In this report, we give an update on some of the biggest projects around the world aiming to make cross-border payments faster, cheaper and more accessible, giving key insights on the challenges these projects are facing moving forward.

Globally, banks and payment industry players are seeing demand for faster, more accessible payments.

To unlock the potential and meet the demand for global trade, businesses, financial institutions and individuals need to be able to rapidly settle payments for goods and services across borders as quickly and easily as if they were paying for items in their own country.

However, the cost and speed of cross-border payments remains a major barrier compared to domestic payments. Our most recent data shows that the average margin cost of sending the equivalent of $200 was more than 5% across 56% of the 6,362 currency corridors we track, while transfers are mostly received within one or two days.

In response to this demand for faster, cheaper payments, countries around the world have already begun mobilising plans for improving cross-border payments. In 2020, the G20 gave its endorsement to a report on this topic, developed by the Financial Stability Board and other organisations, looking at the key challenges involved with enhancing cross-border payments and establishing a key roadmap of objectives for countries to follow.

In this report, we break down the key information you need to know about some of the biggest central bank-linked schemes and cross-border platforms in development worldwide to find out what organisations around the world are doing to make cross-border payments easier.

India: Unified Payments Interface expansion

Owned/managed by: National Payments Corporation of India

What is the Unified Payments Interface?

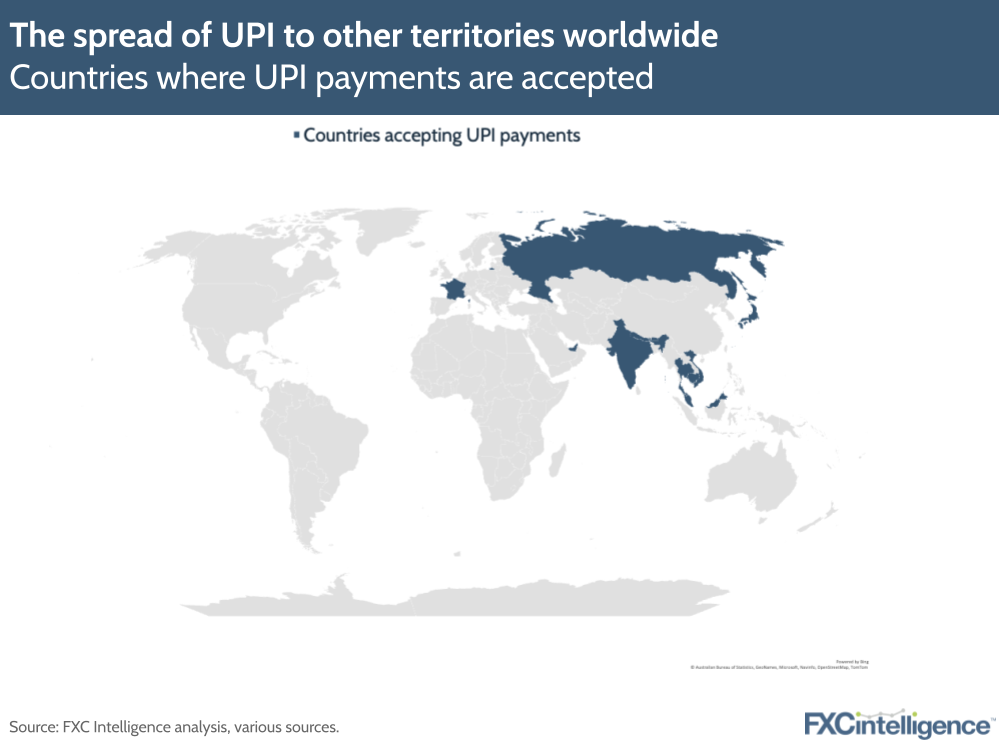

The Unified Payments Interface (UPI) is a mobile payment system that enables peer-to-peer and person-to-merchant transactions across India. With the system, users can send money abroad, pay bills and authorise transactions from their UPI app.

UPI has been a mainstay in India for some time, but the country is now taking steps to deploy the system in other territories. UPI is managed by NPCI International Payments Limited (NIPL), a wholly owned subsidiary of the National Payments Corporation of India, which is itself a division of India’s central bank, the Reserve Bank of India.

NIPL has made agreements with countries such as the UAE, Nepal, Bhutan, Singapore and Japan, to link UPI with payment schemes in their jurisdictions, which would make it easier and faster for people in those countries to send money to each other and internationally – it also aims to make it easier for Indian citizens travelling to these countries to send money back home.

What problem is UPI trying to solve?

