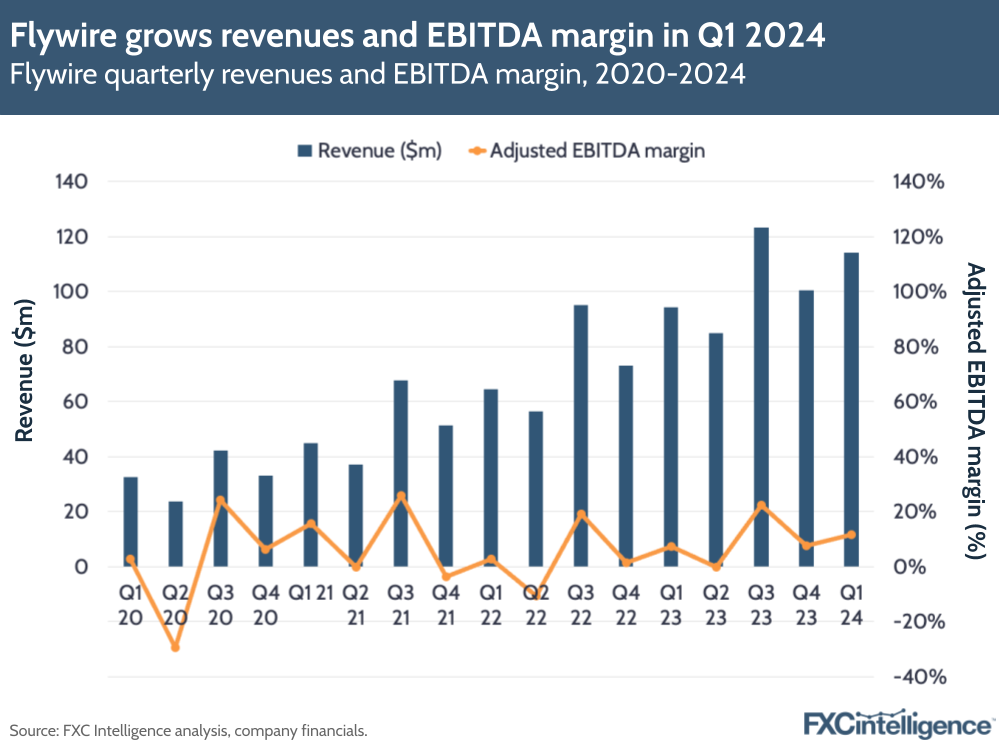

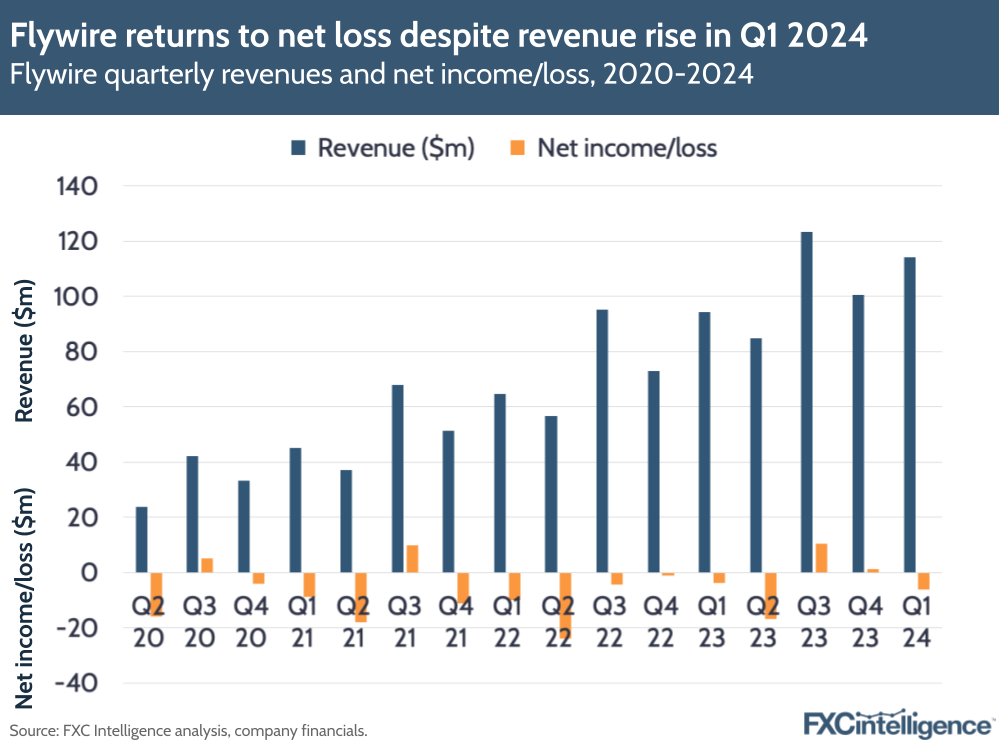

US-based Flywire saw revenues rise by 21% YoY to $114.1m in Q1 2024. The company is continuing to expand its client base across its education, travel, B2B and healthcare verticals. However, changes to student admittance policies in Canada were a headwind during the quarter, contributing to a lower revenue growth figure than Q1 2023 (46%).

