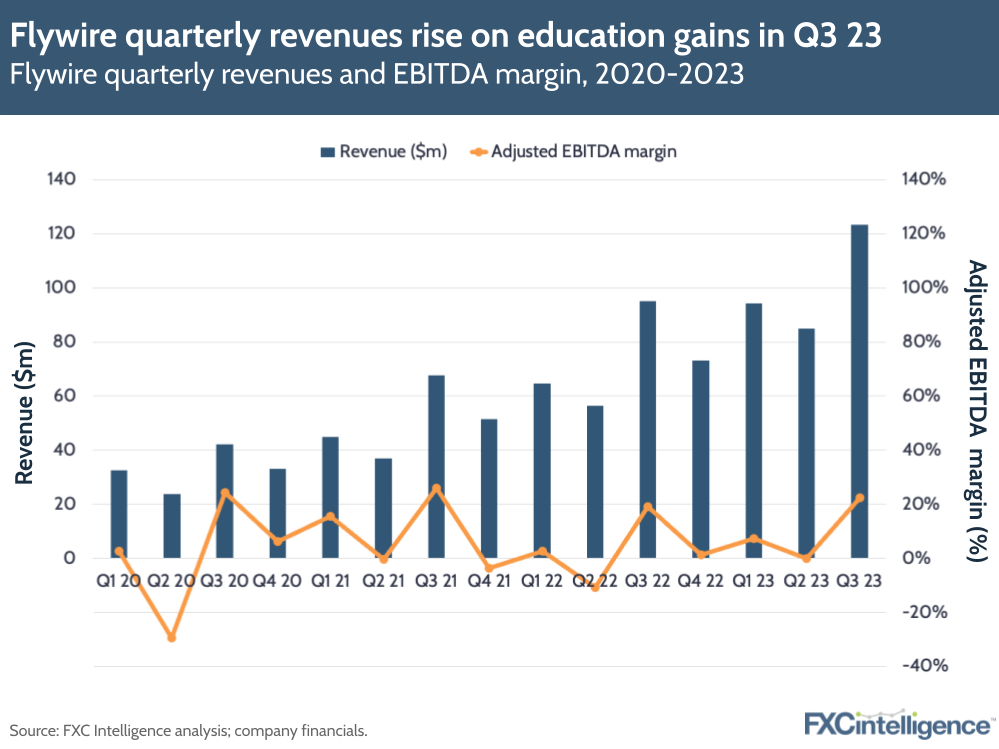

Education payments specialist Flywire has reported total revenues rising by 29.5% to $123.3m in Q3 23 – minus ancillary services, revenues rose 31.4% to $116.8m – while adjusted EBITDA rose 51% to $27.5m.

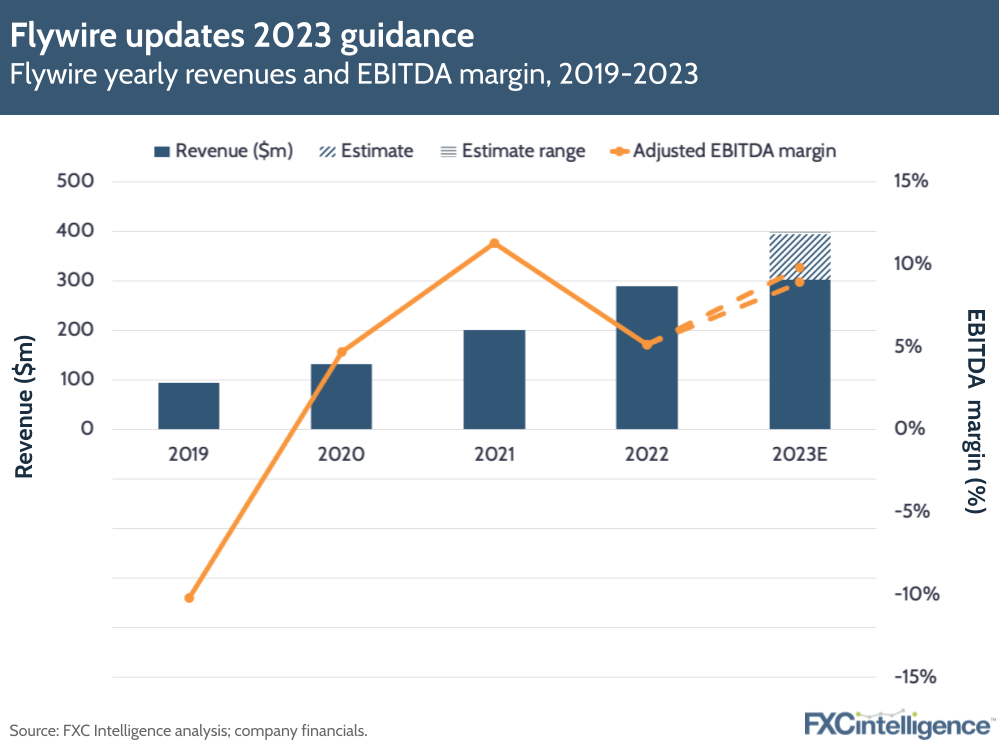

However, after some growth impacts this quarter, Flywire has narrowed its guidance for the year to $394.1m-399.3m (compared to $392m-408m in Q2 23), as well as changed its adjusted EBITDA projection to $35m-39m, previously $33m-39m.