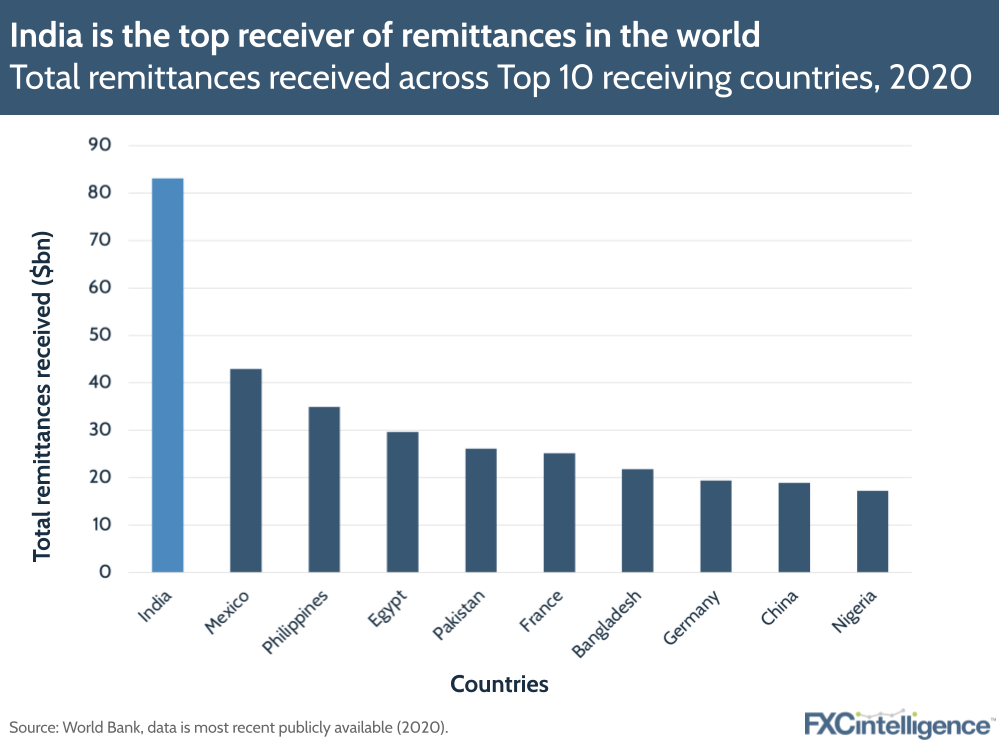

India is the largest remittance receiving country in the world, having received remittances worth $87bn in 2021 (an 8% increase) according to the World Bank. Huge numbers of migrants move from India to other countries every year and the country exports a huge amount of goods and services worldwide. The US, UAE, Singapore and Nepal all have particularly significant remittance flows to and from India, with the US recently surpassing the UAE to hold the largest share of remittances into India.

Payments between cross-border countries require international corresponding banking relationships, but if UPI can be linked up with domestic payment schemes in other countries, this will enable easier payments between the two countries.

One of the key links already enacted was between Singapore’s PayNow system and India’s UPI. The objective was to create faster, cheaper and more transparent cross-border payments between the two countries by enabling the systems to send standardised messages to each other, bypassing the need to send payment via an external system that adds additional delays and fees.

Looking at our data, we found that 59% of the 17 providers we track on the Singapore-India corridor offer cheaper FX margins than across other corridors (when transferring an amount equivalent to $300), with two major money transfer companies being more than three times cheaper to use than on other corridors. However, this is just one example including two countries where a UPI partnership has been formed.

Where is the UPI project up to?

NIPL has signed agreements with several countries in the Middle East and Asia-Pacific, including the UAE, Nepal, Bhutan, Singapore and Japan, to deploy UPI payment rails in those jurisdictions. Recently, it was reported that NIPL is engaged in discussions with more than 30 countries regarding the adoption of UPI.

The expansion of UPI is just one central-backed bank scheme being operated by India under its Payments Vision 2025 initiative, which explores several updates the country is applying to its payment systems to make it easier for migrants to send money back home.

For example, through the Indo-Nepal Family Remittance programme, Nepalese citizens in India are able to remit up to 50,000 rupees via their bank to Nepal (as long as the bank is a participant under India’s National Electronic Funds Transfer scheme). The programme has since been expanded with new rules that expand it in several ways – removing the existing cap on remittances and increasing the maximum amount for transactions from 50,000 rupees to 200,000 rupees.

Europe: Single Euro Payments Area

Owned/managed by: The European Commission and the European Central Bank

What is the Single Euro Payments Area?