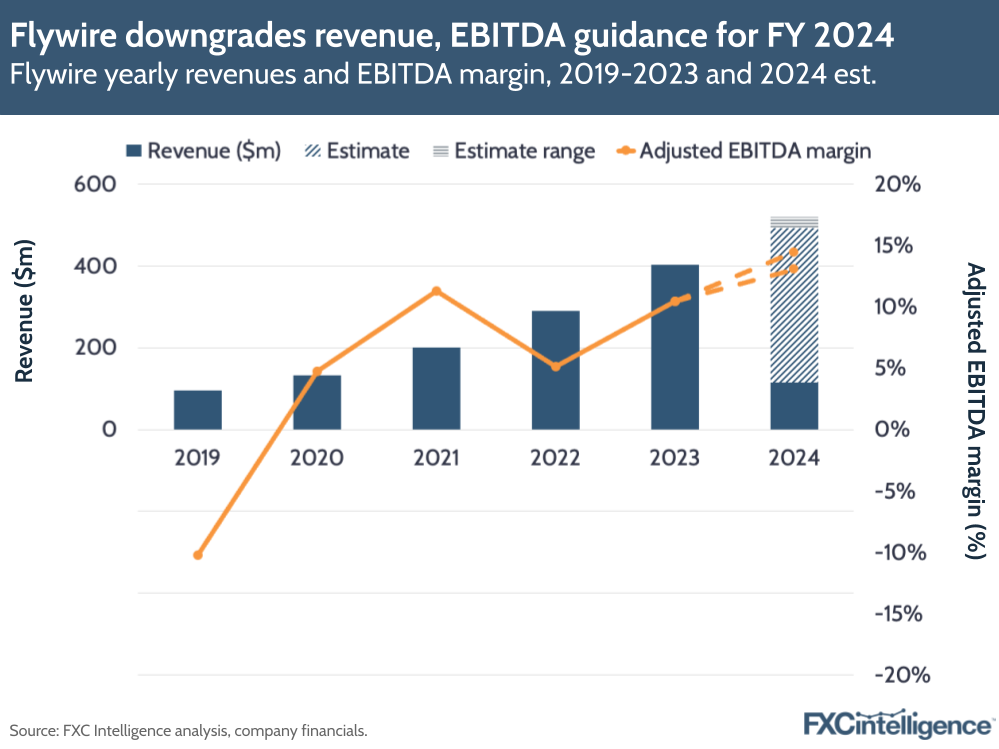

On the back of its results, Flywire has updated its guidance for FY 2024. It now expects revenues over the full year to rise by 22-29% YoY to between $491-519m (compared to the $501-535m it forecast in Q4 2023), while it expects adjusted EBITDA to rise by between 52-79% to $64-75m (compared to $65-76m previously).

In Q2, Flywire is anticipating revenue of $99-108m and an adjusted EBITDA of between $1-4m, providing a projected adjusted EBITDA margin of 1-4%. The company has adjusted this guidance to respond to FX impacts, as well as shifting expectations regarding its education clients in Canada.

For the full year, the company said that it was maintaining top-line growth expectations on a constant currency basis, and anticipated its adjusted EBITDA margin to expand by 320 bps (at the midpoint of its FY 2024 guidance range). Based on the numbers it has provided, its projected adjusted EBITDA margin for FY 2024 is now 13-14.5%.

