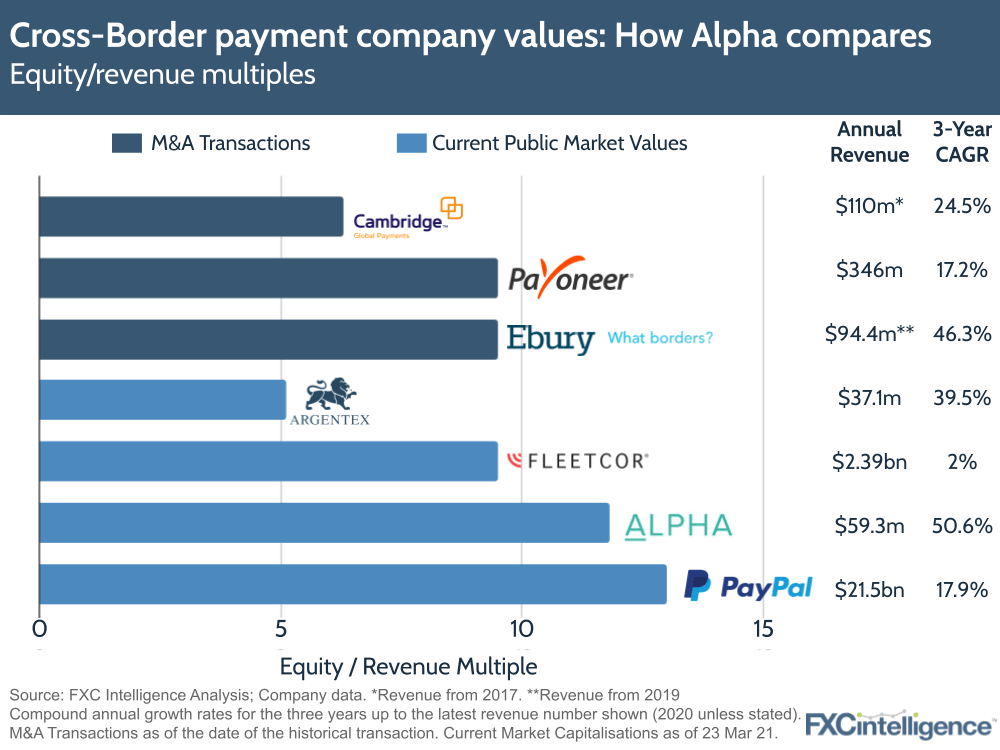

Alpha FX has a current market cap of c.£550m ($750m) and is trading at some of the highest multiples in the sector. How does it compare to other companies in B2B payments?

To assess how Alpha’s value compares to its peers, we looked at two groups – values from recent M&A transactions and competitors who are currently publicly listed. Unfortunately, there are not many direct comparisons available.

On the transaction side, the 2017 sale of Cambridge to Fleetcor and 2019’s sale of Ebury to Santander look the closest. Both these companies have a broader range of customers than Alpha, from SMEs up (Alpha focuses on mid-market corporates and institutions). Payoneer offers an interesting comparable too as the only cross-border payments focused ecommerce group, which is now coming to market via a SPAC.

On the public markets side, Argentex is the most similar. Argentex is around two thirds the size of Alpha and had a tougher 2020, trading at a much lower multiple. Fleetcor, a large US payments conglomerate (which owns Cambridge and is about to complete the acquisition of Afex) trades below Alpha as well.

To find a company trading above Alpha’s level that has material B2B cross-border payments, we had to bring industry star PayPal, a company valued at $275bn, and that still is a push given its consumer and ecommerce focus too. (We didn’t include Western Union Business Solutions as it accounts for only 8% of Western Union overall.)

Which leads us back to Morgan and his team at Alpha. What will they have to do to continue to maintain valuations multiples that lead the sector? Continued high growth will be the baseline, but will this be enough? We’ll be watching closely.