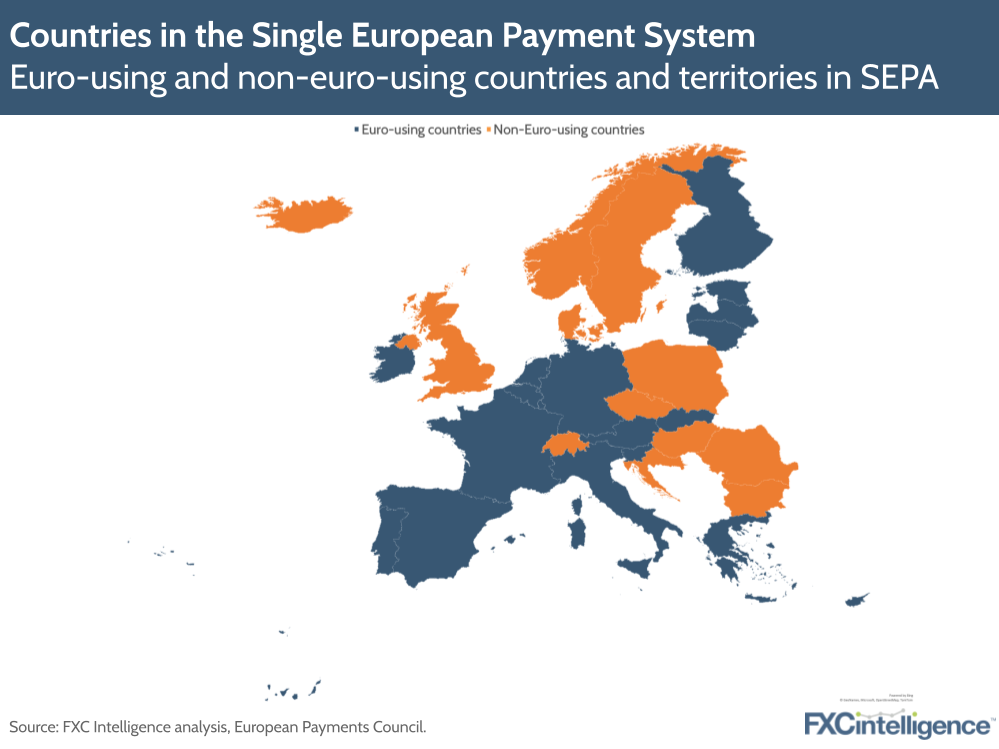

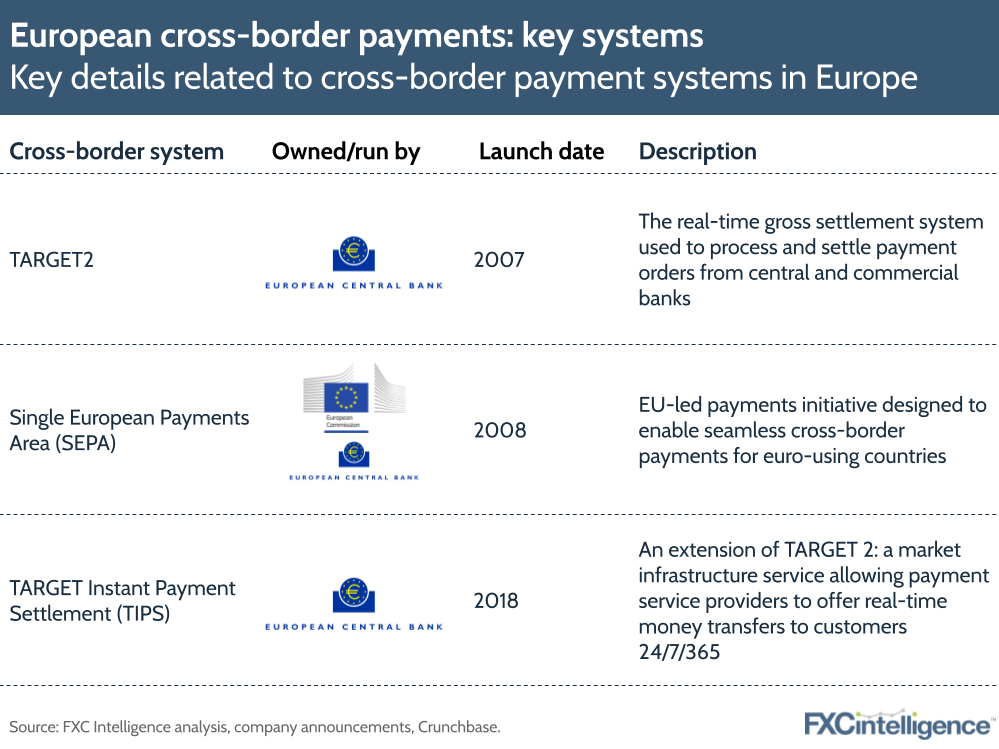

Launched in 2008, the Single Euro Payment Area (SEPA) is an initiative aimed at ‘harmonising’ cross-border payments between countries that use the euro, with the intention of making them as simple, cheap and fast as domestic local payments.

The area covers 36 European countries in total, including EU countries and countries that are involved in the scheme via financial agreements (e.g. the three non-EU members of the European Economic Area agreement: Iceland, Liechtenstein and Norway).

The SEPA effectively replaces the usual system for cross-border payments with SEPA transfers, which is split into three tiers: the SEPA Credit Transfer, the SEPA Instant Credit Transfer and the SEPA Direct Debit Transfer. Financial services facilitating cross-border transfers across SEPA countries have been required to implement these in their schemes.

SEPA transfers allow individuals and businesses in the SEPA to make cash-free euro payments to any account located in the region via a single bank account. For countries within the SEPA that don’t use the euro, cross-border payments still require a conversion to the euro, which is why some of them are introducing their own cross-border schemes (see our discussion of P27 below).

