At the end of 2021, Santander pulled the plug on its international money transfer service PagoFX around a year and a half after it first launched in August 2020. Promising fast, transparent payments, PagoFX aimed to be a key challenger in the FX space and specifically targeted Wise. But after opening in just three sending corridors, Santander closed the service, refocusing its wider PagoNxt brand on B2B services through Getnet, One Trade and Ebury. So, what went wrong?

In its most recent results, Santander reported a significant climb in losses of its PagoNxt division, with the first three quarters of 2021 seeing €206m losses compared to €61m in the first three quarters of 2020. How much PagoFX contributed to this is unclear, with Santander citing other expenses, particularly in its trade segment, as contributing. However, it is unlikely PagoFX reached anywhere near the scale to be profitable, or had a clear path to reach scale – Wise had to drive nearly $100m of revenue before it reported its first annual profit.

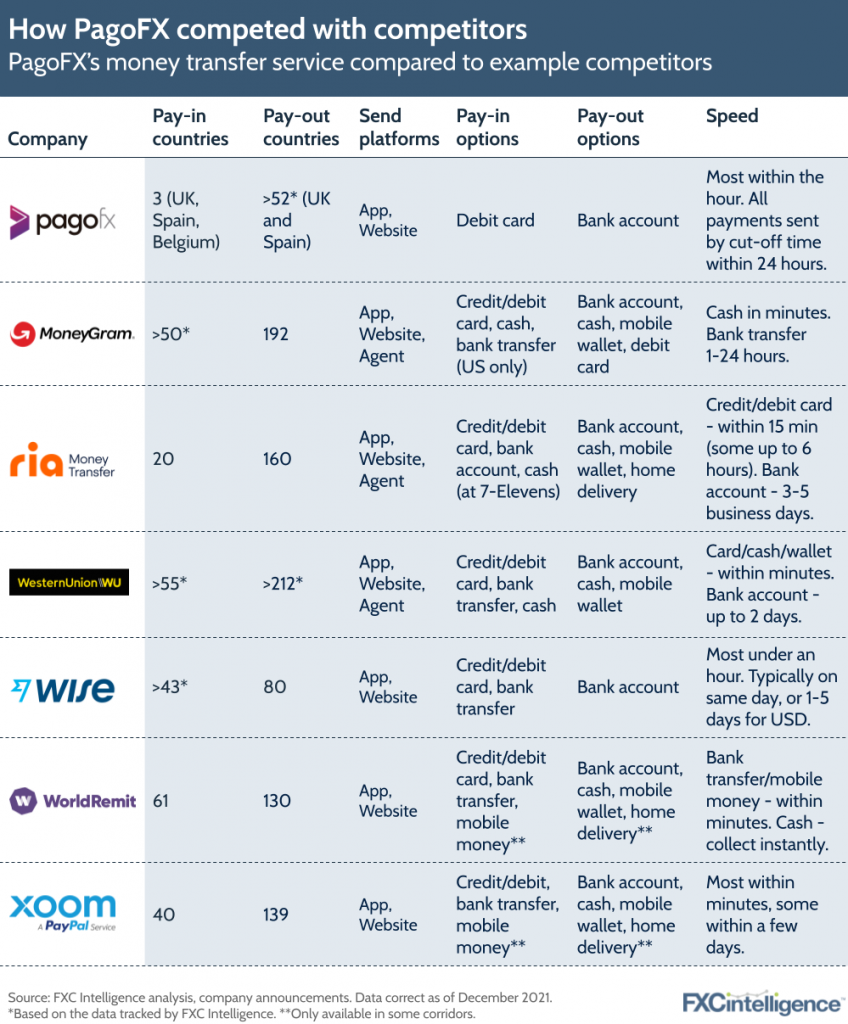

This may explain Santander’s decision not to give PagoFX longer to prove itself, but its lack of traction can also be explained in how it stacked up against its competitors. While it was broadly competitive in terms of speed, it lacked the pay-in and pay-out options of many other competitors, and operated in fewer markets.

