China’s Cross-Border Interbank Payment System has seen growing use for RMB-denominated cross-border transactions and in April broke its record for single-day transaction value, with RMB 1.22tn ($178.5bn) passing through the system. Below, we explore what’s driving growth for CIPS in 2026, as well as how it fits into China’s wider push to expand cross-border yuan usage.

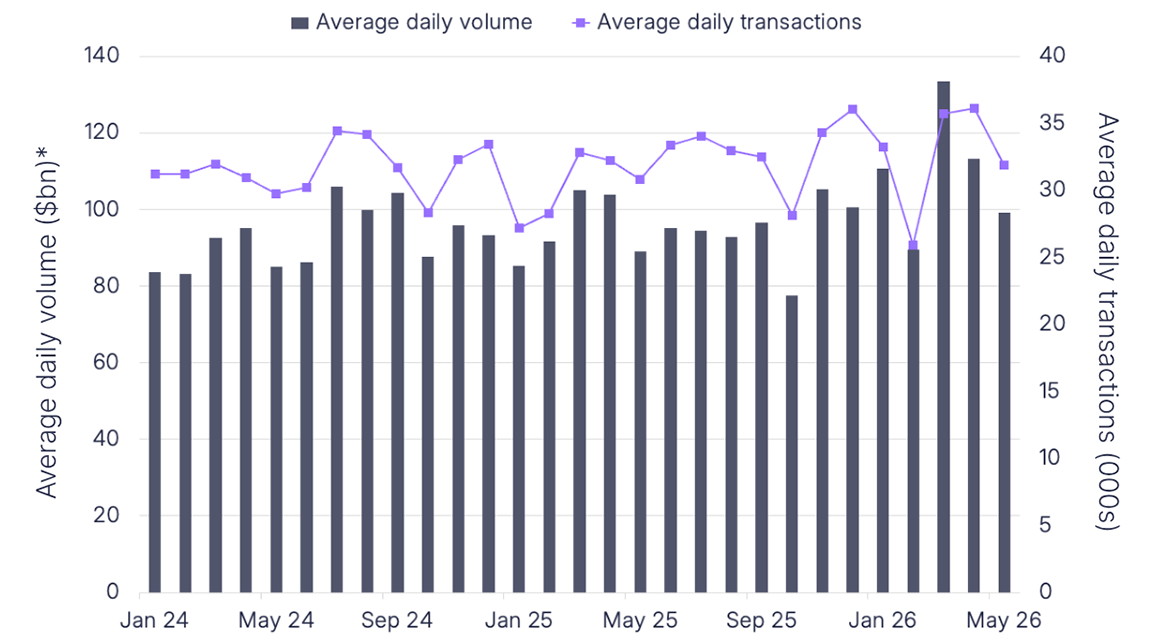

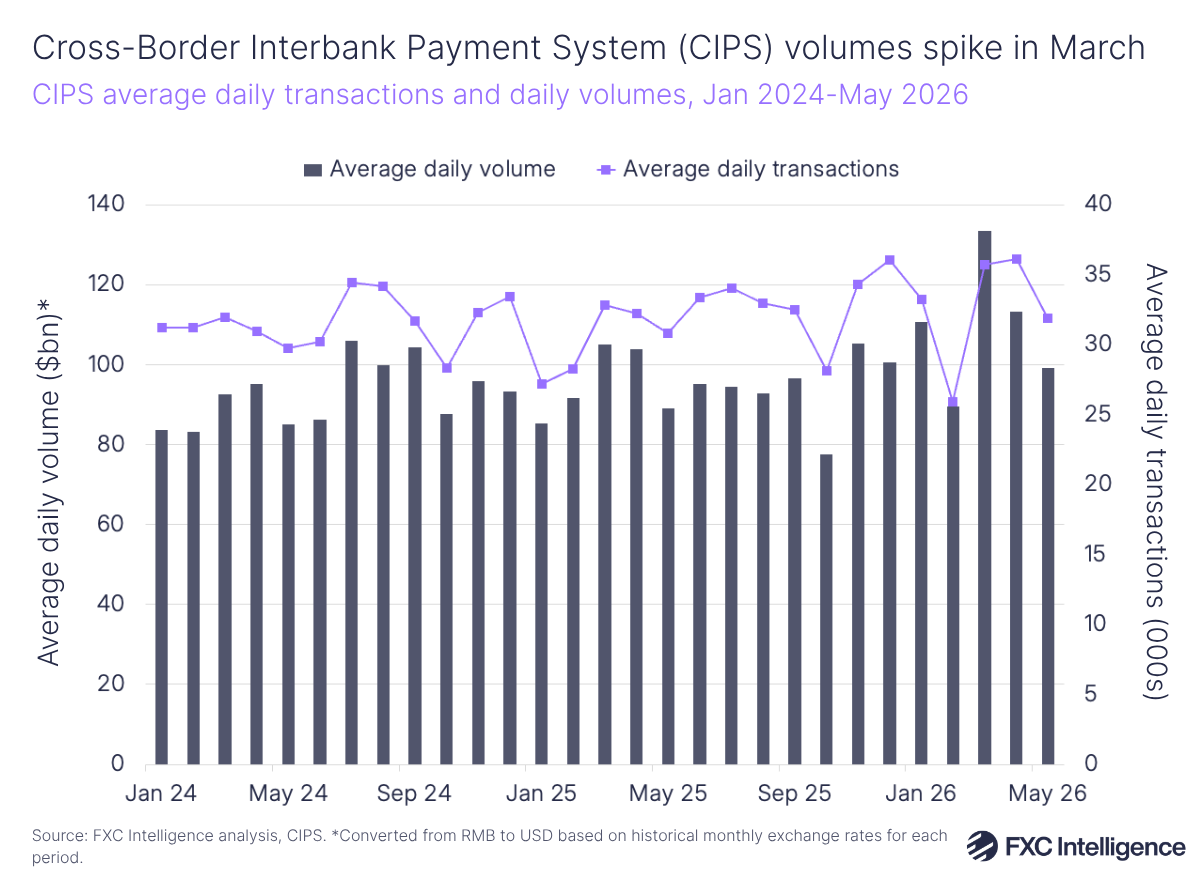

The average daily volume of transactions through CIPS broke records in March at RMB 920.5bn ($133.5bn), rising 20% YoY, while the number of transactions rose by 9% to approximately 36,000. This figure has since tapered back down to RMB 674bn ($99bn) as of May 2026, though this is still an increase of 5% YoY overall.

The surge in transactions in March has been linked to events in the Middle East, specifically coming after the US attacks on Iran. The region reportedly saw a rise in demand for the yuan for settling oil transactions as tensions rose, with the Council for Foreign Relations arguing that the rise in transactions aligned with reports showing Iran’s growing demand for large RMB toll payments in the Strait of Hormuz, in addition to renewed US threats of sanctions on countries aiding Iran.

Ding Shuang, chief economist for Greater China and North Asia at Standard Chartered, told the South China Morning Post that rising volumes could also be linked to the yuan’s stability during the period, as well as China’s continued investment in cross-border payments infrastructure and the growing number of participating financial institutions using CIPS.