Key revenue drivers for Flywire in Q1 2024

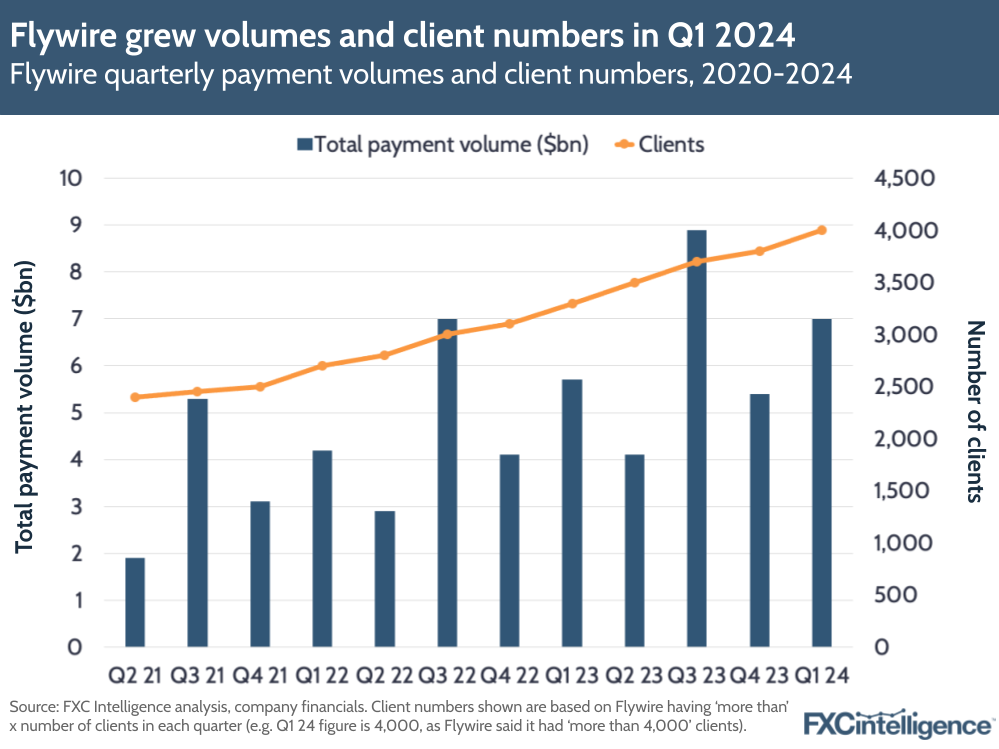

Revenue minus ancillary services rose by 24% to $110.2m in Q1, with growth driven by a 23% rise in total payment volumes to $7bn. Meanwhile, Flywire’s adjusted EBITDA nearly doubled to $13.2m, giving a margin of 11.6%.

Revenue growth was bolstered by better-than-expected volumes from higher education clients in the UK; strong growth from new travel accommodation clients in Europe and Asia; and the company’s recent acquisition of student admissions tech provider StudyLink.

Gross profits also increased to $70.4m, resulting in a gross margin of 61.7%, though the company’s net losses were slightly higher at $6.2m for Q1, compared to $3.7m. Flywire signed more than 200 new clients in Q1 – a new quarterly record – so that its total now exceeds 4,000 clients. This number is nearly two times higher than it was when Flywire filed for its IPO in 2021.

Having said this, Flywire is also cross-selling and expanding services provided to its existing clients, having previously reported a 125% annual dollar-based net retention rate in 2023.

Flywire saw a 20% YoY pipeline growth across all verticals, with B2B and healthcare reportedly giving their highest all-time pipeline creation in a single quarter, and travel breaking its record for projected annual recurring revenue (ARR) signed during the quarter.

Flywire continues to report that B2B has a significantly higher total addressable market than other payments segments, which reflects research that FXC Intelligence has carried out into the topic (see our projections for the global B2B cross-border payments market by 2032).

Flywire expands verticals but student visas remain a headwind

Education remains a key vertical for Flywire, but the company acknowledged that there have been tightening student visa rules in some countries (Australia and the UK for example). The concern is that shifting rules could reduce applications to study abroad, which in turn might affect cross-border revenues for Flywire.

Flywire CEO Mike Massaro said that the company had been resilient to such changes before, and was confident given that Flywire nearly doubled its higher education revenue in the UK in Q1 2024, despite the fact that there have already been some policy changes in the country. He also said the company continued to believe in the long-term growth of the international student market, and had also seen strength in other countries such as Australia, the US and China.

During the earnings call, executives returned to the issue of Canada, which earlier in the year announced new policies that led to a pause in study permit allocations, which could weaken Canada as a market for Flywire. The company did note that it had seen a high single-digit percentage headwind related to its higher education business in Q1 2024.

Massaro said that a number of Canadian clients had noted that recent study permit allocations had been better than expected with a “rolling ramp” back to normal levels of admissions.

He also noted in the call that the education segment will continue to benefit from several other factors, including growing tuition fees (which in turn grow average transactions sizes); growth in international students (based on consistent growth over the last couple of decades, even normalising for Covid); and a growing TAM based on Flywire expanding its services with existing clients.

This land-and-expand strategy is also how the company is trying to approach all its verticals. New CFO Cosmin Pitigoi explained how the company’s net revenue retention rate had remained stable over the year, due to a growing TAM across the company’s growth verticals combined with the company expanding across its existing clients.

“The opportunity to solve these multidimensional customer problems starts with large, complex cross-border payments, but increasingly opens the door to cross-selling into domestic capability,” said Pitigoi.

Flywire’s investment strategy

Flywire reiterated its intention to increase investment in sales and relationship managers by more than 15% in aggregate, spread across verticals and geographies across 2024. This, the company said, is already delivering gains in its travel vertical particularly, such as in South Africa, where it has seen a three-fold increase in clients over the last 12 months.

However the company is also focused on keeping costs contained, with expenses as a percentage of revenue down 6% versus Q1 2023. Moving forward, the company is continuing to optimize its go-to-market capabilities to expand its diversified client base as well as grow its ‘Flywire Advantage’ for clients.

The focus on growing Flywire’s smaller verticals – e.g. healthcare – could become more important as policies for international students create more ambiguity over its education business. However, the company has seen resilience in this area and believes international student numbers worldwide will continue to grow.