What challenges does the SEPA system aim to solve?

While charges for cross-border payment may have varied greatly in the past, under SEPA regulations banks are required to apply the same charges for domestic and cross-border payments in Euro. For transfers between two euro-using countries, this reduces costs and creates greater competition between private money transfer providers, which leads to more competitive margins that reduce prices for consumers even further.

By removing friction from intra-European cross-border payments, the system was implemented to help boost trade across Europe, which in the past has been fragmented; for example, in the past, businesses may have had to deal with many different payment card standards for euro payments. However, consumers now have to use just one payment account and card to make payments wherever they are in Europe.

Where is the project up to?

Financial services in SEPA regions have now migrated onto SEPA’s transfer schemes, meaning that cashless euro transactions are underway. Moving forward, according to SEPA, the next stage of the project will focus on greater harmonisation across mobile and online payments.

The Eurosystem, the monetary authority representing euro-using EU member states, is currently investigating the use of a digital euro, which would exist alongside the fiat version of the euro and provide a more stable payment system.

This project seems to be responding to the reduced use of cash in Europe, the volatility of increasingly popular cryptocurrencies and the fact that more countries are introducing central bank digital currency (CBDC) projects worldwide (see the section on CBDCs below).

Reflecting growing needs for instant payments systems worldwide, the Eurosystem has also developed TIPS, an extension of TARGET2, its real-time gross settlement system used to process and settle payments from banks in Europe. The goal of TIPS has been to enable real-time money transfers to customers, and its potential for cross-border payments is being increasingly explored. Recently, Swedish central bank Sveriges Riksbank successfully completed the first phase of its migration to TIPS, the first step towards enabling instant settlement of Swedish krona across borders.

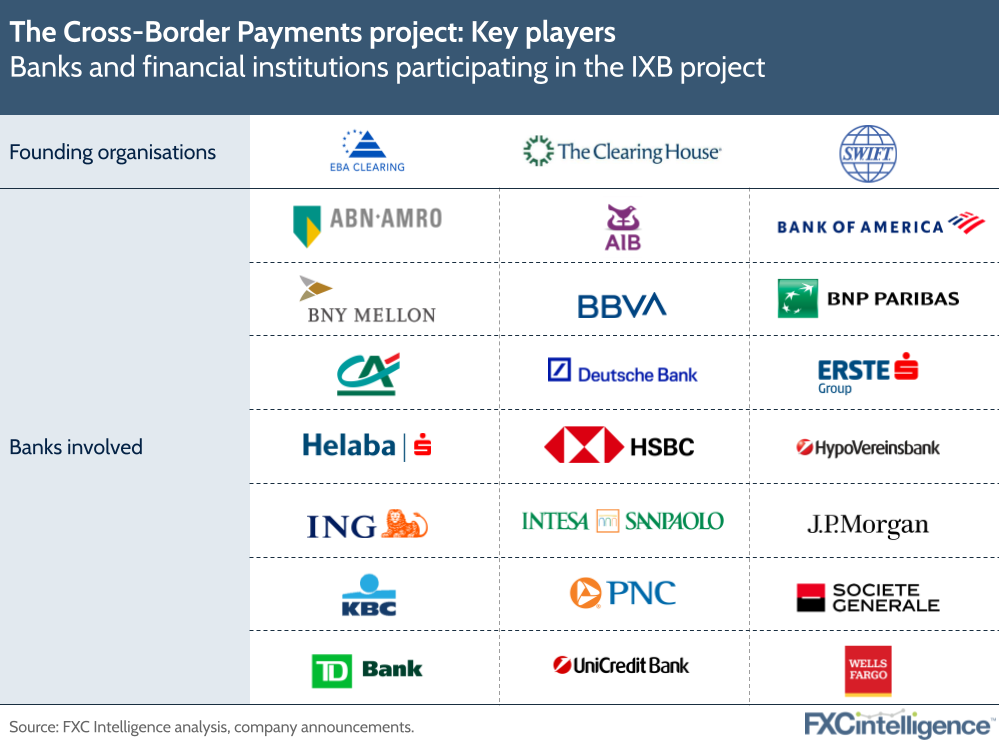

US-Europe: The Immediate Cross-Border (IXB) payment scheme

Owned/managed by: EBA Clearing, Swift and The Clearing House

What is the Immediate Cross-Border payment scheme?

The Immediate Cross-Border (IXB) payment scheme is an initiative to speed up cross-border payments over the US to Europe corridor, enabling 24/7 payments between parties in two separate countries in real-time. Initially, the focus will be on the US-Europe corridor, but this could be extended to other countries.

Formed as a result of a partnership between major payment organisations EBA Clearing, SWIFT and the Clearing House, the scheme will make use of two existing domestic instant payment systems – the Clearing House’s RTP network in the US, and RT1 in Europe. Essentially, the project aims to allow payments to be settled in two domestic instant payment systems situated in different countries at the same time.

What are the challenges the IXB system aims to solve?