It’s been speculated that this updated guidance prompted the company’s share price to fall by over 30% after earnings, as well as FX headwinds and some delayed deployments of solutions in the education and healthcare verticals.

Flywire’s growth drivers in Q3 23

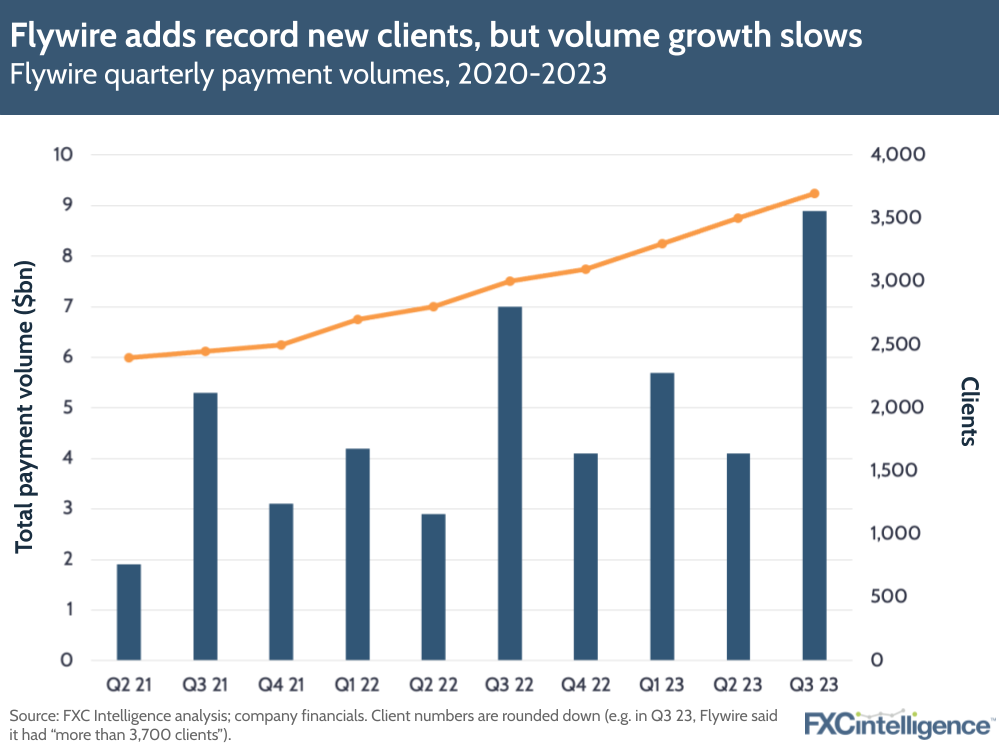

Flywire’s revenue was driven by 26% payment volume growth, powered by higher revenues in the company’s education vertical for Q3, when many international students pay fees through Flywire. It reiterated its core pillars driving gains, including growing with new and existing clients; expanding to new industries and geographies; and acquisitions.

In particular, Flywire noted strong growth in business from public sector higher education institutions across European countries including Spain, Finland, Lithuania and France.

Education continues to be a key focus for the company, but it also noted that travel and B2B were its fastest growing teams in the company. Travel payments volume saw 100% growth over Q3 2023, and new travel clients made up the majority of 185 new clients signed – a record for the company.

Having said this, payment volume growth was slower than in previous quarters (for Q3 2022, it was at 40%), which in turn drove lower, though still solid, revenue growth for Q3. China and the UK were both mentioned as seeing growth in cross-border volumes, as was India, but here Flywire saw lower volumes than expected in education.

Flywire also mentioned the impact of FX fluctuations, particularly the strength of the dollar, which impacted its reported results by $1.4m, and said that this could grow to a $2.5m impact in Q4. Also, delayed solutions in Flywire’s healthcare and education verticals affected revenues by a seven-figure sum, said Flywire President and COO Rob Orgel.

Flywire’s new acquisition in Australia

The company also announced its latest acquisition this week in the form of Australian student admissions company StudyLink. Flywire says it is acquiring StudyLink to accelerate its business in Australia and capture more of the market, where it claims there are around 620,000 international students and a tertiary education TAM worth $11bn.

From a revenue perspective, the StudyLink deal isn’t massive, as the company said it was a $6m-7m business in terms of revenue for the full year. When asked about acquisition strategy during the call, Flywire said that it was making acquisitions that fit with its core growth pillars, but that it continues to consider deals of all sizes and expects more opportunities to come forward in quarters to come.

Despite the investor response to some setbacks this quarter, Flywire has maintained growth and profitability and continues to pursue opportunities globally. For example, alongside India’s UPI and PIX in Brazil, Flywire has also enabled Netherlands’ iDEAL real-times payment network as a new payment method.