First, credit where credit is due. The Financial Times continued to report its allegations about Wirecard for years, facing a barrage of criticism and lawsuits. In the end, it proved to be right and this is a great lesson in truth-seeking and perseverance.

As the dust is settling on the rest of whatever Wirecard’s life now is, we can reflect on a few points:

- This was not a Covid-19 related collapse

The timing is simply coincidental but the allegations for fraud are now a criminal matter. Wirecard first postponed and then missed a deadline to file accounts (which EY wouldn’t sign off on) and had to admit what was going on. - Wirecard was processing payments for many known fintechs

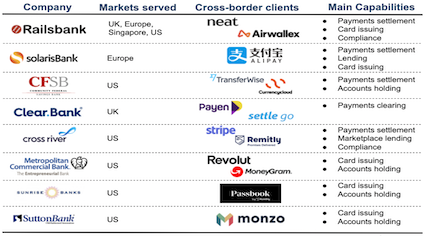

(Payoneer, Curve, Revolut and plenty of others)

The questions every fintech should be asking now is what is my redundancy plan and how quickly could I put it into effect? More importantly, how much is it going to cost? - How will trust in fintechs be affected?

Wirecard was worth over $20bn at its peak and it was listed in Germany’s prestigious DAX30 market, where many pension funds in Germany simply invest in all players. Although Wirecard itself and the German regulator BaFin liked to call the company a fintech, it’s been argued that it was more like the bank behind the fintechs. - How much can you blame the regulators and the watchdogs?

A lot is probably the right answer. It is clear that regulators wanted Wirecard to be a success, both independently and for the fintechs it was supporting. Many forward thinking regulators around the globe, such as the UK’s FCA or Singapore’s MAS, have been great at giving springboards and room for new fintechs to grow. Fintechs bring new products to market, increase competition and virtually always benefit the end customer. But will more oversight now be needed and should some freedoms be limited?

Do we all go back to trusting the banks?

To answer this, let’s look to the words of Revolut, one of Europe’s most valuable fintechs (Revolut recently raised over $500m reaching a valuation of $5.5bn).

When Revolut needed to comfort its customers over the past week as Wirecard filed for bankruptcy and Wirecard’s UK assets were temporarily frozen, well… Revolut had to turn to the banks. See for yourself…