Slow, costly and non-transparent cross-border payments between banks in the US and Europe currently rely on correspondent banking and lengthy delays for settlement. This affects trade, e-commerce and industry, which bear the brunt of additional costs and delays. On the other hand, a new more interoperable system could pave the way for a system where transferring money abroad is as easy as a domestic payment.

Where is the IXB project up to?

The IXB project is expecting to launch a pilot project by the end of 2022, with participants joining in phases. At the moment, it’s being designed with the contribution of 24 financial institutions. The project went through a proof of concept in October 2021, which saw participation from seven organisations and tested the concept of instant real-time payment between two different systems.

It’s expected that the pilot will be followed by a full service offering in 2023.

Africa: The Pan-African Payment and Settlement System

Owned/managed by: Afreximbank, AfCFTA Secretariat

What is the Pan-African Payment and Settlement System?

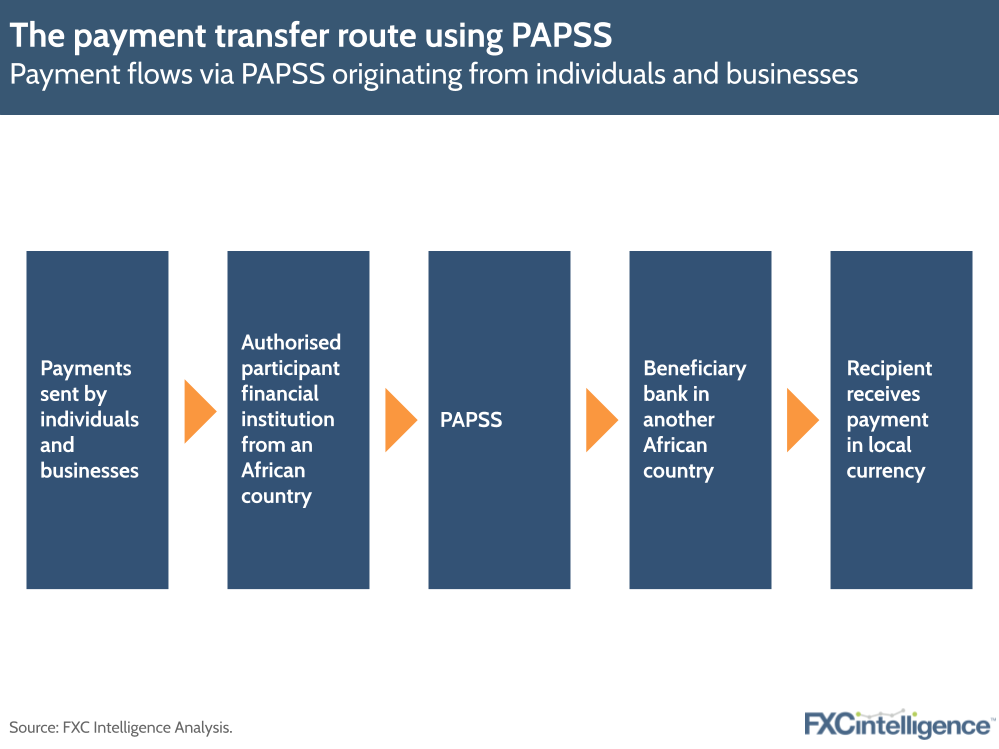

The Pan-African Payment and Settlement System (PAPSS) is a payment system that will enable instant secure payments between African countries, simplifying the complexities and costs of transfers across African borders. It’s the latest milestone of the African Continental Free Trade Area (AfCFTA), which aims to boost trade and achieve greater prosperity across the continent.

Companies send payment instruction in local currency to their PAPSS-participating bank/payment service provider. This is then sent on to PAPSS, which carries out validation checks and passes it on to the receiver’s bank/payment service provider, which then clears funds to the receiver in their local currency.

What challenges does the PAPSS system aim to address?