Notably, it lacked any features that made it stand out from competitors, with no offerings that showed marked differentiation from other app-first players such as Wise and WorldRemit. There was some effort to attract customers through a number of promotional discounts, but otherwise much of its efforts were restricted to standard content marketing practices that were designed to increase the company’s online presence. This does not appear to have yielded significant interest, with search trends for PagoFX dropping off after its initial launch in the UK.

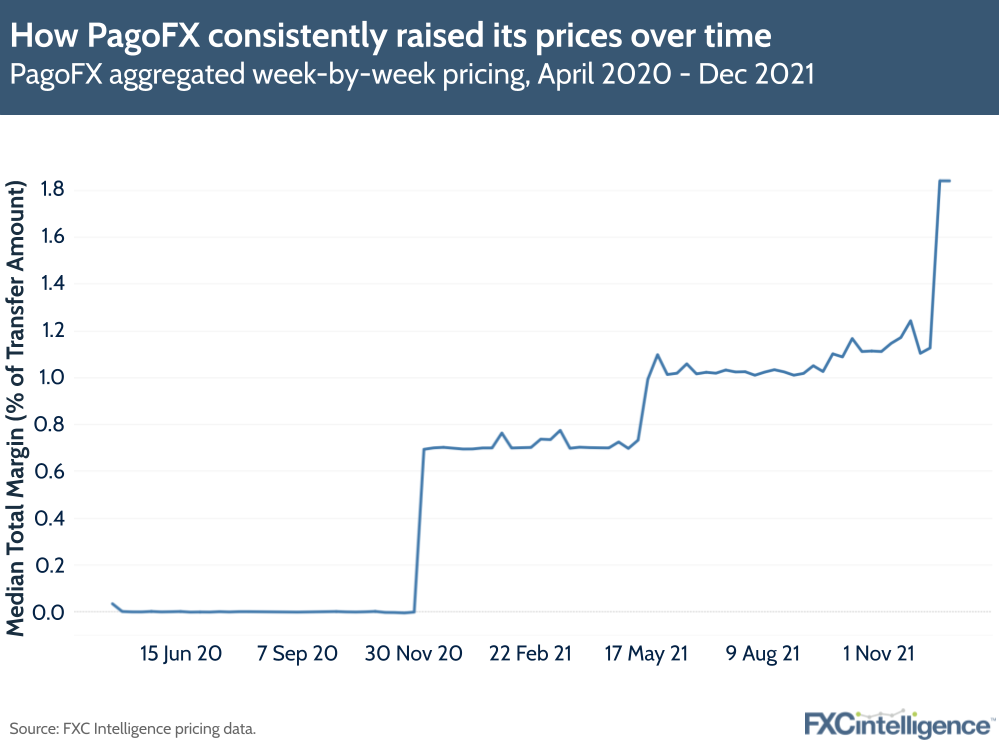

Where PagoFX did attempt to compete more strongly was on pricing. Our own pricing data found that the company was in the cheapest 20% of providers for almost 60% of the corridors it operated in, and below average for around 80%. The company was particularly competitive on pricing in Europe and Asia, suggesting these corridors were seen as priorities.

However, despite pricing competitively throughout its run, PagoFX consistently increased its prices over the course of its operation, suggesting the company was pursuing a strategy of very low pricing to gain initial customers before increasing prices towards a more sustainable business model. Neither worked.

While PagoFX has now ceased operating, Santander’s PagoNxt division has retained a consumer company in the form of Superdigital and may still leverage some of the infrastructure behind PagoFX.

Targeting financial inclusion in Latin America, Superdigital serves the region with app-based financial services that include money transfers, bill payments and international virtual cards. For Santander, Superdigital may ultimately represent a better consumer strategy, tackling a faster growing, less competitive market that offers greater long-term potential.

Additional research by James McKee.