Fleetcor is a US public company best known for fuel cards and corporate payment products. It stunned the market when in 2017 it paid $675m for Cambridge Global Payments, a historically traditional FX payments and currency risk management company that had begun offering more automated and tech-powered products.

Did Fleetcor have a strategy in mind different from everyone else? The results suggest its bet paid off.

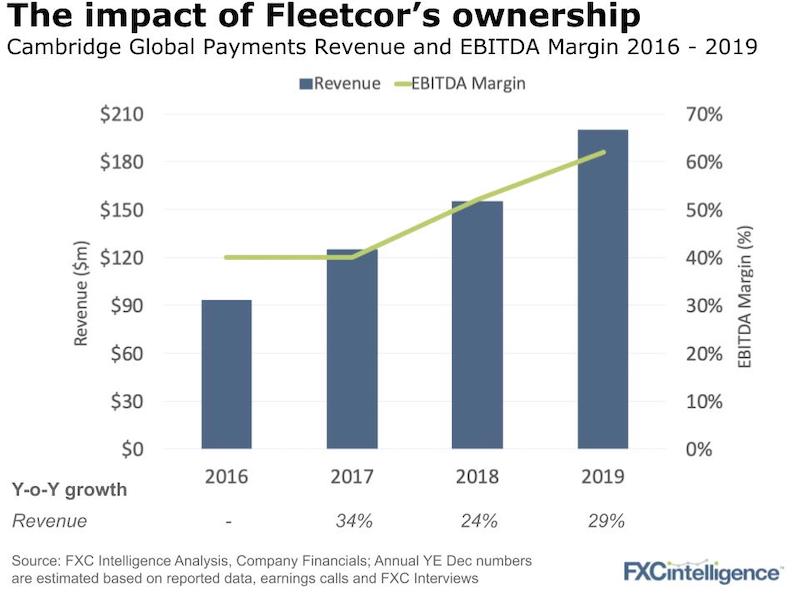

(Note that since Fleetcor does not report on Cambridge separately – it includes it within its corporate payments division – we’ve pieced the numbers together below for you).

There are many benefits to being bought by a big strategic player. Fleetcor is an M&A machine and, in a period of three years, has pulled the EBITDA margin of Cambridge up from c.40 to 60% (although it is not clear what a standalone EBITDA level would be). Applying the same EBITDA multiple as the acquisition (13.5x) would make Cambridge worth north of $1.5bn.

To frame this valuation, Western Union Business Solutions (WUBS), the biggest standalone player in the space, is twice the size but far less profitable (in 2019 its EBITDA margin was 22%). WUBS was reported to have been up for sale in 2018 for c.$500m but there were no takers. Fleetcor were the odds-on favourite to buy WUBS but have instead ended up adding more value organically.

Not bad going at all. What’s driving this growth and increase in value according to President Mark Frey (aside from Fleetcor’s ability to drive margin improvement)?

- A core B2B currency risk offering

Cambridge offers the full suite of spot, forwards and options products to mid-size and up companies. Few players at scale actually offer this now if you include options in the mix (Afex, Global Reach). Alongside this sits a well-oiled, traditional B2B direct sales model that has kept chugging along. - Product expansion into Payments as a Service

A handful of new products have helped fuel growth. Cambridge’s invoice automation product, formerly focused just on the legal sector, is being repositioned as a general offering. The second is its emerging markets payment business focusing on the last mile of the payments’ delivery even in countries with complex jurisdictions. The target customer here is Tier 1 banks and, increasingly, payment aggregators (but not startups or smaller fintechs, which others have chosen to target). - A model shifting to partnerships and one to many sales

If you want to move the needle quickly, partnerships with companies who themselves have a lot of customers is a good way forward. That’s been a focus. - Towards a unified API model

Cambridge is looking to both pull its own products into one offering and then put it alongside Fleetcor’s other payment products. For large corporates, that may be very compelling. For standalone fintechs, it will be something harder to compete against.

Not only good news though. In Q1 2020, Cambridge registered a $90m bad debt loss. A big trading client in the agricultural sector entered voluntary liquidation as a consequence of the financial pressure of Covid-19 and defaulted on its margin call. While hedging accounts for 30% of Cambridge revenue, the loss will likely have a negative effect on the company’s financials.

According to Cambridge, this is a one-off occurrence as the business has never experienced more than 1.5% bad debt as a percentage of revenue. Also, client trading will be closed or capped above the client’s established credit limit. How this will impact the company’s valuation is uncertain. But hoping that Cambridge is right, we might expect growth to resume in the next quarters.

While organic growth will continue to be a priority in Cambridge’s future strategy, we’d expect some M&A backed by Fleetcor’s experience to happen at some point too.