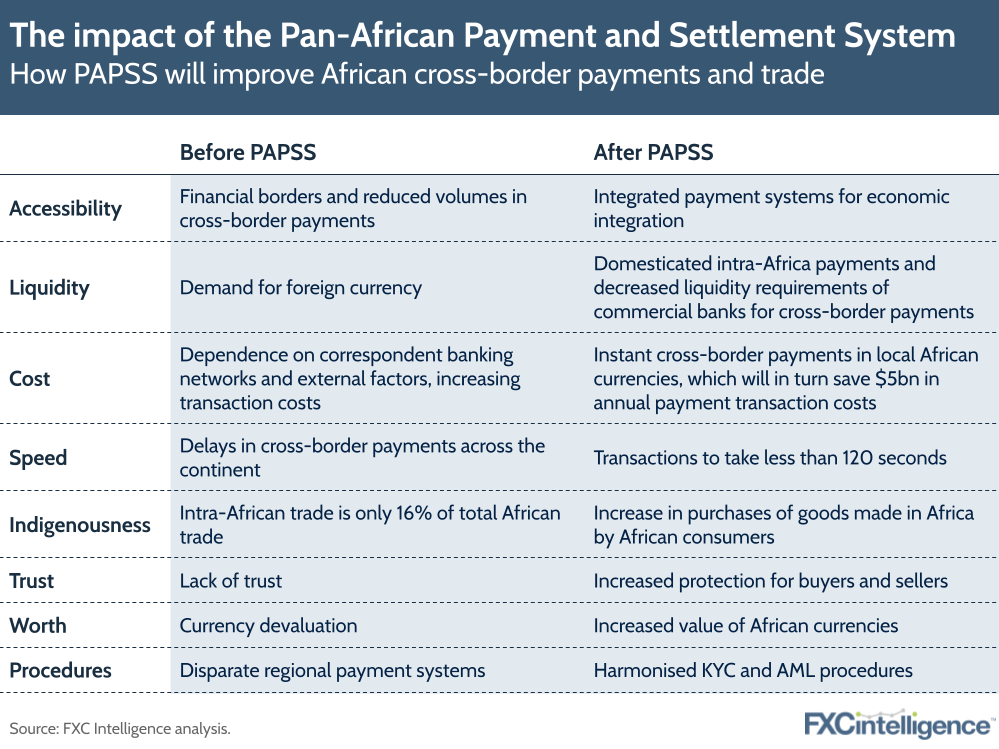

The current intra-Africa payments system is a complex one. The continent has a large unbanked or underbanked population, which has led to the emergence of lots of mobile wallets/digital payment services. As cardless transactions and online activities grow, the ease and convenience of these solutions continues to drive the growth of neobanks in the country. Neobanks have also often attached specialised remittance services to serve Africa’s high emigrant population.

The issue is that these mobile banks often aren’t interoperable and don’t have a direct banking relationship. Intra-Africa payments across borders often need to be routed to other third-party banks outside of the country to process payments, which can add significant delays and costs to the process. In turn, these delays and costs hamper intra-Africa trade.

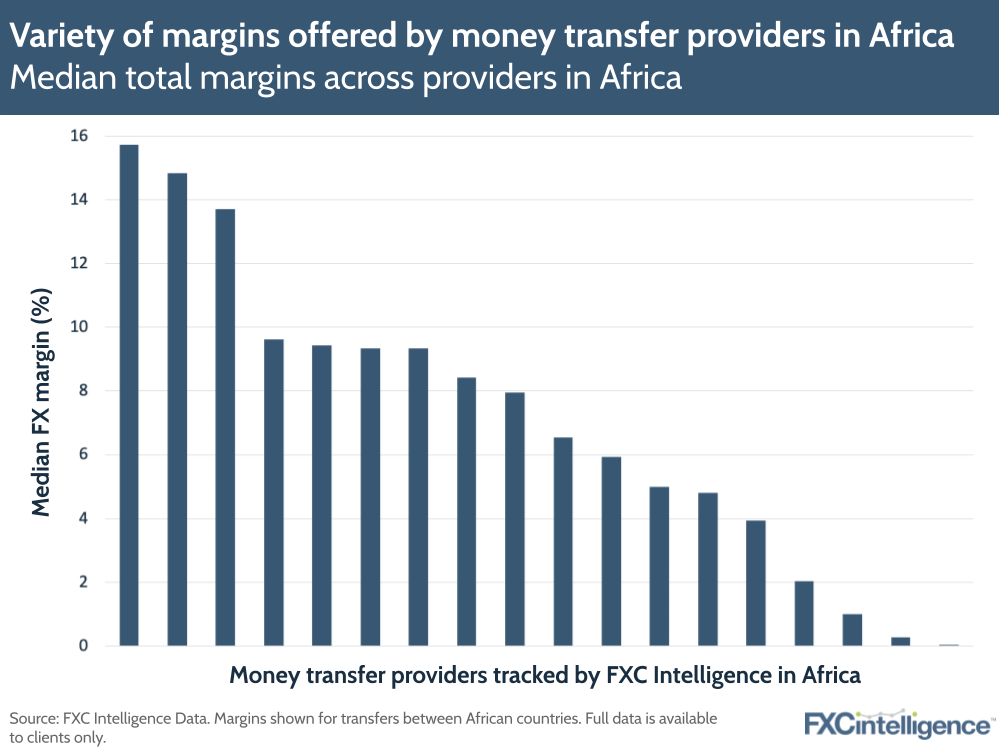

For the corridors we track offering transfers within Africa, we found a large spread of margins offered by each provider with the range in median of providers total margins being over 15%. That means that the range of margins (i.e. costs being applied on money transfers via fees and FX markup) across intra-African corridors is high, unlike Europe where prices are much more competitive.

The median prices for intra-Africa transfers was more than seven times as much as the median intra-Europe cost across corridors tracked by FXC. Altogether, intra-Africa transfers are not only significantly more expensive on average than intra-Europe, but there is a much higher variety in prices across corridors.

PAPSS aims to provide a link between countries’ domestic currencies, allowing participating banks to facilitate faster, speedier and more efficient cross-border payments. The end goal, eventually, will be in stimulating intra-Africa trade, promoting the growth of businesses and the local economy.