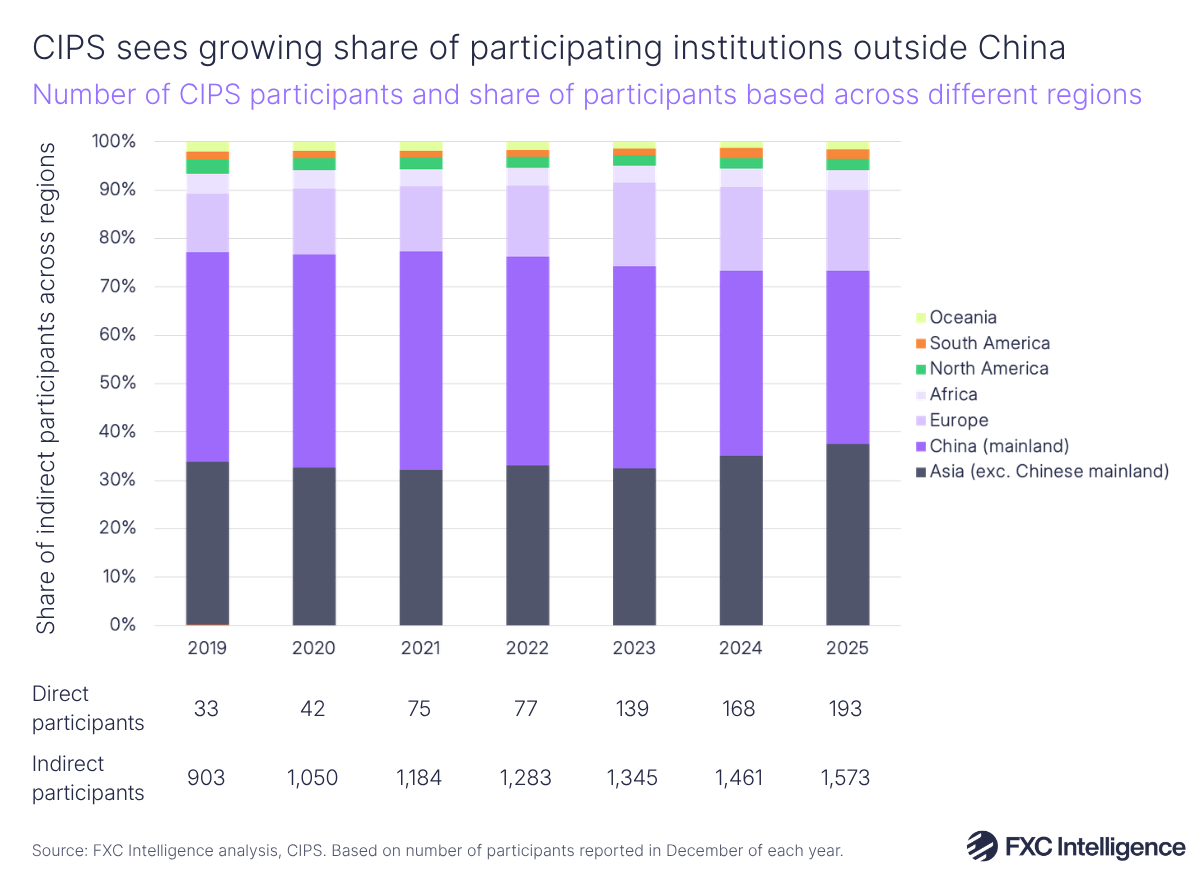

Overall, the number of financial institutions that have joined CIPS had risen to 1,791 as of the end of Q1 2026. This includes 194 direct participants, which directly open an account and are able to send and receive messages in CIPS (i.e. having direct access to RMB clearing and settlement), and 1,597 indirect participants, which have access to services provided by CIPS through direct participants. This is still significantly lower than the 11,000+ institutions hosted by Swift, though comparisons made between the systems aren’t one to one as Swift remains a global messaging system, with CIPS still relying on Swift to send financial messages for a large proportion of transactions.

73% of indirect participants are from Asia, with institutions from the Chinese mainland accounting for 35% of the share, down from 43% in Q1 2020. Meanwhile, institutions from Asian countries outside the Chinese mainland account for 38% of the share, up from 34% over the same period, showing the growth of the system’s importance in neighbouring regions since the start of the decade. Europe is the next leader in terms of share with 17% in Q1 2026, followed by Africa (5%), with North America, South America and Oceania accounting for around 2% each. Overall, indirect participants from non-Chinese mainland countries accounted for 65% of the system’s participants, highlighting a gradual rise from 57% in Q1 2020, showing a growing demand to connect from regions with strong trade links to China.

CIPS’s growth should be seen in the context of China’s broader efforts to expand the use of RMB in cross-border transactions. As we reported earlier this year, the yuan saw significant growth for non-bank cross-border payment transactions in 2025, but remains in much lower use than currencies such as the US dollar globally. RMB still accounts for a small portion of global payment volumes through Swift, with Swift’s Global Currency Tracker data for June 2026 showing it accounts for less than 3% of global payments, versus 51% for USD, 22% for the euro and 7% for GBP.

Having said this, CIPS’s recent growth highlights how macroeconomic events can cause a shift in currency usage, and its expansion over time – particularly to regions beyond China – underlines an increasing move from the country to build out payments infrastructure to support future growth. The country has also made progress with its digital yuan initiative, and this week reportedly signed an agreement with 26 financial institutions to join a new integrated cross-border settlement platform.