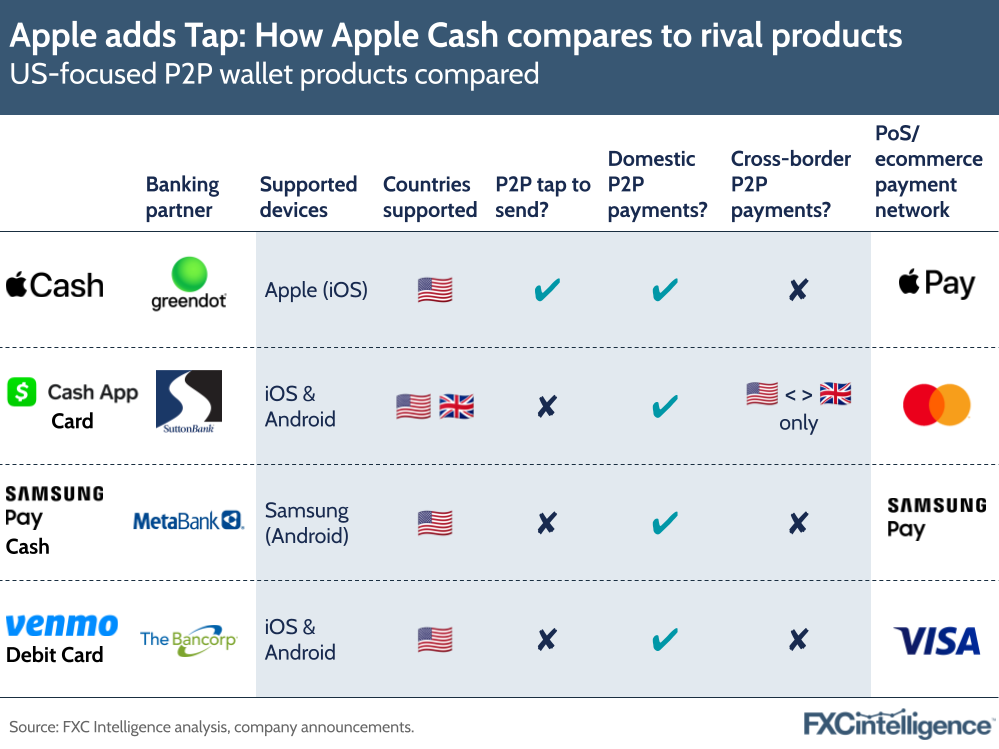

This week, Apple held WWDC24, the latest iteration of its yearly developer conference. Among the usual hardware and software announcements was the news that it was launching a near-field communications (NFC)-based P2P payments system, dubbed Apple Tap to Cash.

An add-on for Apple’s US-only Apple Cash service, Apple Tap to Cash allows users to make P2P payments by bringing together their phones to automatically transfer an agreed-upon amount.

“Continuing on our journey to replace your physical wallet, we’re introducing Tap to Cash, a quick and private way to exchange Apple Cash without sharing phone numbers or email addresses,” explained Craig Federighi, SVP, Software Engineering at Apple, during the keynote. “With Tap to Cash you can pay someone back for dinner just by holding your phones together.”

The technology is only available in the US for customers with Apple Cash, a combined wallet and virtual card-like service that sits within a customer’s wider Apple Pay wallet alongside other third-party cards, and so is limited to iPhone owners with the service in the US only.

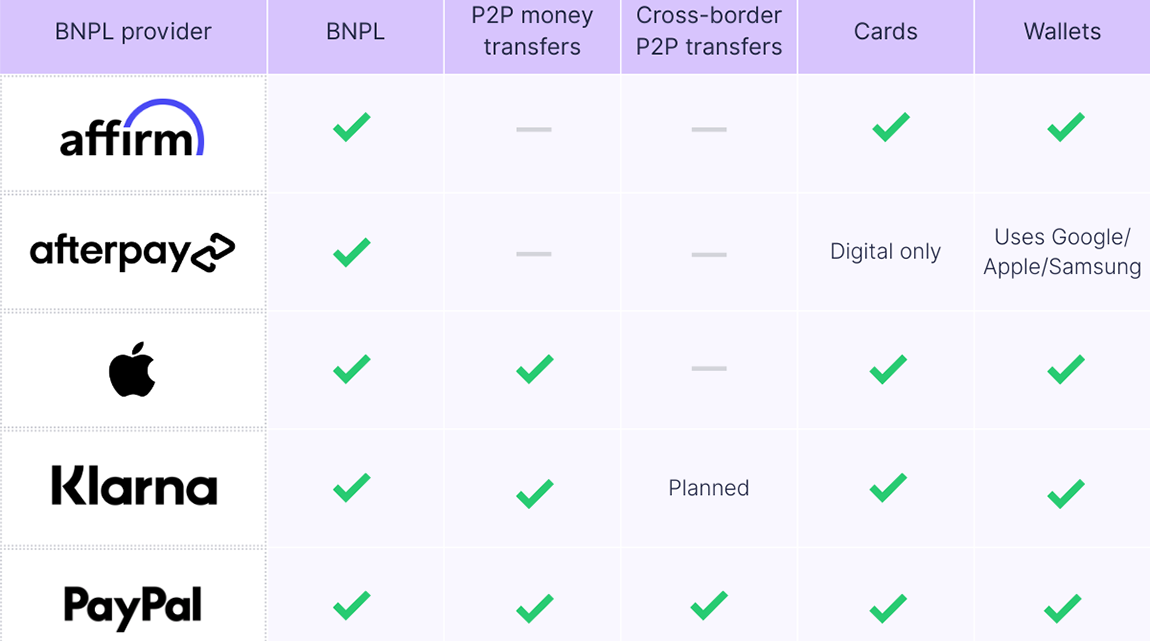

While there are several similar products available in the US market, including Samsung Pay Cash and the add-on cards for e-wallet-based products Venmo and Cash App, this is the first high-profile solution to incorporate the NFC payment feature in this way – although it does follow some smaller solutions with similar technologies. Tap to pay functionality is now widespread for point-of-sale purchases, but there have been limited P2P products with this technology included.

However, this may change. Visa announced the addition of Tap to P2P – a P2P payment solution by tapping mobile devices – at its annual Visa Payments Forum in May and other providers may follow Apple’s suit.

Nevertheless, the technology’s need for physical interaction and its lack of availability beyond the US – as well as its lack of support for cross-platform or cross-border transactions – may ultimately limit its use. It is not clear how much easier the solution will be to sending a P2P payment from within an app, and therefore how significant user adoption will be.