that has seen it raise over $6.5bn at a valuation of $50bn – significantly below its valuation high of $95bn in March 2021. The drop reflects a more broadly muted market, which has seen companies make considerable cuts to their workforces and provide lower projections for a year that is already being impacted by a cost-of-living squeeze and where many still expect to be impacted by a global recession. So, with this in mind, what is driving valuations for payments companies in this more cautious time?

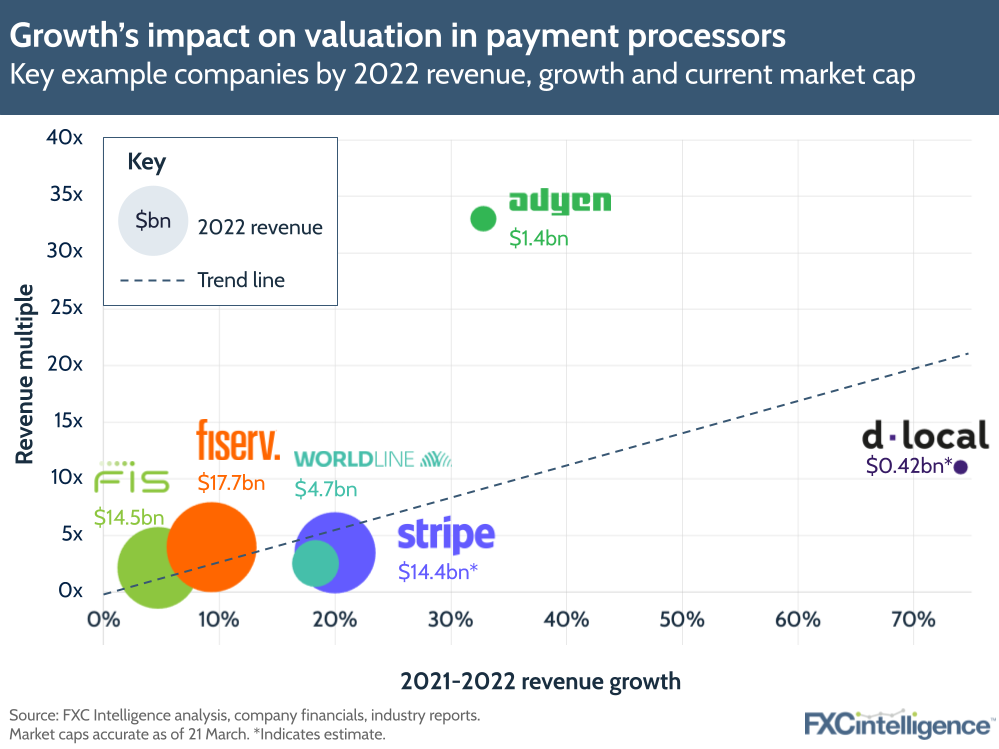

Payment processors, whose 2022 revenues are often into the billions and who have market caps to match, do see a limited correlation between valuation and revenue growth. Long-established players FIS and Fiserv, for example, both saw sub-10% growth year-on-year, but have significant valuations, likely driven by significant revenue. This is giving them revenue multiples (current valuation divided by 2022 revenue) that are firmly on the trend line for the sector, albeit at the low end.

Meanwhile, newer players that are on a sharper growth curve are seeing greater valuations and therefore revenue multiples as a result, with Adyen, whose revenues remain low compared to many competitors, being the strongest example of this.

Interestingly, Stripe now sits in the middle of this pack, between the established players and dLocal and Adyen’s high growth-led positions. Increased growth may therefore help Stripe push its valuation higher, but it does suggest that its current valuation is more rational than the level it held a few years ago.

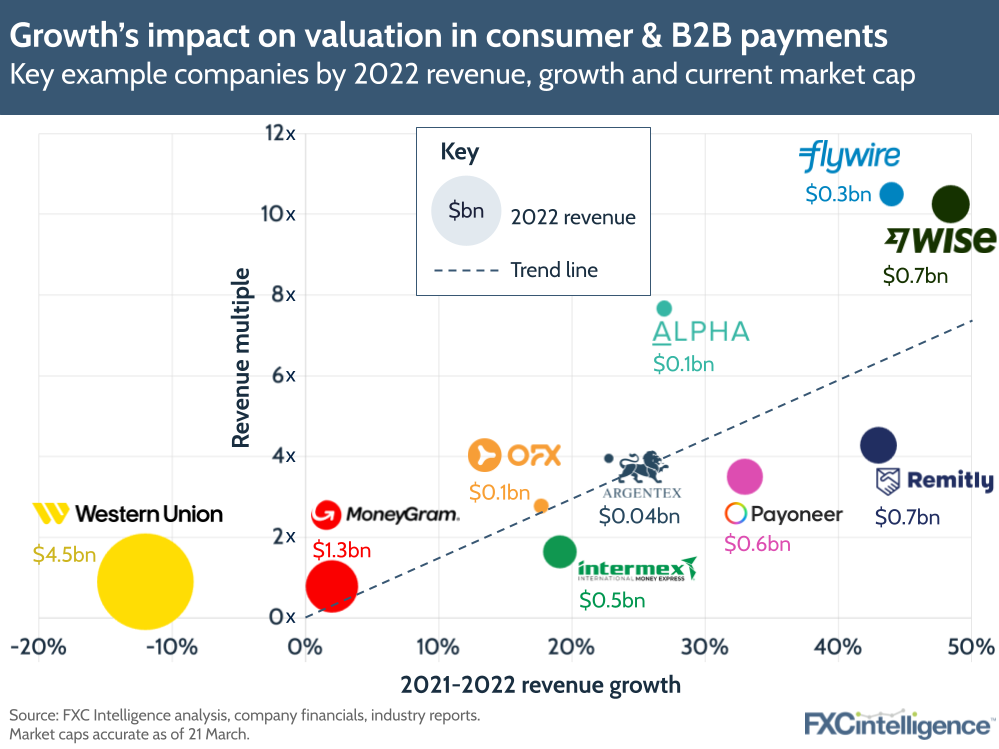

By contrast, consumer and B2B payments companies have a clearer link between revenue multiple and growth, highlighting the fact they are all have relatively small market shares and plenty of opportunity to expand.

Wise and Western Union are some of the outliers. For Wise, this is likely to be because is seeing its strong growth alongside solid profits.

Western Union, meanwhile, stands out as the one player with declining revenue in the group and a share price at historic lows. New CEO Devin McGranahan has asked investors for time as part of a three-year turnaround plan and for now many are watching on the sidelines to see the results.

In an increasingly conservative investment environment, growth still matters, but either profitability or a clear path to it are now just as important too.