Where is the project up to?

In July, PAPSS said it is now compliant under the ISO27001 standard. The initiative is continually expanding across Africa and as of April 2022 was reportedly seeing participation from eight central banks and 25 of the largest commercial banks on the continent.

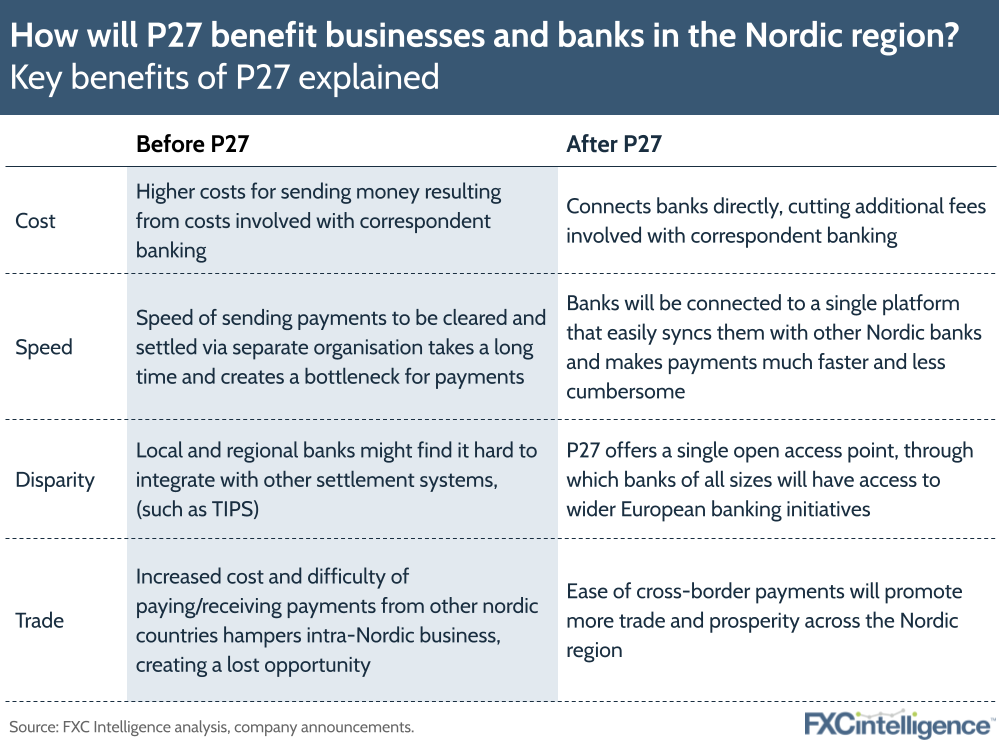

Nordic region: P27

Owned/managed by: A coalition of Danske Bank, Handelsbanken, Nordea, OP Financial Group, SEB and Swedbank.

What is P27?

P27 refers to a new system to enable instant real-time payments across Nordic countries, including Denmark, Sweden and Finland. Norway and Iceland, meanwhile, have yet to commit to the project.

Similar to other cross-border interoperability systems on this list, P27 aims to link the localised payment systems of the individual jurisdictions and enable them to synchronise payment settlements in both places at the same time.

What are the challenges the system aims to address?

Even though they are in close proximity, cross-border payments between Nordic countries can be expensive and time-consuming.

Unlike European countries that are part of SEPA, the difference in currencies between Nordic countries means they must go through a foreign exchange process via the SWIFT system, which comes with all the difficulties involved with correspondent banking. For example, it is often easier for customers in Finland (part of SEPA) to make cross-border payments to Germany than Finland, despite its proximity.

Similar to PAPSS, an intra-Nordic payment system linking the fast payment systems used by Nordic countries could result in faster, cheaper cross-border payments that promote intra-Nordic trade and create greater equality between larger and smaller banks in the region.

Where is the project up to now?

13 banks linked to the Swedish instant payments solution Swish are set to test the P27 platform by the end of the year. P27 is expected to process all Swish payment flows from 2023.

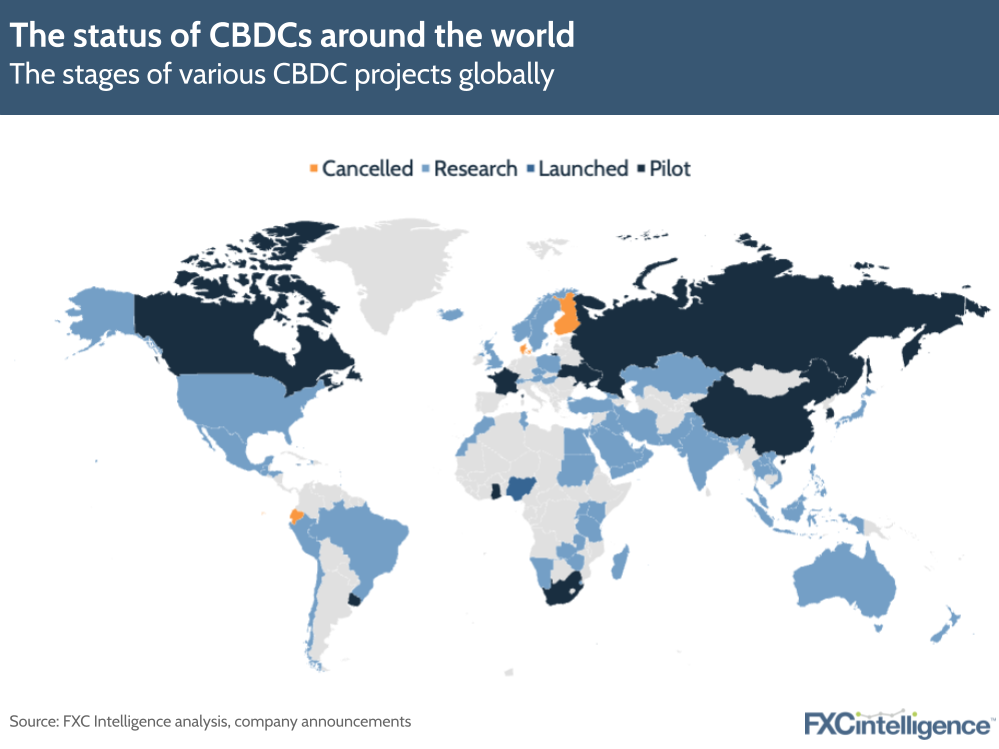

Worldwide: Central bank digital currencies (CBDCs)

A number of countries, from the Bahamas to India to Singapore, have introduced projects surrounding the use of central bank digital currencies (CBDCs). Pegged to the fiat currency of their respective country, these digital forms of central bank money would operate on a separate payment infrastructure to existing legacy banking systems and, in theory, could enable real-time instant settlement of cross-border payments 24/7.

To zone in on one such example, the mBridge project is attempting to show how these digital currencies could be used to complete cross-border payments and settle payments instantly. It’s being developed by the Bank for International Settlements (BIS) alongside four central banks (Hong Kong, Thailand, China and the UAE), and has received support from banks including Goldman Sachs, HSBC and Société Générale.

The idea of mBridge is to create a common platform that would allow faster, cheaper and safer international cross-border payments. It would do this by joining up national CBDCs – being developed by the countries in question – into a common payments infrastructure that wouldn’t require payments to rely on correspondent banking, but would instead allow payment and settlement to occur instantly for both CBDCs at the same time.

Navigating away from correspondent banking would eliminate the issues inherent within that system – for example, the fact that intermediary banks are closed at different times, or charge additional processing fees. Another issue raised in the mBridge report is that many banks are currently ‘derisking’ – ceasing relationships with foreign banks and international payment services – seemingly because of the cost of complying with cross-border payment regulations.

The potential of CBDCs is still being explored, and projects regarding cross-border payments are still in their early stages. The BIS recently released a new report on the interoperability of CBDCs for cross-border payments, and central banks continue to announce/give updates on their ongoing CBDC projects.

Key takeaways for improving cross-border payments

Examining these cross-border payment schemes more closely, there are a number of commonalities. Clearly, there are three core objectives for schemes to improve cross-border payments: cheaper, safer and more transparent payments across borders.

A key theme running through the projects here is interoperability: finding ways to connect existing fast payment systems and standardising messaging so that payments can be settled in both systems at the same time. There has been a focus on eliminating or reducing the impact that FX conversion can have on fees for cross-border transactions.

For example, the PAPSS system eliminates the need for currencies to be sent out of Africa to be converted to hard currencies before being sent back. Instead, payments pass through PAPSS and money is paid out in the local currency.

In many regions, interoperability is largely being driven by private companies, with central banks playing a supporting role (e.g. through clearing). Central bank involvement, for example, currently varies across the PAPSS project; as of April 2022, the number of central banks participating in the programme was reportedly eight, while the AfCFTA comprises 55 countries. The P27 Nordic scheme is led by a coalition of the biggest commercial Nordic banks, with three central banks supporting and carrying out clearing of payments.

A great deal of effort to create better cross-border interoperability is focused in Asia, which has already seen major projects to reduce the cost and increase efficiency of cross-border payments. This can be seen in India and Singapore linking their instant payments systems, and the investigation of CBDCs by several countries in the region.

Many of these cross-border payment projects are being framed more from a perspective of making payments easier between financial institutions, with the impact of this trickling down to consumers and businesses. The P27 initiative, for example, is focused on making interbank payments easier by streamlining the clearing process, thereby enabling faster cross-border payments. The expansion of UPI, meanwhile, appears more focused on directly aiding and speeding up money transfers.

What’s clear is that institutions around the world are beginning to understand the pitfalls of slow, costly cross-border payments. We’ll be continuing to track the progress of these cross-border payments projects (and others as they arise) in the months to come.